Below is an extract from our weekly research report. For a copy of the full report containing other investment and trading ideas, please contact us.

We see Resmed as a good business – looking back, it has been managed well and has delivered impressive performance given its capital base. For this, and for its US domicile, we see a valuation premium warranted when compared with the market. Why do we attribute value to a US domiciled business? Being listed in the United States, as a US-based company, allows Resmed to enjoy relatively cheaper capital than an Australian business. It is able to issue debt at lower margins to benchmark interest rates, by virtue of its US listing, as well as issue equity in a deep market, relative to Australia of course! However, as we are based in Australia, its 18 times earnings multiple ranks it lowly compared to other investment domestic opportunities, where we are able to attain sustainable growth at lower valuations. For this reason, we are negative on Resmed at current prices, but are cognisant that it begins to look appealing above $4.60.

The case for…

Resmed is a developer, manufacturer and distributor of medical equipment for treating, diagnosing, and managing sleep-disordered breathing and other respiratory disorders. Sleep-disordered breathing, or SDB, includes obstructive sleep apnea, or OSA, and other respiratory disorders that occur during sleep. When formed in 1989, its primary purpose was to commercialise a treatment for OSA. This treatment, nasal Continuous Positive Airway Pressure, or CPAP, was the first successful noninvasive treatment for OSA. CPAP systems deliver pressurised air, typically through a nasal mask, to prevent collapse of the upper airway during sleep. Since the development of CPAP, Resmed have developed a number of innovative products for SDB and other respiratory disorders including airflow generators, diagnostic products, mask systems, headgear and other accessories. Its growth has been fuelled by geographic expansion, increased awareness of respiratory conditions as a significant health concern among physicians and patients, and its research and product development efforts. Resmed employ approximately 3,900 people and sell its products in approximately 100 countries through a combination of wholly owned subsidiaries and independent distributors.

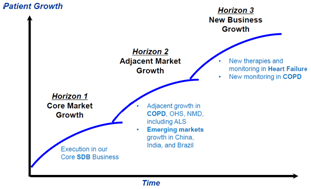

Resmed’s growth strategy has three stages – core market growth, adjacent market growth and new business growth.

Figure 1 Resmed growth strategy (Source: Company Reports)

Core market growth pertains to ongoing innovation in developing products for the diagnosis and treatment of SDB. Resmed management believes that continued product development and innovation are key factors to its ongoing success. Approximately 15% of its employees are devoted to research and development activities. In fiscal year 2013, it invested $120.1 million, or approximately 8% of net revenues, in research and development. This investment in research and development also provides opportunities for the second and third stages of its growth strategy.

The second stage of growth is about expanding geographic presence. Resmed market its products in approximately 100 countries to sleep clinics, home healthcare dealers and third-parties. Management intends to increase sales and marketing efforts in principal markets, as well as expand presence in other geographic regions.

The third tier is largely about using existing capabilities and internally developed technologies and creating new products and applications with them for significant unmet medical needs. For example, studies have established a clinical association between OSA and both stroke and congestive heart failure, and have recognised SDB as a cause of hypertension or high blood pressure. Research also indicates that SDB is independently associated with glucose intolerance and insulin resistance. Resmed have developed a device for the treatment of Cheyne-Stokes breathing in patients with congestive heart failure.

The case against…

Trading at 18 times next year’s earnings may indicate the market is sanguine about earnings growth, but as value investors we see a business, that still has some shortcomings, priced for perfection.

The markets for Resmed’s SDB products are highly competitive and are characterised by frequent product improvements and evolving technology. Its ability to compete successfully depends, in part, on its ability to develop, manufacture and market innovative new products. The development of innovative new products by Resmed’s competitors or the discovery of alternative treatments or potential cures for the conditions that our products treat could make its products non-competitive or obsolete. Current competitors, new entrants, academics, and others are trying to develop new devices, alternative treatments or cures, and pharmaceutical solutions to the conditions Resmed’s products treat. Additionally, some of its competitors have greater financial, research and development, manufacturing and marketing resources than Resmed does. The past several years have seen a trend towards consolidation in the healthcare industry and in the markets for its products. Industry consolidation could result in greater competition if Resmed’s competitors combine their resources, are acquired by other companies with greater resources, or become affiliated with its customers. This competition could increase pressure on Resmed to reduce the selling prices of our products or could cause it to increase its spending on research and development and sales and marketing. If Resmed are unable to develop innovative new products, maintain competitive pricing, and offer products that consumers perceive to be as good as competitors, its sales or gross margins could decrease.

Chart view

RMD has been trending well for nearly two years now but last week saw it drop quite dramatically on large volume. This shock move will result in some sort of correction for RMD, whether that be in price or time. By “time”, we mean that it could potentially drift sideways for a while. That would be similar to the price action earlier this year where the share price dropped at the end of January but instead of pulling back, it drifted sideways for a few months before resuming the uptrend. Alternatively, given the lacklustre strength in the last few days, we could potentially see it fall under $5.20 support which means that it could be heading to under $4.80. That is the point where it could be finishing its correction in price and would see RMD trading at a more attractive PE level.