The rand has had a good year so far in 2016 following the turmoil seen last December in the wake of the ‘Nenegate’ scandal. However, politics is again threatening to derail the rally, and the longer-term trend continues to be a weakening against the dollar.Since December 2015’s brutal depreciation of the rand following the surprise shift in South Africa’s Finance Ministers in what’s become known as the Nenegate scandal, the rand has been on a steady path to recovery in 2016.

However, news that South Africa’s Finance Minister Pravin Gordhan might be facing a possible arrest by the “Hawks” (Directorate for Priority Crime Investigation), as well as a new forensic investigation relating to his tenure at the South Africa Revenue Service (SARS) has provided a domestic catalyst for renewed short-term weakness for the rand.

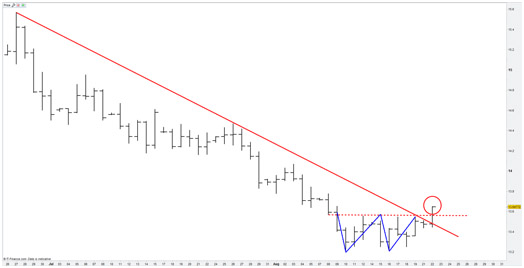

Ironically, or coincidently, the chart snapshot taken on 22 August showed a forewarning that the rand (in dollar terms) had formed a “w” shaped reversal pattern. The pattern (in the below context) suggests a short-term change in directional trend from that of strength to one of weakening.

But where next for the rand?

But where next for the rand?There have been a number of external global factors causing developed market currency weakness and in turn, emerging market currency strength. Major economies around the world have continued, and in many cases extended, monetary easing programs, in an attempt to stimulate inflation and economic growth. While the US Federal Reserve has commenced a monetary tightening cycle, the process of raising interest rates has been paused for the time being, leaving lending rates at very accommodative levels as the global marketplace remains in a fragile economic state. In the EU and the UK, uncertainty pertaining to “Brexit” has further weighed on the respective currencies.

In South Africa, domestic factors for rand strength have been a moderate increase in interest rates and the short term aversion of a sub-investment ratings downgrade from ratings agencies Fitch and Standard and Poor’s. In the last few months improved trade balance data and a successful election process would have further helped the rand by bettering investor sentiment and aiding the attraction of foreign direct investment. While emerging market currencies in general were strong over this period, the rand’s outperformance of its peers (pre Finance Minister Saga) had paid tribute to the aforementioned catalysts. The relatively high interest rate environment in South Africa, when compared with that of developed markets, has also helped induce carry trade demand, with investors searching for an increased yield opportunity.

While accommodative monetary policy looks set to remain, and may be extended across major world economies, it might be argued that external risks to catalyse rand weakness may be diminished in the near-term. Against the dollar however, this might not be the case as the probability of a rate hike in the US is starting to appear more probable as Fed officials have been more hawkish in comments of late.

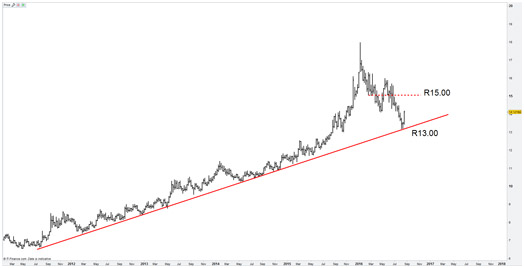

A look at a longer-term chart (Sept 2013 to present) of the rand against the dollar, shows a clear trend of weakening for the domestic currency. The strength we have seen in the shorter-term (Jan 2016 to current) almost feels like the normalisation of the currency after it had capitulated short term weakness in December last year.

However, the current investigations into the affairs of the South African Finance Minister are unlikely to find short-term resolve (as has been the nature of these types of event in the past). The end of the year also sees international ratings agencies’ review South Africa’s sovereign debt rating once again, and with economic growth now expected at 0% for the year, combined with political turmoil, a downgrade (or two) becomes a very real probability.

With these factors in mind, the risks to the South African rand might be skewed in favour of the long term weakening trend, finding the R15.00/USD mark a more likely short-term target than a retest of the R13/USD level for now.