By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

Investment markets and key developments

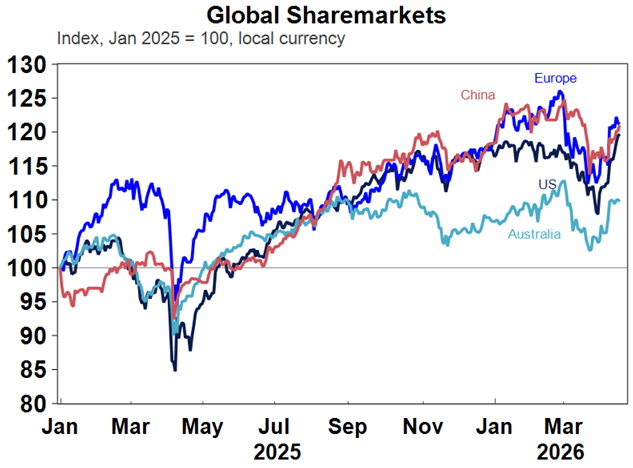

Global share markets rose further over the last week on optimism for a peace deal with Iran, with US and Japanese shares rising to record highs. Despite the positive global lead, Australian shares fell back slightly resulting in a fall of around 0.4% for the week reflecting concerns about a bigger boost to inflation in Australia and a bigger hit to economic growth as highlighted by sharp falls in consumer and business confidence and expectations that the RBA will raise rates again and remain more hawkish compared to other countries. While the ASX saw gains in IT and property shares this was offset by falls in financials and industrials.

Source: Macrobond, AMP

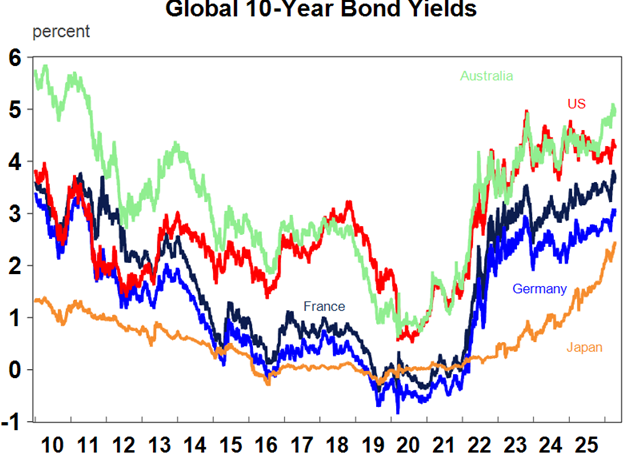

Global bond yields fell slightly but rose in Australia.

Source: Bloomberg, AMP

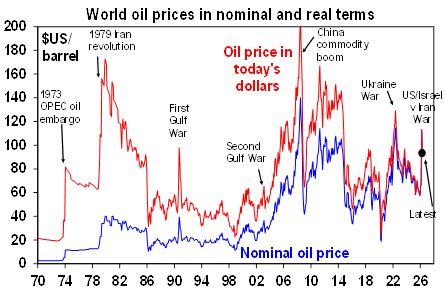

Oil prices fell a bit further but still remain around $US95 a barrel with the hit to oil supply continuing.

Source: Bloomberg, AMP

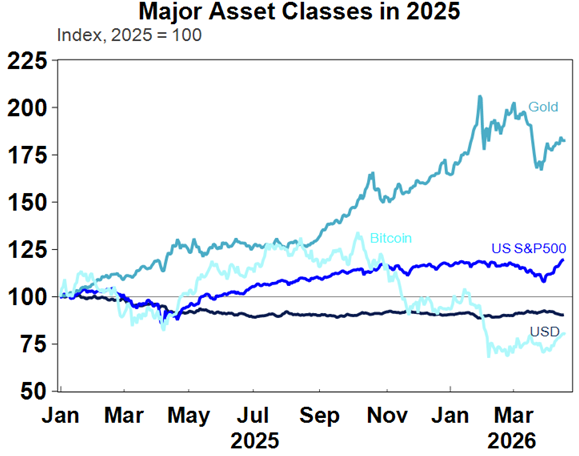

The continuing risk on tone saw the $US fall and the $A rise to its highest since 2022, with gold, metal and iron ore prices also up along with Bitcoin.

Source: Macrobond, AMP

On the road to peace with significant pressure on both the US and Iran to cut a deal – and share markets have been moving to factor this in. Despite the collapse of the initial US/Iran peace talks last weekend and the US blockading Iranian ships through the Strait which will further restrict global oil supplies, optimism regarding an end to the War was fuelled again in the last week by signs of renewed talks and an extension of the ceasefire with Trump saying prospects for a deal with Iran are “looking very good.” We continue to lean to the view that Trump will find a way to stay on the off ramp from the War. Pressure on Trump to back down remains very high with only a third of Americans supporting the War and his approval rating running below where it was 8 years ago and lower than Biden’s, because his policies including the War are worsening the affordability concerns that saw him elected in 2024. The Republicans are seeing increasing odds that they will lose both the House and the Senate in the midterms. And likewise, pressure on Iran to reach a deal is high as the US switch from bombing (which can unite a population) to even tougher economic sanctions via the blockade of Iranian oil exports will intensify popular discontent with the Iranian Government. And it may conclude that its ability to cause pain for the US by effectively blocking 20% of global oil supply means it has no need for nuclear weapons to ensure it survives. So its understandable that share markets have bounced back. This has ranged from a 70% recovery of the falls in Australia to a rebound to record highs in the US and Japan, with US shares moving to factor in another run of strong profit growth for the March quarter with earnings growth expectations running around 14%yoy.

Source: Bloomberg, AMP

However, there is a risk that shares may have run a bit ahead of themselves – particularly in the US where they are now at new record highs:

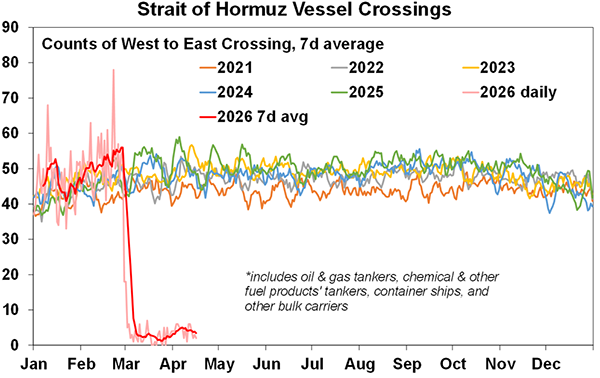

- There is still a high risk that the War could re-escalate again – with the US expanding its bombing and Iran retaliating by hitting more ships in the Strait of Hormuz and getting the Houthi’s to do the same in the Red Sea.

- The flow of ships through the Strait while up from its lows remains a fraction of normal levels so the hit to global oil supply continues.

Source: Bloomberg, AMP

- About of stagflation – higher inflation and weaker growth – is already baked in in the near term as even if there is a quick and sustained increase in ships flowing through the Strait it will take several months for global oil and related product flows to return to normal.

- The global economy is now getting closer to crunch time regarding the supply of oil – as the last ship load of oil to leave the Gulf before the War started is now getting refined into fuel and the longer the hit to oil supply continues the greater the risk of the global economy moving beyond a short term bout of stagflation into a recession along the lines flagged by the IMF.

- Australia is particularly vulnerable as it imports 80-90% of its fuel. Our rough estimate is that if the flow of oil through the Strait does not quickly resume we could survive till late next month but beyond that fuel rationing would likely be required which would mean a direct reduction in economic activity and the likelihood of recession. Disruption to production at the Geelong refinery due to a fire highlights the risk for Australia, although its looking like it won’t affect fuel supply and production could be back to normal in a few weeks.

- And even if a deal is reached to end the War and reopen the Strait the quality of that deal will be important. Because if the US just quits and leaves Iran more aggrieved and, in some ways, more powerful than ever, it could all flare up again – maybe after the US midterm elections are over.

So the risk of a renewed spike in oil prices and more volatility in shares remains high. Historically the pattern of weakness in midterm election years in the US, which on average has seen a 17% top to bottom fall in shares, starts around now and runs out to around October. Any renewed weakness in US shares would affect the Australian share market. As such, it remains a time for those with a short-term investment horizon to remain cautious.

A supply side shock – which both adds to prices and detracts from economic activity – presents tough choices for central banks but the experience of the 1970s oil shocks which contributed to higher inflation and inflation expectations suggests central banks will likely initially focus on the hit to inflation – biasing interest rates to the upside rather than the downside. Consistent with this market expectations for major central banks policy rates have increased since the War started, with only a 33% chance of a rate cut priced in for the US down from more than two rate cuts expected prior to the War and Europe, the UK and Canada now all expected to raise rates this year.

In Australia, we expect the RBA to hike again but it’s a very close call. The challenge facing the RBA was highlighted by Deputy Governor Hauser who noted that the risks to inflation “might still be on the upside, in which case we’re going to have to respond. But we do also need to take account the of the possibility that activity slows.” But his urging of governments to support central banks in undertaking unpopular rate hikes to lower inflation could also be interpreted as preparation for another rate hike. Inflation expectations, wage pressures and cost and price pressures as flagged in business surveys have all moved up since the War started and March data highlights that the labour market was tight going into the War all of which biases the RBA towards more rate hikes. But against this, the labour market is a lagging indicator and slumps in business and consumer confidence point to weaker economic conditions ahead which will dampen inflation eventually. In the near term we think the RBA will give primacy to the increased threat to inflation and so see another rate hike in May. But it can’t ignore the potential hit to economic growth, so the May RBA meeting is a close call, and we put the probability of a hike versus a hold at 60/40. Market pricing for a 74% probability of a hike in May looks too aggressive though and if the RBA does continue hiking, we see it cutting next year.

Major global economic events and implications

US economic data was again a mixed bag. Industrial production fell in March, but manufacturing conditions in the New York and Philadelphia regions improved sharply in April. Jobless claims also fell and remain low. Against this small business optimism fell and housing indicators remained depressed with falls in existing home sales and home builder conditions not helped by a rise in mortgage rates. Meanwhile, the Fed’s latest Beige Book of anecdotal evidence for April suggests a limited impact of the War so far on economic activity, but stronger cost pressures and uncertainty weighing on investment and hiring.

Source: Macrobond, AMP

While US producer price inflation in March rose less than expected, key components from it along with the CPI point to a rise in core private final consumption inflation to 3.2%yoy in March from 3%yoy in February. And the regional manufacturing surveys show a sharp rise in cost pressures.

Source: Macrobond, AMP

Uncertainty around the Fed continues, with Trump again threatening to sack Powell, but markets see little impact. The Senate Banking Committee hearing to consider Trump’s nominee Kevin Warsh as the new Fed Chair is set for 21 April, but GOP committee member Tillis is still refusing to vote on him until the DoJ action against Powell is resolved which it looks like it won’t be any time soon, so Warsh looks unlikely to be approved by the 15 May expiration of Powell’s term which probably means Powell stays on as Chair for a while. However, Trump is saying he will sack him if he doesn’t step down on 15 May. Markets are no longer responding much to this as: Trump unlikely has the power to follow through on his threats; even if the courts agree that Trump has the power to replace Powell as interim Chair he would most likely be replaced by the Vice-Chair who has similar views; and once Warsh takes over (assuming he does), the Fed under his leadership is unlikely to take a different approach to rates in the near term than under Powell. At a broader level were it not for Trump’s tariffs and now the War which also threatens higher inflation for longer the Fed probably would have cut rates more by now. So, the main brake on rate cuts has been Trump himself!

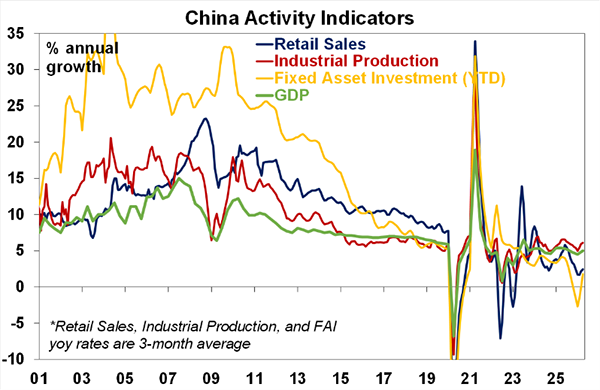

China’s economy doing better at the start of the year. March quarter GDP rose 1.3%qoq which took annual growth to 5%yoy. Growth in industrial production and investment in March were stronger than expected but retail sales were weaker. Cutting through monthly volatility all have seen some improvement since late last year. And home price falls have slowed. Policy measures are likely still needed to boost consumer spending and the housing sector, but they are likely to remain incremental unless the oil supply shock goes on for longer than expected.

Source: Bloomberg, AMP

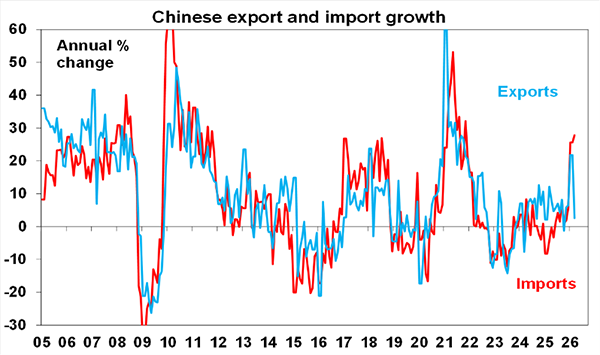

Chinese export growth plunged in March after booming 20%yoy in January and February but the volatility likely reflects distortions due to the timing of the Lunar New Year. Exports to the US remain depressed with exports to other countries filling the gap. Import growth accelerated even further but appears to reflect more trading days this March.

Source: Bloomberg, AMP

Australia economic events and implications

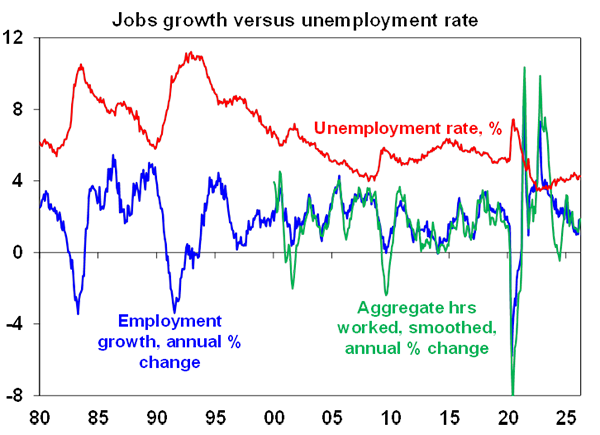

After a messy February, jobs data for March was solid, with solid growth in employment and hours worked and unemployment and underemployment unchanged. While unemployment is in a mild rising trend it remains low versus recent decades as does underemployment.

Source: Bloomberg, AMP

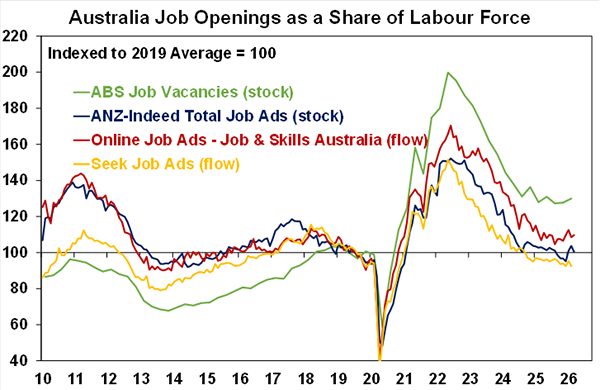

Job vacancies are down from their highs but are at okay levels and may have been starting to bottom. So the RBA is likely to continue to characterise the jobs market as slightly tight. However, the jobs data even up to March is now pretty dated given the likely hit to growth flowing from higher fuel prices and the oil supply shock. Going forward we expect this to result in higher unemployment.

Source: ABS, AMP

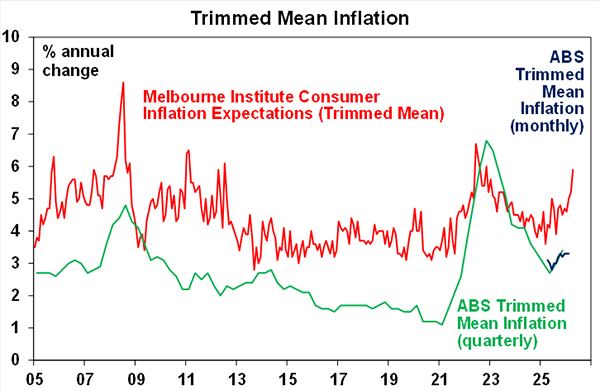

The rise in petrol prices and all the talk of higher inflation has seen consumer inflation expectations spike to 5.9%, its highest since 2022. So far wage growth expectations have not picked up but the ACTU is calling for a 5% rise in minimum and award wages and is likely to now revise it higher so the risks to wages growth are skewed to the upside. This will worry the RBA as it raises the risk higher cost and price pressures will become more entrenched.

Source: ABS, Melbourne Institute, AMP

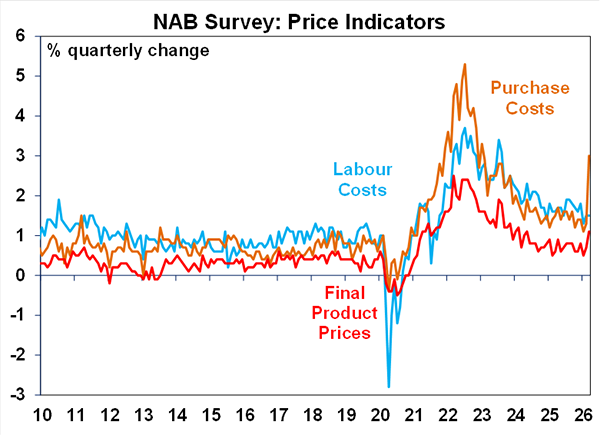

The impact of the surge in energy and other costs associated with the War is also evident with the NAB survey showing a surge in purchase costs and final product prices. This will add to RBA concerns, particularly as the price and cost indicators in the NAB survey had been heading in the right direction.

Source: NAB, AMP

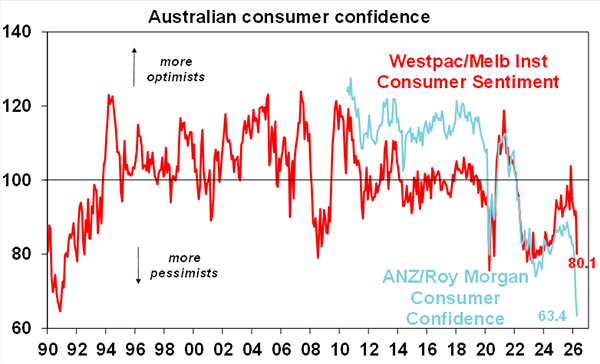

However, the Iran War has also hit consumer and business confidence very hard. The Westpac/Melbourne Institute’s consumer confidence index plunged 12% in April taking it back to around pandemic and 2022 rate hike lows with the decline being broad based across components and across mortgage holders, outright homeowners and tenants. Consumers are also now expecting a sharp rise in unemployment. The alternative ANZ/Roy Morgan index is even weaker at record lows.

Source: Westpac/Melbourne Institute, ANZ/Roy Morgan, AMP

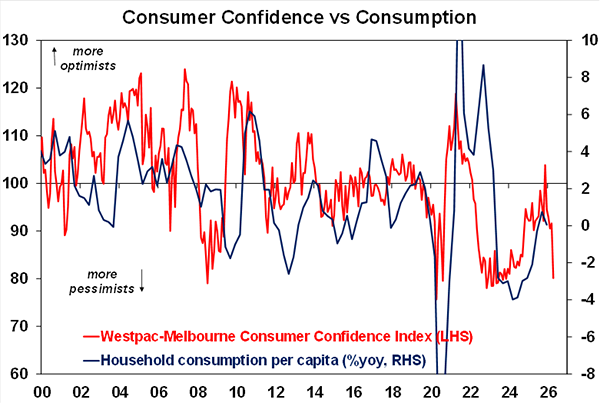

While the link is not always reliable, the plunge in consumer confidence if sustained is warning of weakness in consumer spending ahead.

Source: Westpac/Melbourne Institute, AMP

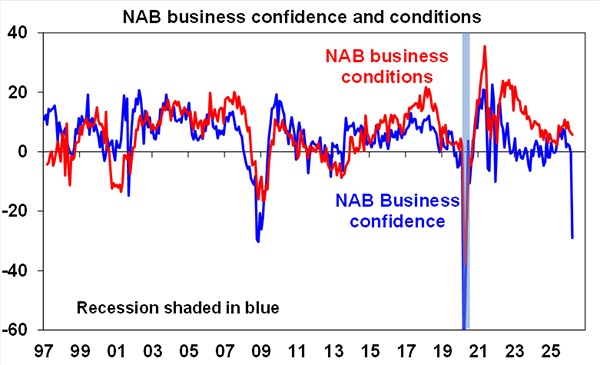

While the latest NAB business survey showed okay business conditions, business confidence also plunged with worries regarding the impact of the War.

Source: NAB, AMP

So, it’s a hard balancing act for the RBA!

What to watch over the next week?

Business conditions PMIs for April to be released Thursday for developed countries including Australia are likely to show further signs of stagflation with another slump in conditions and confidence and a further rise in cost and price pressures reflecting the impact of the supply shock flowing from the War.

In the US, expect a solid 1.2% rise in March retail sales (Tuesday) due to higher gasoline prices, but underlying retail sales growth to be soft. The US March quarter profit reporting season will continue. Consensus expectations are for 14%yoy earnings growth, but this is likely to end up around 18%yoy, which will be the strongest in four years.

Canadian inflation for March (Monday) is likely to spike 1.1%mom to 2.6%yoy, but with the core inflation measures remaining around 2.3%yoy.

UK inflation for March (Wednesday) is likely to spike for the same reasons to around 3.8%yoy from 3%yoy, but again with core inflation remaining around 3.2% for now.

It will likely be similar in New Zealand (Tuesday) with March quarter CPI inflation likely to rise 0.9%qoq, but falling to 2.9%yoy.

Japanese inflation for March (Friday) is likely to rise to around 1.5%yoy, with core inflation around the same level.

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the War and oil shock if the flow of oil quickly resumes but the risk of further falls taking us to a 15% top to bottom correction remain given uncertainty around the peace talks and flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and increasing worries about private credit and the impact of AI. However, returns should still be positive for the year as a whole thanks to Fed rate cuts likely later in the year, Trump still likely to pivot to consumer-friendly policies ahead of the midterms and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to around 3-5% due to poor affordability, RBA rate hikes and the hit to confidence from higher fuel prices and the War.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA hikes. Fair value for the $A is around $US0.72.