Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, economic activity trackers, major global economic events and Australian economic events.Investment markets and key developments over the past week- Most share markets rose again over the last week as the Fed finally pivoted towards rate cuts and numerous central banks left rates on hold. As a result, for the week US shares rose 2.5%, Eurozone shares rose 0.8% and Japanese shares gained 2.1%. Chinese shares fell 1.7% on ongoing concerns about Chinese growth and its property sector. The US share market is now just 1.6% below its record January 2022 high which had been reached before the inflation and interest rate scare took off in earnest. The positive global lead and the flow on from the Fed’s pivot to expectations for RBA rate cuts next year saw the Australian share market surge 3.4% for the week with property, IT, material and health stocks leading the charge. This has substantially improved its year-to-date gain to a respectable 5.7%, although it still remains a relative underperformer. Bond yields fell further on the back of falling interest rate expectations for next year and they are nearly back to where they started 2023. The oil price rose slightly as did metal prices, but the iron ore price fell slightly. The $A rose to around $US0.67 as the $US fell.

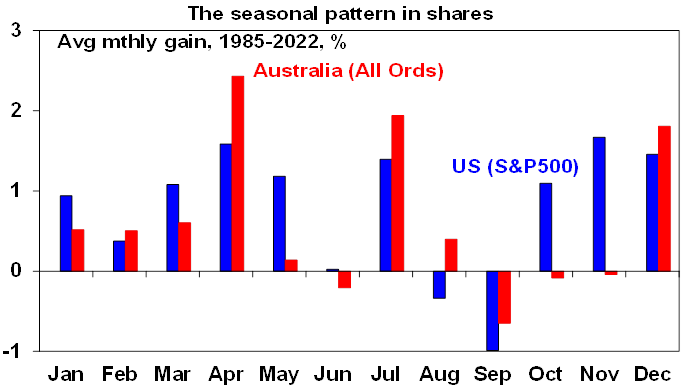

- Shares remain vulnerable to concerns about sticky inflation, recession fears, worries about the Chinese economy and geopolitics but they are likely to see more upside in the months ahead as inflation continues to ease, the monetary policy environment turns progressively less threatening and then more supportive and positive share market seasonality remains in place with the Santa Rally normally kicking in from about now. So, while we should expect lots of bumps along the way our base case remains that global and Australian shares can trend up.

- Out of interest the Santa rally normally kicks in around mid-December on the back of festive cheer and new year optimism, the investment of any bonuses, low volumes and no capital raisings at this time of year. Over the last 15 years the period from mid-December to year end has seen an average gain of 0.7% in US shares with shares up in this two-week period 10 years out of 15. In Australia, over the last 15 years the average gain over the last two weeks of December has been 1.4% with shares up 10 years out of 15. It has tended to be weaker or less reliable in years when the market is down year to date though.

Source: Bloomberg, AMP

Source: Bloomberg, AMP- More good news on interest rates, with key central banks leaving rates on hold and the Fed pivoting towards interest rate cuts. The past week saw a raft of central banks – the Fed, the ECB, the BoE along with central banks in Switzerland, the Philippines and Taiwan – all leave interest rates on hold. The Norwegian central bank surprisingly raised rates but signalled that rates are now likely on hold. And the Brazilian central bank cut rates. It’s now looking almost certain that rates have peaked in major central banks and they are moving towards rate cuts. This is all being driven by the ongoing fall in inflation, with US CPI inflation falling again in the last week and a bigger than expected fall in producer price inflation. Of course, some central banks are moving faster than others. In particular:

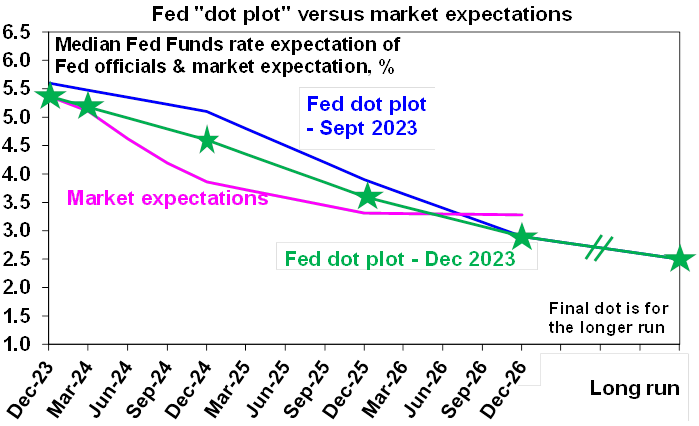

- The Fed is the most dovish arguably reflecting the fact that its inflation rate peaked in June 2022 which was several months ahead of other countries (October 2022 for the Eurozone and UK and December 2022 in Australia) and so its seen a longer period of slowing. It held rates at 5.25-5.5% as expected but has become dovish in noting that growth and inflation have slowed, is now referring to what will determine “any” additional tightening, has started to discuss rate cuts and its dot plot of Fed officials’ interest rate forecasts is now allowing for three rate cuts next year. We expect the Fed to start cutting interest rates in the June quarter.

Source: Federal Reserve, AMP

Source: Federal Reserve, AMP- The ECB held rates at 4.5% and moved to be a bit less hawkish with President Lagarde dropping guidance that it would not cut rates in the next two quarters but sounding more hawkish than expected and unlike the Fed is yet to discuss rate cuts. Quite clearly the ECB is a bit concerned that market expectations for rate cuts have moved too quickly and it wants to damp it down. That said, with the Eurozone in or close to a mild recession and inflation likely to fall further we see it starting to cut rates in April.

- The BoE held at 5.25% and was understandably a bit more hawkish given its higher inflation rate and wages growth above 7%yoy. However, with the economy weakening and inflation likely to slow further its likely to start cutting around mid-2024.

- The peaking in global interest rates and shift towards rate cuts led by the Fed is a good sign for the RBA. Just as Australian inflation and interest rates lagged the pickup in US/global inflation and interest rates by a few months its likely to also do the same on the way down. So the fact that the US is moving towards rate cuts suggests that the RBA will likely do the same with a lag. While there is still a high risk of another RBA rate hike early next year, its likely to be headed off by weaker inflation for December and the pivot towards rate cuts globally. Our base case remains that the cash rate has peaked and that the RBA will start cutting rates mid next year taking the cash rate down to 3.6% by end 2024 (which is below market expectations for a fall in the cash rate to 3.8% by end 2024).

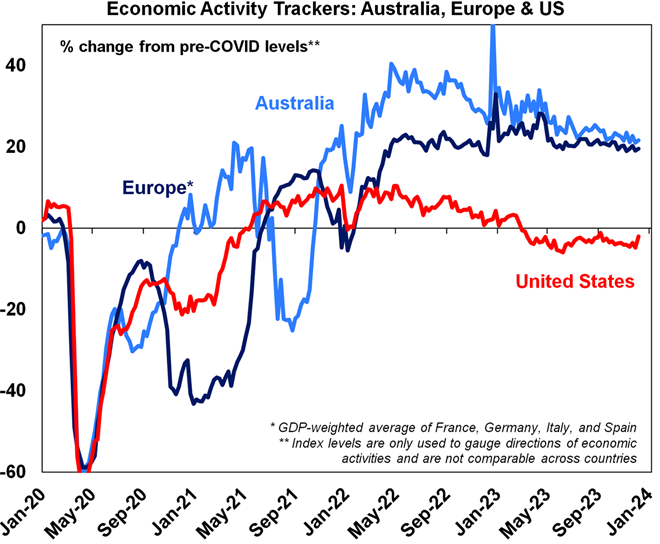

Economic activity trackers- Our Economic Activity Trackers are still not showing anything decisive for the direction of economic activity – although the US Tracker picked up a bit in the last week.

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence and credit & debit card transactions. Source: AMPMajor global economic events and implications

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence and credit & debit card transactions. Source: AMPMajor global economic events and implications- Global economic data over the last week remained consistent with soft growth and falling inflation. December developed country composite business conditions PMIs rose slightly but remained weak at an average 49.6. Price indicators also rose slightly but remain well down from their highs.

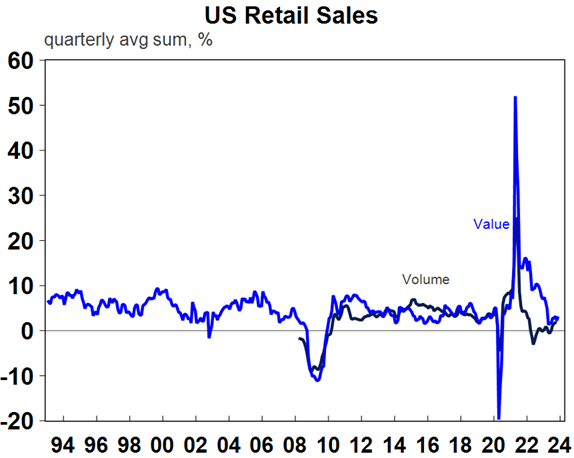

- US economic data was mixed. Retail sales were stronger than expected but the previous month was revised down. Industrial production rose less than expected but with the previous month revised to a fall of 0.9%. The composite PMI for December rose slightly but is still relatively soft, manufacturing conditions fell sharply in the New York region and small business optimism remained weak. Initial jobless claims fell but continuing claims rose.

Source: Macrobond, AMP

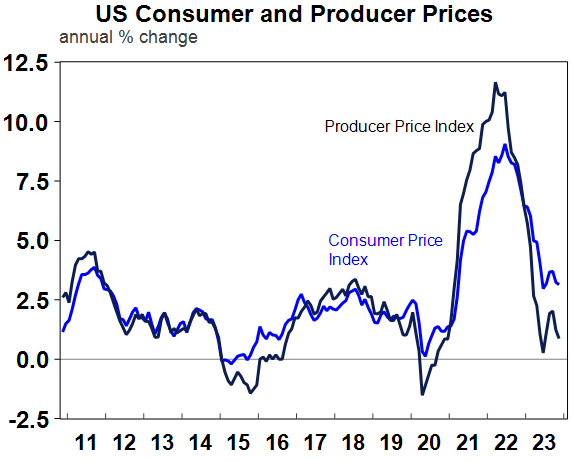

Source: Macrobond, AMP- US November consumer price inflation came in roughly in line with expectations falling to 3.1%yoy with core inflation unchanged at 4%yoy. While core services excluding shelter inflation is still a bit sticky slowing wages growth points to a slow down in it too. Falling producer price inflation also points to a further fall in CPI inflation & suggests November core private final consumption deflator inflation (which the Fed targets) will be soft with the six month pace actually running at or below the Fed’s 2% target.

Source: Macrobond, AMP

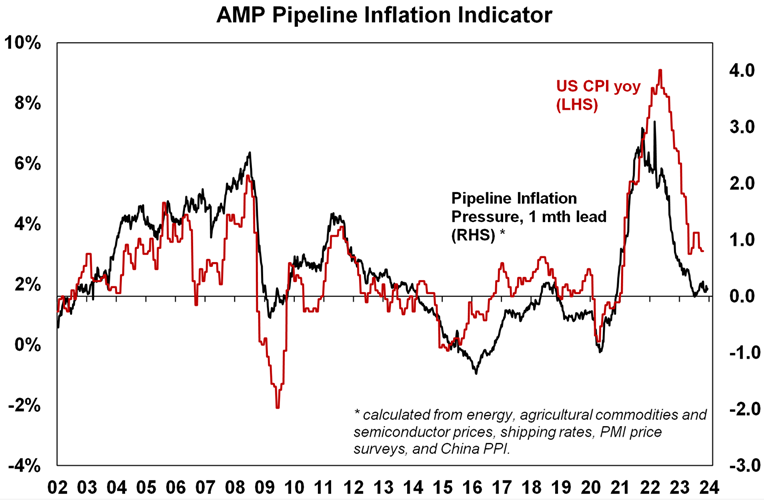

Source: Macrobond, AMP- Our Pipeline Inflation Indicator for the US continues to point to a further fall in inflation.

Source: Bloomberg, AMP

Source: Bloomberg, AMP- Eurozone industrial production fell again in October and is down 6.6%yoy, highlighting the softness in the Eurozone economy as did a further fall in the composite PMI for December to a weak level of 47.

- UK jobs data was soft in November with employment down and wages growth slowing to 7.2%yoy (from 8%), easing concerns about services inflation, although the BoE remains cautious.

- The Japanese Tankan business survey showed improvement but conditions are expected to slow a bit in the current quarter. The composite business conditions PMI also improved slightly in December. Producer price inflation slowed further to 0.3%yoy in November. No BoJ tightening signal here!

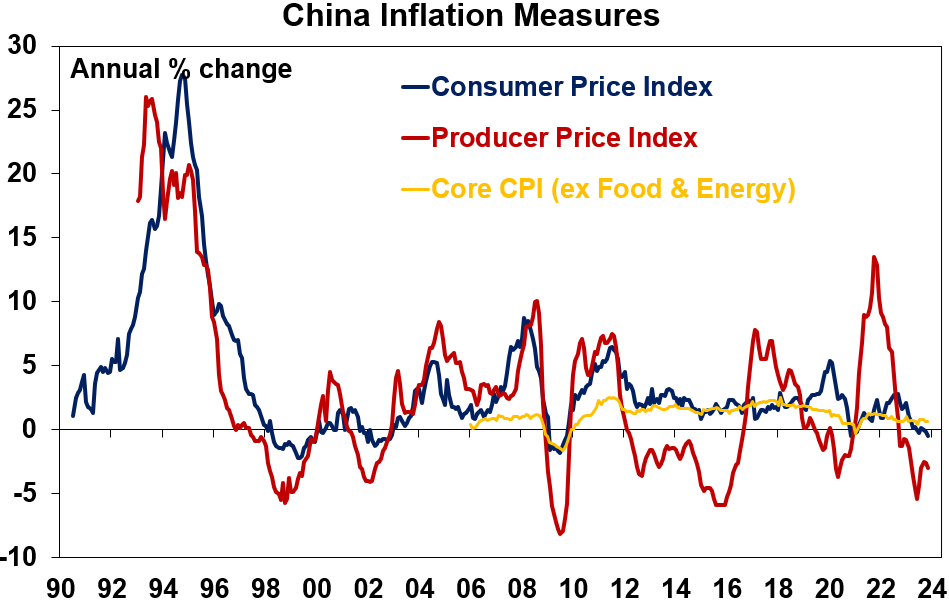

- China not rushing into a big fiscal stimulus. The Central Economic Work Conference maintained a pro-growth tone but with a focus on quality growth. On the data front, Chinese activity indicators for November were mixed with industrial production and retail sales accelerating from a year ago due to base effects from last year’s lockdowns with production stronger than expected but retail sales weaker than expected, investment growth remaining subdued and property investment and sales still falling. Home prices are continuing to fall and credit was weaker than expected but annual credit growth accelerated to 9.4%yoy, from 9.30%.

- China slipped further into deflation in November but note that core inflation was unchanged at 0.6%yoy.

Source: Bloomberg, AMP

Source: Bloomberg, AMP- New Zealand economy contracting under the weight of high interest rates. GDP contracted 0.3% in the September quarter and is down 0.6%yoy. Expect weak economic conditions and falling inflation to see the RBNZ starting cutting rates in the June quarter.

Australian economic events and implications- Australian economic data over the last week was a mostly consistent with slowing growth, easing inflation and the RBA having peaked on rates.

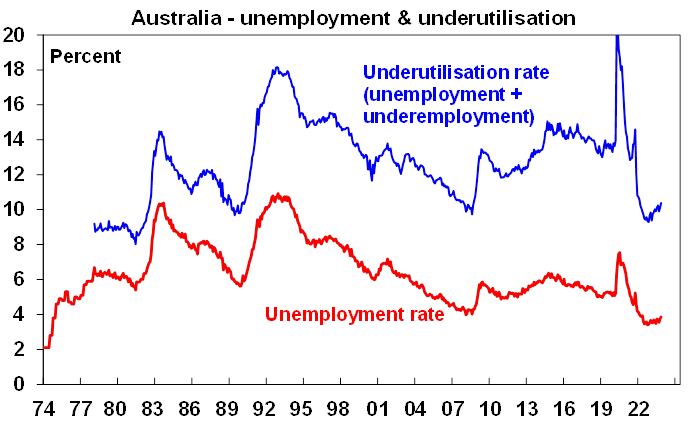

- Still rising unemployment. Jobs growth was way stronger than expected in November, but against this unemployment and underemployment rose on the back of a record participation rate and are continuing to gradually trend up, hours worked were flat and have been trending down over the last six months all of which suggests softness.

Source: ABS, AMP

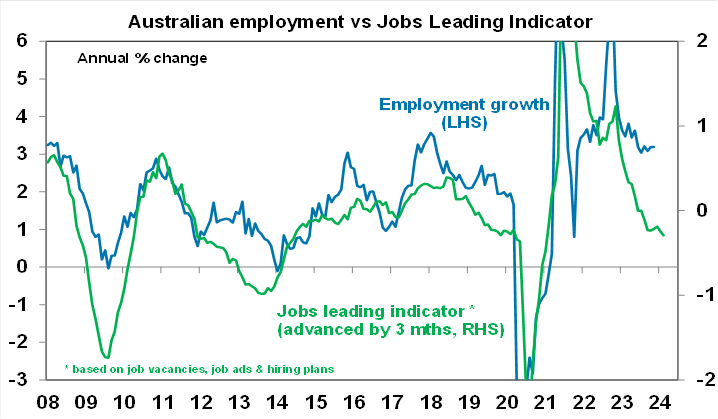

Source: ABS, AMP- And our Jobs Leading Indicator continues to point to slower jobs growth ahead on the back of falling vacancies and hiring plans. Given the surging population more than 30,000 new jobs are required each month to stop unemployment rising and the Jobs Indicator suggests we will soon fall below that.

Source: ABS, AMP

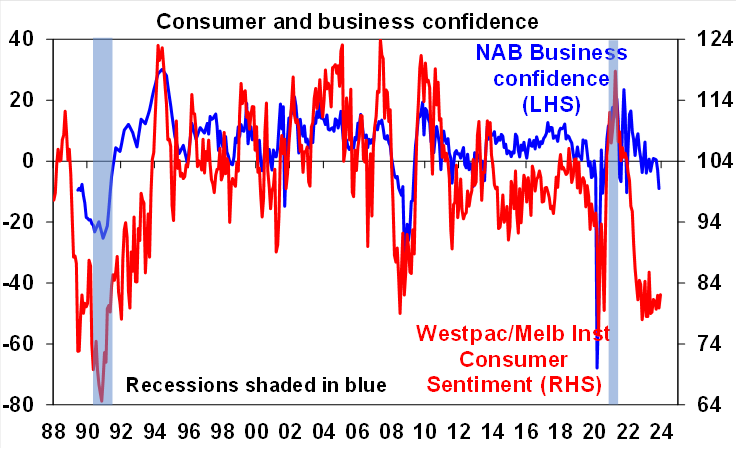

Source: ABS, AMP- Confidence remains weak. Consumer confidence rose slightly in December on the RBA rate pause but remains depressed and business confidence in the NAB survey fell, albeit business conditions are still okay but also falling. All things being equal this is consistent with soft growth.

Source: NAB, Westpac/MI, AMP

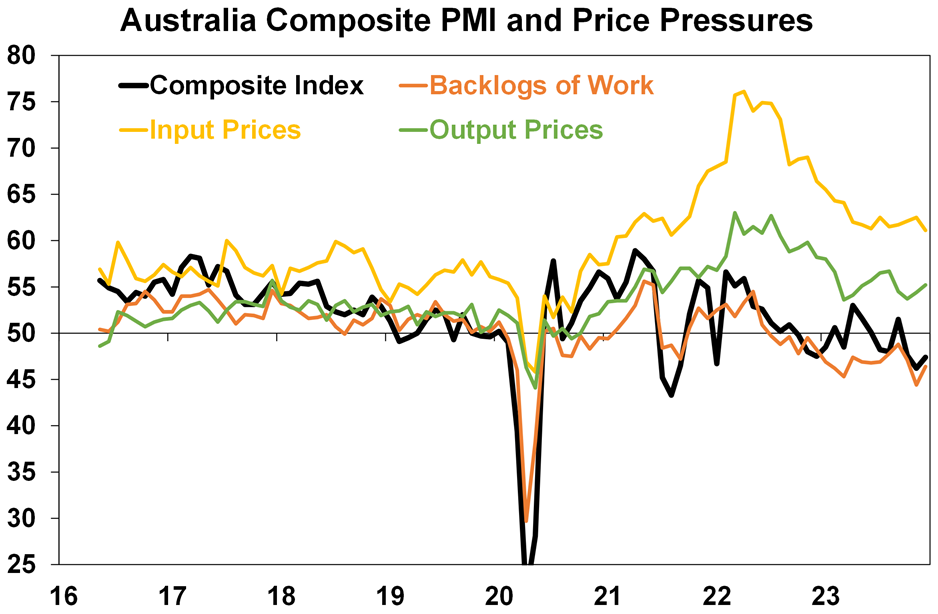

Source: NAB, Westpac/MI, AMP- The business conditions PMI for December improved slightly but remain weak, with depressed new orders. Price and cost indicators remain well down from their highs but are still a bit elevated and work backlogs are weak.

Source: Bloomberg, AMP

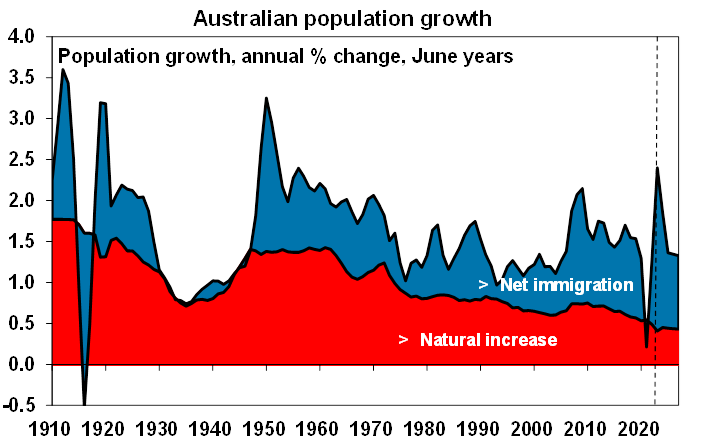

Source: Bloomberg, AMP- Strongest population growth since 1956. Australia’s population rose by 2.4% in 2022-23 its fastest pace since 1956, driven by record immigration of 518,000 people with students on 1 year or more visa’s being a big driver. This is way above the 180,000 net migration forecast at the time of the March 2022 Federal Budget. The surge in immigration may have helped support the economy and ease labour shortages but its done nothing to boost per capita GDP (which is in recession) and has added to demand and hence inflation and likely led to higher than otherwise interest rates. The strains are most evident in the housing shortfall which has contributed to surging rents and record home prices.

Source: Melbourne Institute, AMP

Source: Melbourne Institute, AMP- We may be at peak immigration but the housing shortfall will still worsen. Monthly arrivals data suggests that net migration may be at or close to peaking and helped by a tightening in visa requirements the Government is now forecasting a slowing to 375,000 this financial year and 250,000 in 2024-25. However, this is still above the pre-covid average of 230,000 a year and given constrained home building will mean that the shortfall of houses in Australia will likely rise to around 170,000 by June next year.

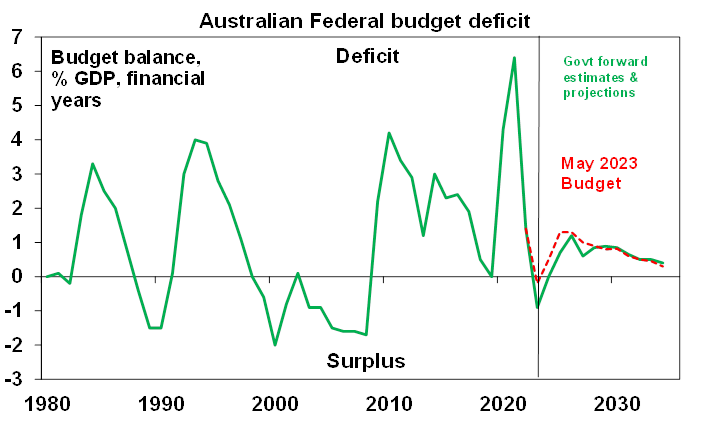

- On track for another budget surplus. The Government’s mid year review confirmed a further improvement in budget projections with the deficit for this year now projected to be just $1bn down from $14bn back in May thanks to stronger personal and company tax collections. Monthly budget data suggests that this could turn into another surplus. Its good to see the Government largely saving its revenue windfall as it will help take pressure off inflation by taking money out of the economy, but spending is still projected to grew rapidly and this partly works in the opposite direction. Meanwhile the rapid growth in tax revenue highlights the ongoing issue of bracket creep and hence the case for the Stage 3 tax cuts, although ideally the tax brackets should be indexed to wages growth.

Source: Federal Treasury, AMPWhat to watch over the next three weeks?

Source: Federal Treasury, AMPWhat to watch over the next three weeks?- In the US, expect a rise in home builder conditions (18 Dec), weaker housing starts (19 Dec), a rise in consumer confidence (20 Dec), soft underlying durable goods orders and a further fall in core PCE inflation (22 Dec), continued softness in the manufacturing ISM and falls in job openings (both 3 Jan), further softening in payroll jobs growth (5 Jan) and a slowing December CPI (11 Jan).

- In Europe, expect continued softer inflation (5 Jan).

- The Bank of Japan (19 Dec) will probably leave rates on hold as wages growth is still too low, but it will likely signal that it’s getting close to rate hikes. Japanese inflation (22 Dec) is likely to fall to 2.8%yoy but with core inflation unchanged at 2.7%.

- Chinese December trade and inflation data will be released on 8 January, with prices likely to remain in deflation.

- In Australia, the minutes from the last RBA meeting (Tuesday, 19 Dec) will likely reiterate the RBA’ concerns about still high services inflation, inflation expectations and the tight labour market but also indicate that whether rates go up again will depend on global developments, jobs, consumer spending and inflation data to be released before the February meeting. Our view is that lower December quarter inflation data and growing evidence of softer economy will head off another rate hike, albeit the risk is still high. On the data front credit growth (29 Dec) is likely to remain soft, Core Logic data for December (2 Jan) is likely to show a further slowing in home price growth to 0.4%mom with prices up 8.3% for the year, November retail sales (9 Jan) are likely to bounce on the back of Black Friday and Cyber Monday sales, the November CPI Inflation Indicator is likely to slow to 4.6%yoy (from 4.9%) as high year ago increases drop out and job vacancies for November are likely to show another fall (both due on 11 Jan).

Outlook for investment markets for 2024- Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025 should make for okay investment returns in 2024. However, with growth still slowing, shares historically tending to fall during the initial phase of rate cuts, a very high risk of recession and investors and share market valuations no longer positioned for recession, it’s likely to be a rougher and more constrained ride than in 2023.

- Global shares are expected to return a far more constrained 7%. The first half could be rough as growth weakens and possibly goes negative and valuations are less attractive than a year ago, but shares should ultimately benefit from rate cuts, lower bond yields and the anticipation of stronger growth later in the year and in 2025.

- Australian shares are likely to outperform global shares, after underperforming in 2023 helped by somewhat more attractive valuations. A recession could threaten this though so it’s hard to have a strong view. Expect the ASX 200 to return 9% in 2024.

- Bonds are likely to provide returns around running yield or a bit more, as inflation slows and central banks cut rates.

- Unlisted commercial property returns are likely to be negative again due to the lagged impact of high bond yields & working from home.

- Australian home prices are likely to fall 5% as high interest rates hit demand again and unemployment rises. The supply shortfall should prevent a sharper fall & expect a wide dispersion with prices still rising in Adelaide, Brisbane & Perth. Rate cuts later in the year will help prices bottom and start to rise again.

- Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

- A rising trend in the $A is likely taking it to $US0.72, due to a fall in the overvalued $US & the Fed moving to cut rates before the RBA.

- Eurozone shares rose 0.1% on Friday and the US S&P 500 was flat, as investors digested the strong gains already seen through the week and some Fed officials pushed back against the speed with which the market expects the Fed to start cutting rates.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.