Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the cash rate.

Key points:- The RBA left its cash rate on hold at 4.1% for the fourth month in a row.

- This was in line with our own forecast, the consensus of economists and the money market’s expectation.

- The decision to hold is consistent with more signs of weakness in the jobs market and consumer spending in the last month, a continuing downtrend in inflation and the significant rise in interest rates that has already occurred.

- That said the RBA is again likely to have considered the case for another hike and it retained its tightening bias given still high inflation and the still tight labour market, albeit it remains data dependent.

- Our concern remains that the RBA may have tightened more than necessary with a high (50%) risk of recession.

- As a result, while the risk is still on the upside for the cash rate in the short term with 40% chance of another hike by Christmas, the RBA probably won’t have to act on its tightening bias, and we continue to see it cutting rates through next year starting around June.

The RBA’s post meeting statement under new Governor Michele Bullock is little changed – apart from updating for recent inflation and growth data – from former Governor Lowe’s last statement indicating that continuity is the name of the game so far with respect to interest rate setting.

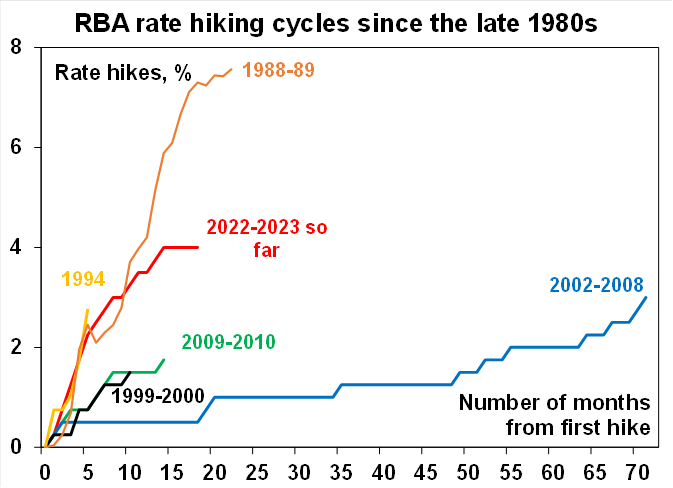

The pause in interest rates over the last four months comes after the biggest interest rate hiking cycle (of 400 basis points over 14 months) since the late 1980s which preceded the early 1990s recession. The risks to the household sector are much higher now because household debt to income levels are three times greater than they were in the late 1980s. The rise in interest rates has taken mortgage rates back to levels last seen in 2011, which for many who were on fixed rates means a three-fold or greater increase in their mortgage rate.

Source: RBA, AMP

In leaving the cash rate on hold at 4.1%, the RBA noted again that: interest rates have already been increased by 4%; higher rates are working to establish a “more sustainable balance between supply and demand”; uncertainty remains high, and staying on hold provides further time to assess the outlook.

Leaving rates on hold again is consistent with the combination seen over the last month of softening full time jobs growth, falling job vacancies and increasing evidence that consumer spending is flagging with rising mortgage stress, sharply falling real per person retail sales and households starting to dip into their bank deposits. The RBA reiterated that recent data are consistent with inflation returning to target in late 2025, but we continue to think it will be earlier.

The RBA is concerned though that: inflation is still too high with sticky services inflation; fuel prices are up noticeably; the labour market remains “tight”; and productivity needs to pick up. In addition to this, although not noted by the RBA, newly lodged enterprise bargaining agreements point to a possible acceleration in wages growth beyond the 4% level seen as consistent with the 2-3% inflation target.

As a result, the RBA probably again considered raising rates (as it has in the last few meetings before deciding to hold) and it retained its guidance that “some further tightening of monetary policy [ie rate hikes] may be required to ensure that inflation returns to target in a reasonable timeframe”. It also reiterated that this will depend on how the data evolves and that it will continue to look closely at the global economy, household spending, inflation and the labour market.

On balance, the RBA is continuing to give more weight to the downside risks to the economic outlook flowing from the lags with which monetary policy impacts the economy and uncertainties around household spending. And it also continued to indicate concerns around the Chinese economy.

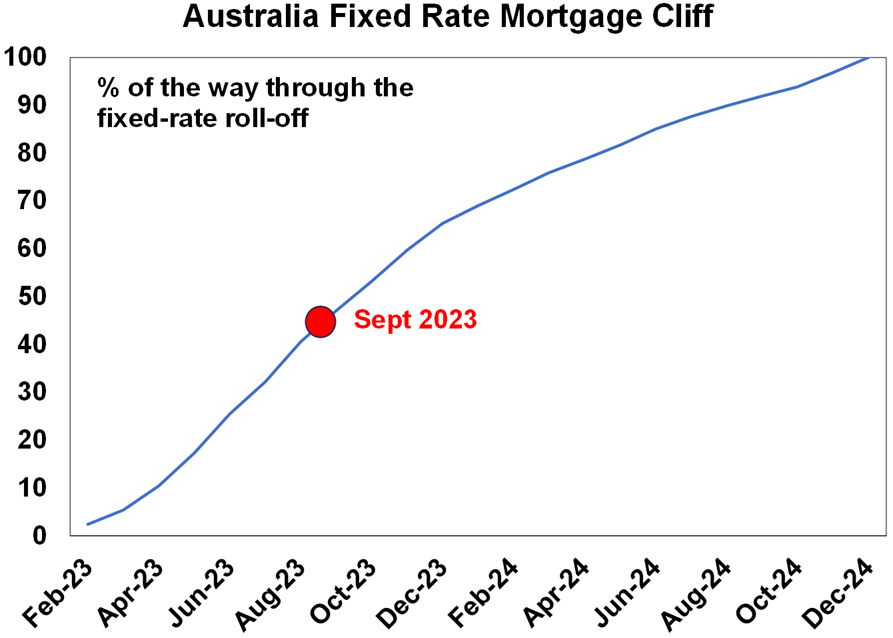

Even though rates were left on hold, the rate hikes since May last year mean that a variable rate borrower with a $600,000 mortgage will have seen $1300 a month added to their mortgage payments. That’s an extra $15,700 a year. Even if the borrower has managed to get a 0.5% discount to their mortgage rate it would amount to an extra $13,300 which is a big ongoing hit to household spending power even if interest rates have stopped rising. Many of those on fixed rates are now starting to experience that increase now in one jump. And so far, we are only around 40% of the way through the transition from the low 2% or so fixed rates taken out through the pandemic and its immediate aftermath. The rise in mortgage rates is pushing debt servicing costs into record territory as a share of household disposable income.

Source: RBA, ABS, AMP

We would concede that the near-term risk of another rate hike is still high particularly with still high inflation, the risk that higher petrol prices will add to inflation expectations and signs of a pickup in wages growth. Economists seem to be split roughly 50/50 as to whether there will be another rate hike or not and our assessment is that the risk is around 40%. If new Governor Bullock is to raise rates again though she is likely to wait to see the September quarterly CPI and updated RBA forecasts which will both be available by the November meeting and possibly September quarter wages data (due in mid-November) which could take us to the December meeting.

However, we would view another rate hike as a mistake as the RBA has already done more than enough to slow the economy in order to rebalance demand and supply and bring inflation back to target. Rate hikes impact the economy with a long lag as it takes a while for the hikes to be passed through to borrowers and for them to adjust their spending. This time around the lag has been lengthened by savings buffers built up in the pandemic, the reopening boost, more than normal home borrowers locking in at 2% of so fixed mortgage rates in the pandemic and the highly competitive mortgage market which has meant that actual mortgage rates paid on outstanding mortgages have gone up by less than the cash rate. However, these protections are now wearing off.

We are now seeing increasing evidence that rate hikes are biting with real per person retail sales down 4.5% or so on a year ago, the ABS’ Household Spending Indicator indicating a fall on a year ago, a sharp fall in building approvals from their highs, slowing business investment plans, a slowdown in GDP growth, rising insolvencies, increasing indications of a slowing jobs market and combined this is likely to continue to bear down further on inflationary pressures. Against this background the rise in petrol prices which will add roughly $11 a week to a typical households fuel bill is more likely to act as a tax on spending rather than as a further impetus to underlying inflation.

Continuing to raise interest rates will only add to the already very high risk of unnecessarily knocking the economy into recession. At the very least the economy is likely to have slowed substantially by early next year with unemployment starting to rise faster than the RBA is allowing for.

So while the risk of another rate hike in November or December remains high, our base case remains that rates have peaked and that the cash rate will be cut next year with the first cut coming around June (which we pushed out from March a few weeks ago). Given the lags involved and the increasing signs that monetary tightening is working it makes sense for the RBA to remain on hold so it can better assess the impact of the rate hikes so far.

With former Governor Lowe having increased interest rates substantially, new Governor Michele Bullock should get a much easier run of it on interest rates. The risk is that her main challenge will be trying to turn the economy back up again in the event of a hard landing or recession.

EndsImportant note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.