Date of Data Capture:

23/10/2019

Name:

WESTERN AREAS LIMITED (WSA)

Classification:

Nickel Ore Mining

Current Price:

$3.25

Market Capitalisation:

$889M

Forecast EBITDA Growth:

114.11%

Yield Estimate:

1.21%

Consensus Price Target:

$3.05

# Covering Analysts:

14

Premium at Current Price:

6.15%

Price Target Trend (3-Month):

Up-Flat +17.31%

Signal Timeframe:

Quarterly-Monthly-Daily

Trend Bias:

Up-Down / Long-Medium

Indicators:

Short-term:

Positive

Medium-term:

Positive-Neutral

Long-term:

Positive

Recommendation:

Buy

Focus:

Capital Growth

Set up Notes:

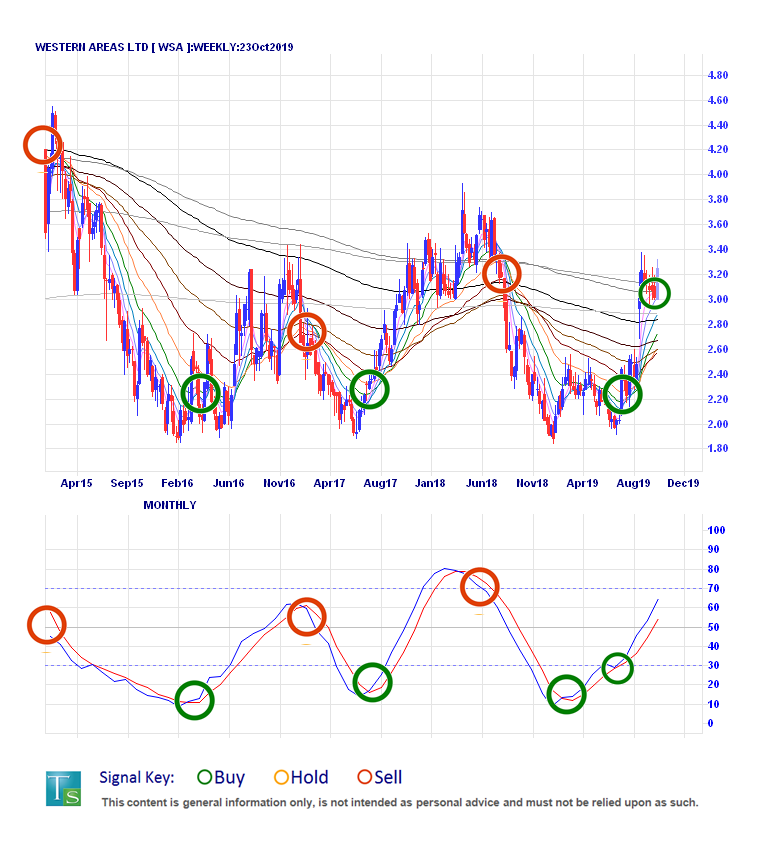

• Moving higher within a medium-term uptrend WSA looks set to continue its upward journey, backed by steadily improving performance, an exciting technical setup, and strong forecasting.

• Consistent sales growth from 2017 belies a volatile earnings history, with underlying nickel commodity pricing and fluctuating margin levels causing large swings in value, but here we see very strong forecasting expected into next year.

• Pricing shows recent medium-term cyclical price moves with the company still working out of a major long-term downtrend from 2008 highs, we are following long-term signalling here, backed by fresh strength in the shorter-term timeframes.

Support ($): 3.00, 2.75, 2.50, 2.25 & 2.00.

Resistance ($): 3.50, 4.00, 4.50, 5.00 & 6.00.

Growth Focus:

WESTERN AREAS LIMITED (WSA)

Our primary focus here is capital gain, we will select our stocks from the ASX Top 500 All Ordinaries Index.

We are always looking for the hottest spots and best areas in the market for emerging growth trends - with the recent strength and excellent outlook for nickel, we think we might be unearthing a bargain with Western Areas as the low-cost producer surges on strong results and forecasting.

Listed on the ASX since mid-2000, Western Areas is an Australian nickel miner/producer with some of the lowest cost and highest grade nickel assets in the world. The company has an active asset development program, with resources and reserves being significantly upgraded in recent years. Ongoing investment into its mines should see growth maintained, with particular focus being given to the underground expansion of the Odysseus mine at Cosmos in Western Australia, offering a long-term mine life at low costings. An active exploration program is maintained with further high-potential prospects in Western Australia and Canada, providing a healthy pipeline for future growth.

Recent results showed strong mining performance offset slightly lower mine grading and currency moves. Increasing nickel pricing saw a boost to cash flow, adding to a good balance sheet recently boosted by the sale of its Kidman stake to Wesfarmers. Recently, the Indonesian government brought forward its planned 2-year ban on nickel exports to January 2020, which should see stockpiling continue to be reduced with LME levels already at 11-year lows, which should provide ongoing price support.

Performance fundamentals have been mostly good, with strong sales growth leading mostly steady gains in earnings, though the softer results of 2019 should give way to a strong 2020, with forecasting showing a strong boost to sales, margins, and earnings expected out to 2021. Analyst sentiment remains strongly majority positive, and while the stock does currently 6% sit above consensus targets, these aggregate valuations have risen 17% in the last 3 months alone.

Since listing on the ASX almost 20 years ago WSA has seen a great many positive and negative cycles, though the current uptrend is really best seen as a greater recovery from a long-running downtrend, in place since mid-2008. The current recovery uptrend began in January 2019, as linear resistance broke and price bounced up off $2 support, and by September price was working on the $3 resistance ceiling, with this level is now turning into support. We see longer-term signalling for a new uptrend beginning here, now gaining some shorter-term momentum, and we think Western Areas could be a great place to be.