For a full copy of the article please contact me directly.

Although the price performance of CGF has been particularly strong in 2013 we still see plenty of potential for the company to continue to provide shareholders with healthy returns in the coming years. The dual structural forces of compulsory superannuation in Australia and the avalanche effect of baby boomers entering the retirement phase are extremely supportive for CGF’s annuities business. In addition, the funds management incubation business is benefiting from stronger fund flows and higher management fees due to outperformance of its investment products.

CGF is one of the company’s that almost collapsed during the global financial crisis in 2008. Its share price fell from above $6 to below $1, and we attribute the ability of then CEO Dominic Steven’s management skills that brought the company back from the near death experience. A strong focus on marketing campaigns to build the Challenger name as an annuities provider and the careful management of the investment portfolio has meant that CGF not only survived the GFC but it has flourished to become a poster child for retirement investment products. Based on the most recent result the annuities business accounts for more than 90% of company profits.

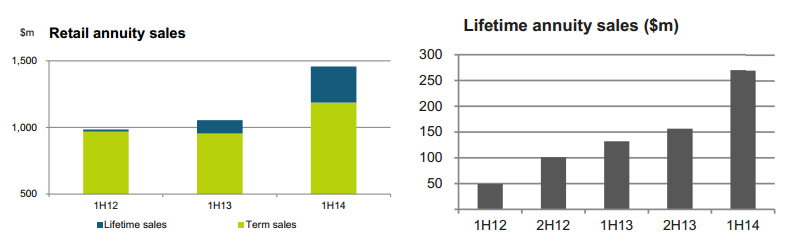

The loss of retirement savings that many Australian retirees experienced during the GFC because of their over allocation to equities was a lesson, and many retirees had finally realised that it was important that they allocate most of their retirement savings towards investment products that are low risk and could produce a steady stream of income. Australia is one of the few developed countries that have very few annuities products, and as a first mover this created an opportunity for CGF to exploit the growing demand. Although we do expect competition to enter the annuities space as the banks in Australia finally realise how lucrative the annuities space will become, the fact that CGF has already established its strong brand will always mean late entries will be playing a game of catch up. The other factors which ensure CGF will continue to ride the annuities wave include, the next decades will be a time when baby boomers will enter their retirement phase in record numbers, and the legislated mandate of compulsory super contributions will continue to pour capital that will need to be invested and which will eventually have to flow into annuities as people age and enter retirement. The rate of compulsory super contributions has risen from 6% when Paul Keating first introduced it in 1996 to 9.25% in 2013. This rate will keep rising in the coming years and will peak in 2021 at 12%. The total amount of super assets now stands at A$1.3 trillion and is expected to quadruple to A$5 trillion by 2030. It is not difficult to see that as long as CGF does not mismanage its assets it will remain a viable force in the retirement investment space for a long time.

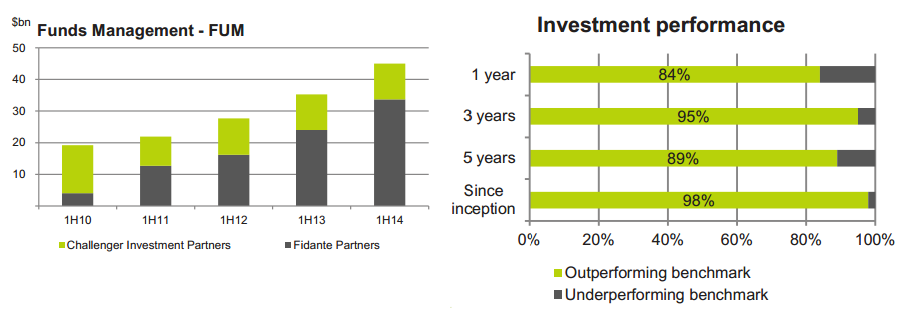

One of the hidden gems in the CGF business is its funds management incubation business. CGF invests alongside 14 boutique funds management companies, providing them with middle and back office infrastructure, and injects initial funds for the boutiques to manage whilst trying to gather institution fund flows. The reward for CGF is that as an equity partner it receives a percentage of the profits that the boutiques generate as they develop to become mature investment businesses. Judging from the success of the boutiques in its portfolio you would have to conclude that CGF has done a remarkable job with its due diligence. Over 90% of the investment products in the incubation companies are outperforming their investment benchmarks and funds under management has risen about 45% to A$45 billion over the last year. The combination of strong fund flows and investment outperformance leads to higher fees and is seeing incomes in the funds management segment rise 63%. CGF is one of those companies that investors should be accumulating for their portfolio for the long term, just like the annuities it provides we see the stock helping investors to generate healthy returns for many years to come.

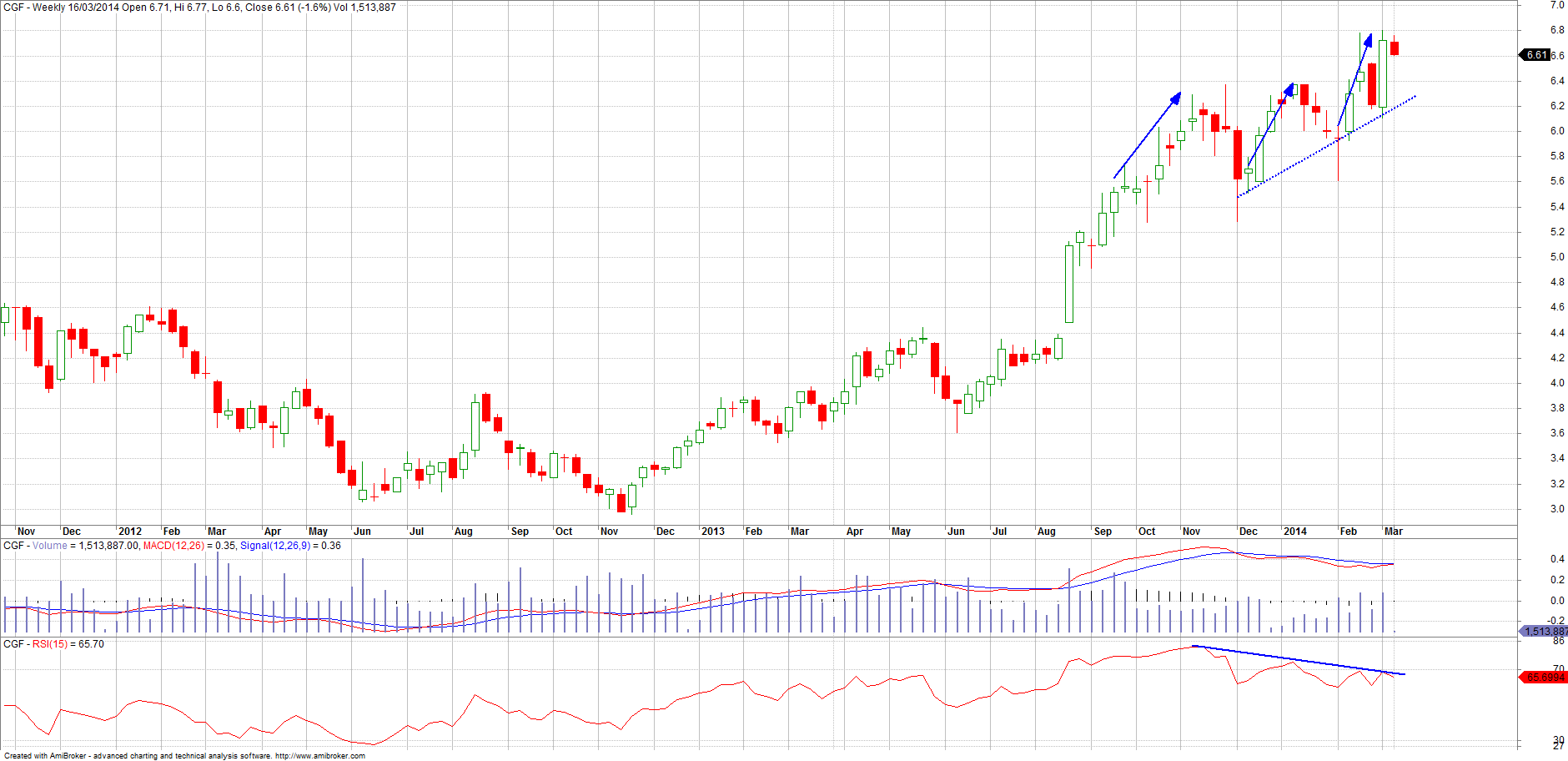

CGF has been trending very strongly for over a year now. Before the GFC hit, it reached an intraday high of $6.58. It has now managed to go through that level. However, we have noticed one negative signal that investors need to watch out for. The stock in our opinion appears to be making a three thrust high. This is indicated by the arrows on the chart. We have also highlighted divergence with the RSI. Sometimes when a top starts to form, the share price will make three attempts at testing these upper limits. CBA had formed the same pattern at its pre-GFC high, and then did the opposite to signify the end of its GFC low. We have drawn in the recent uptrend line that we need to look out for. The share price is still above that so investors do not need to panic just yet. As long as it continues to trend up, you can stick with it. But if it breaks that diagonal dotted line, then the uptrend is over, a top has been formed, and it is time to exit.