Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the cash rate.Key points:- At its June meeting the RBA left the cash rate on hold at 4.35% as widely expected, leaving it unchanged for seven months now.

- The RBA reiterated that it is “not ruling anything in or out”, but its language including that in Governor Bullock’s press conference was a bit more hawkish than in May suggesting more risk of a hike than a cut in the near term.

- Reflecting the slightly more hawkish tone, shares fell and bond yields and the $A rose after the rate announcement, but the moves were marginal.

- We continue to see rates as having peaked, with rate cuts starting late this year. However, the risk of another hike is high if inflation surprises on the upside again this quarter.

The RBA holds rates at 4.35% - for the seventh month in a rowIn leaving rates on hold the RBA noted that high rates are continuing to work to rebalance demand and supply, inflation has fallen from its peak, there is uncertainty around the outlook for consumption and government energy rebates will temporarily reduce headline inflation. But it also noted that there is continuing excess demand, the labour market is easing but remains tight, government budgets may impact (presumably boost) demand, inflation has been easing more slowly than previously expected and services inflation remains persistent.

The RBA retained its comments that its “not ruling anything in or out” suggesting an ongoing neutral bias on rates. But its language remains relatively hawkish - particularly around inflation declining more slowly and continuing excess demand – with Governor Bullock confirming that the option of another hike was again discussed but a cut was not. And the return of a comment at the end of its post meeting statement that the RBA “will do what is necessary” to achieve a return of inflation to target underlines that this was a “hawkish hold” leaning its commentary a bit more hawkish than was the case in May. All of which suggests that the risks in the near term are still skewed towards another hike, particularly if June quarter inflation to be released at the end of July surprises on the upside again.

This makes the August RBA meeting, at which it will also review its economic forecasts, critical, and potentially live for a hike if June quarter inflation surprises on the upside.

The RBA continues to note that it “needs to be confident that inflation is moving sustainably towards the target range” and that it will be watching global developments, domestic demand, the labour market and the outlook for inflation.

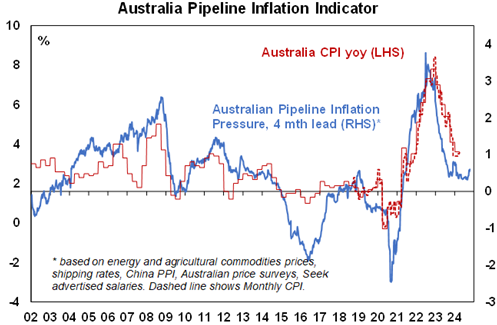

Our view remains that the next move in rates will be down with the first cut coming late this yearWhile the risk of another near-term rate hike is significant, inflation will be key and its worth nothing that our Pipeline Inflation Indicator continues to point down for Australian inflation from current levels and the Melbourne Institute’s May Inflation Gauge points to an ongoing fall in inflation. We have also been seeing a quarterly pattern of higher than expected then lower than expected inflation lately which suggests the June quarter could see lower than expected inflation. The resumption of lower inflation readings in the US after a period of hotter inflation readings earlier this year is also a positive sign for Australia in that Australian inflation has been lagging that in the US (both on the way up and now on the way down). Similarly, the lower increase in minimum and award wages this year granted by the Fair Work Commission supports the RBA’s assessment that wages growth has likely peaked.

So all up we continue to see the trend in inflation remaining down ultimately helping to avert another rate hike and allowing the RBA to start cutting rates in November or December (with a 0.25% cut to 4.1%).

Source: Bloomberg, AMP

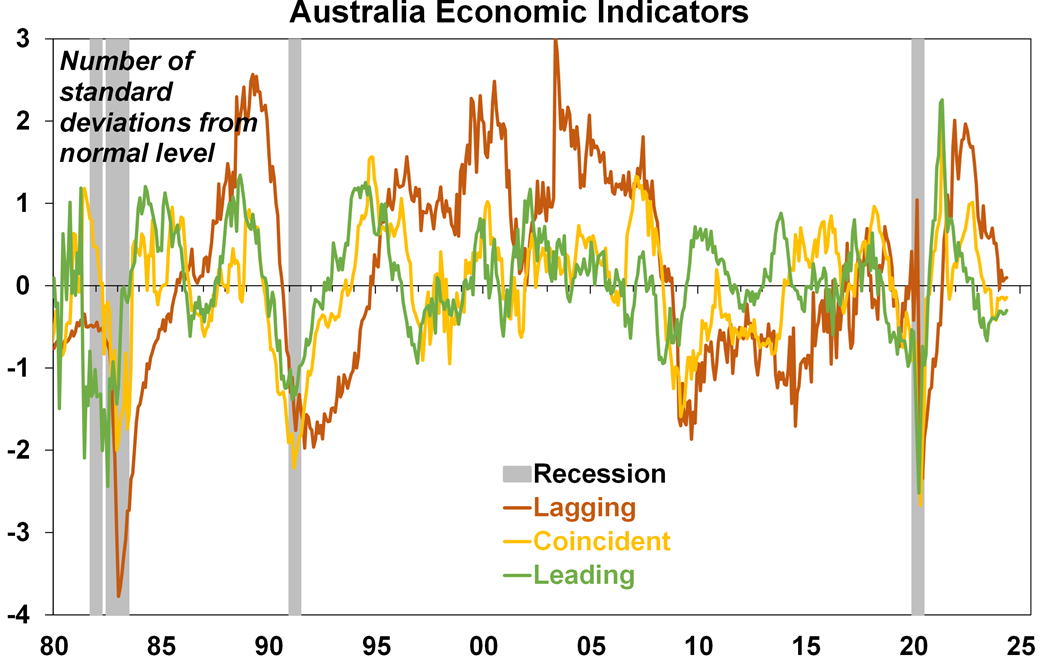

Similarly, Australian economic growth remains very weak with the economy virtually stalling in the March quarter. Retail sales and household spending data indicate that consumer spending remains very weak under the impact of high rates and cost of living pressures. More broadly the next chart shows a composite mix of economic indicators that lead (like building approvals, consumer and business confidence and the yield curve), are coincident with (like employment and retail sales) or lag (like unemployment and corporate delinquency rates) the economy. While none are at recessionary levels, they all remain very weak and certainly not suggesting of any overheating that may require further rate hikes.

Source: Bloomberg, AMP

Nevertheless, the path to rate cuts will likely remain bumpy and while our base case is for the first cut to come at year end, the risk of another rate hike in the near term is material as is the risk of a further delay in rate cuts into next year. The next key things to watch regarding the interest rate outlook will be the June quarter inflation data at the end of July, any early reading on the impact of the 1 July tax cuts on consumer spending and any revisions to its economic forecasts in August.

Ends Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.