By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

- Uncertainty around the duration of the US/Israel war with Iran has intensified with oil prices spiking to $US119/barrel only to then plunge as President Trump hinted that the war may be close to over. This is in turn driving big gyrations in investment markets.

- While a limited war remains more likely than a long war, it could still push oil prices higher & shares lower in the near term. Trump may be getting close to an off ramp though.

- For the RBA, there is a strong case to wait till May on rates as the boost to inflation could prove temporary.

Introduction

Oil and investment markets initially reacted relatively calmly to the US/Israel war with Iran, despite the Strait of Hormuz through which 20-25% of global oil and gas supplies flow through on a daily basis being closed from the get go. However, as the war has continued with the Strait remaining effectively closed uncertainty has intensified. Coming into the second week of the war oil prices surged to $US119 as the pace of Iranian drone and missile attacks on its neighbour stepped up again, Iran’s decision to replace Ayatollah Ali Khamenei with his son suggested it’s not in a rush to surrender, as various Gulf countries shut oil and gas production and Trump downplayed the surge in oil prices as “a very small price to pay.” They then plunged back to around $US83 as Trump hinted the war could be over “very soon” noting that it was “very complete, pretty much”. But uncertainty remains high as he also said he did not believe it would be over this week and that he would “not relent until the enemy is totally and decisively defeated.” So oil prices then bounced back to around $US89 at the time of writing. Gas prices in Europe are also up around 80% since the war started. Bond yields have increased on worries about a boast to inflation. And from this year’s highs to recent lows US shares have had a fall of around -2.5%, Eurozone shares -8%, Japanese shares -10% and Australian shares -6.5% on the back of worries about a hit to growth. This note provides a Q&A around the key issues.

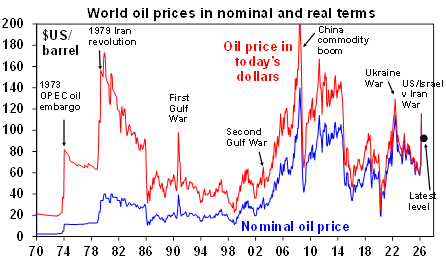

How high will oil prices go?

With their spike yesterday oil prices roughly doubled from their lows early this year taking them back to their highs around the start of the Ukraine War. The 1973 OPEC oil embargo saw a fourfold increase in prices (albeit from a much lower base even in today’s dollars) and the second oil shock in 1979 saw a threefold increase. Both reflected supply cuts with the second shock seeing a 5% hit to supply on the back of the Iranian revolution. While Trump has made assurances about reopening the Strait of Hormuz at present its still effectively shut, meaning a 20-25% hit to global oil and gas supplies. An optimistic take is that this may be reduced to a 15-20% supply hit if various pipelines can be used. But with global oil demand being relatively inelastic in the short term such a supply setback risks pushing the oil price to say $US150-200/barrel the longer the supply disruption persists as inventories run down. Reports of a release from the G7 oil reserves if realised may provide relief but it will only be temporary if the war and oil disruption continues.

Source: Bloomberg, AMP

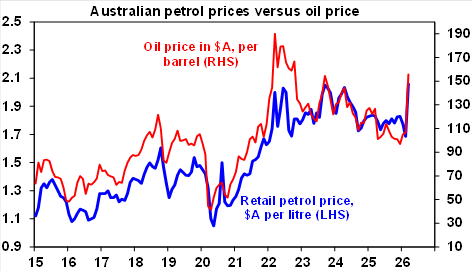

What is the flow on to petrol prices?

In Australia, each $US1 a barrel rise in oil prices roughly adds around a cent a litre to petrol prices. So, if the oil price settles around $US100 for a while it would mean a rise of $US40-50 from January lows and roughly a 40-50 cents per litre rise in petrol prices. This would normally take 7-10 days to fully show up but petrol prices have already moved up partly due to the normal discounting cycle in some cities and a catch up to the rise that occurred prior to the war starting.

Source: Bloomberg, AMP

What is the threat to growth?

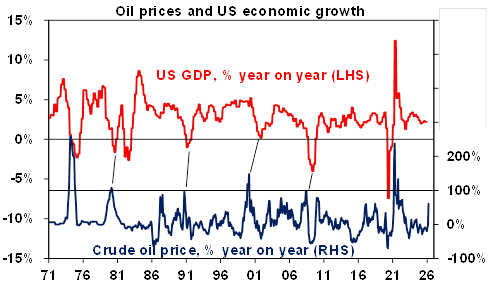

Higher oil and gas prices will depress economic activity because they act like a tax on businesses and consumers leaving less money to spend elsewhere in the economy. Past oil price surges have played a role in US & global downturns. As can be seen in the next chart, the threat becomes significant once oil prices double – which they have come close to doing since the start of the year with yesterday’s spike, although not if measured from a year ago.

Note: the relationship between oil prices & GDP looks messy over 2020/2021 as oil prices crashed with the pandemic and then rebounded into 2021 but were still low. Source: Bloomberg, AMP

A 60 to 70% decline in the oil intensity of GDP since the 1970s thanks to energy efficiencies and the bigger services sector across the US, global and Australian economies mean their impact will be less than it used to be. Rough estimates by Goldman Sachs indicate that a spike in oil prices spike to around $US100/barrel will knock around 0.4% off global growth over the year ahead. With Europe and Asia (which are net energy importers) more affected than the US (as the US is a net energy exporter).

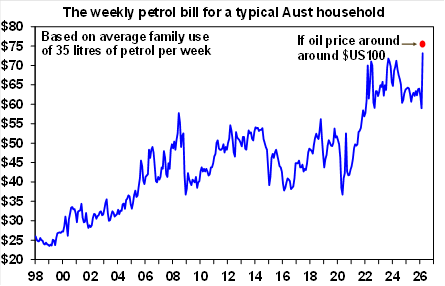

While Australia is also a net energy exporter it is likely to see a similar sized hit to growth as a result of weaker consumer and business confidence and as higher petrol prices lower household disposable income. Our rough estimate is that oil prices around $US100 and the flow on to petrol prices will cost the average Australian household an extra $14 a week or $730 a year, which will lower their ability to spend. At the same time consumer confidence readings taken late last week as the war intensified show a sharp 7% plunge which will likely depress spending.

Source: Bloomberg, AMP

What is the impact on inflation?

Our rough estimate is that oil around $US100/barrel will directly add around 0.8% to inflation in Australia, pushing it up to around 4.6%yoy. There may be another 0.1-0.2% added due to higher transport costs and a flow on to goods like fertiliser and plastics that use oil but this may be offset in terms of underlying inflation by the impact of weaker spending in the economy reducing underlying pricing power.

What does it mean for interest rates in Australia?

For the RBA, the implications are ambiguous but with a bias to higher rates. The case for higher rates is that inflation is already above target and a further big boost to headline inflation to above 4% will threaten higher inflation expectations making it even harder for the RBA to get inflation back down. These concerns likely explain RBA Governor Bullock’s more hawkish tone last week. The case to hold is that the boost to inflation may be brief if the War ends in the next few weeks and the negative impact on demand in the economy could lead to lower underlying inflation.

On balance we expect the RBA to wait till May before deciding what to do on rates, but to sound hawkish in the interim.

Why have share markets fallen?

Shares have fallen because the surge in oil prices is threatening a negative combination of higher inflation, bond yields and potentially central bank rate hikes on the one hand and lower economic growth and profits on the other. This has also come at a time of increased uncertainty around the disruptive impact of AI and stretched valuations. So, shares were vulnerable to a pullback, and the war may have provided the trigger. We have been of the view that while global & Australian shares will have okay returns this year, they are likely to have a 15% or so correction on the way.

Why is the $US up and the $A down (a bit)?

Consistent with the risk off tone the $US is up (because it’s a net oil and energy exporter) particularly against the Euro (which is a net energy importer). The $A is down because of fears about global growth but it has held above $US0.70 because while it’s a net oil importer it’s a net energy exporter and will benefit from higher gas prices and because the RBA is still expected to raise rates whereas the Fed is still expected to cut rates.

How long will the war last and oil supplies remain disrupted?

This is the key issue. Trump is under big pressure to keep it short and avoid troops on the ground – polls show little support in the US for this War (around 27%), compared to 70% or more for Iraq I and II and Afghanistan, most of his MAGA base was motivated by a desire to stay out of wars and surging gasoline prices will go down badly into the midterm elections. And it could be argued that the US is at or close to success on several of its four stated goals which are:

- Dismantling Iran’s missile forces – close.

- Destroying its navy – done.

- Stopping its nuclear weapons development – largely done.

- Cutting of its regional terrorist groups – to be seen.

This suggests that Trump may be getting close to finding an off ramp. Hence his comments that the war may be close to over. So our probabilities on the two key scenarios remain:

Limited war (60% probability) – given these considerations our base case is that the war is limited with Trump likely finding a way to declare victory sometime in the weeks ahead. This may still take a few more weeks so oil prices could still go higher (seeing further falls in shares) before they go lower (shares higher). This would ultimately be a selling opportunity in oil and a buying opportunity in shares. Trying to time it will be hard though.

Long war (40% probability) – however, while Trump may want to declare victory soon, Iran may not play ball and has an incentive to prolong the surge in oil prices and hence the cost to Trump and US consumers. So far it’s not playing ball, with a defiant new leader. Iran could also descend into chaos with various military groups continuing to threaten ships in the Strait of Hormuz. This could necessitate a longer-term US involvement and mean a much longer disruption to oil, conceivably resulting in oil prices going to $US150 & beyond driving a sharp sustained fall in shares.

Key to watch for will be a sustained fall in missiles & drones coming from Iran, indications Iran wants to negotiate and a 10% or more top to bottom fall in US shares which may up pressure on Trump to find a way out.

What should super members do?

While no one likes to see their wealth go backwards, periodic setbacks are an inevitable aspect of investing. Given the difficulties in trying to time markets, the key for investors is to stick to an appropriate long-term investment strategy.