This article was originally published on 14 December 2023.Mid-Year Economic and Fiscal Outlook - budget deficits revised down, immigration revised up but projected to have peaked

Key points:- The Federal Government’s Mid-Year Economic and Fiscal Outlook (MYEFO) revised its budget deficit projections down sharply largely reflecting stronger revenue and some modest spending savings.

- The deficit for this year is now revised down to just $1.1bn (from $13.9bn in the May Budget), with a surplus possible.

- Structural pressures on spending remain for the years ahead and are expected to steadily push spending up as a share of GDP.

- There are no major new spending announcements in the MYEFO.

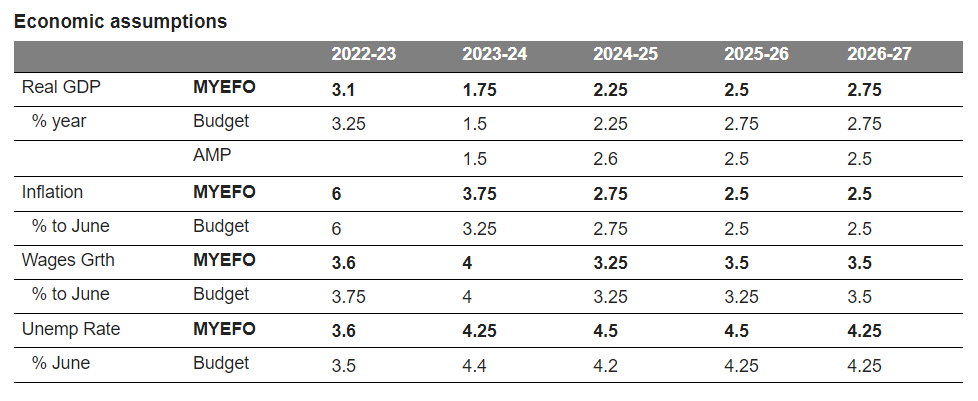

- The Government is now forecasting slightly higher growth and inflation this financial year, but its inflation forecasts are slightly lower than the RBAs.

Economic growth and inflation revised up, but inflation forecast to fall slightly faster than the RBA is forecastingReflecting the more resilient than expected economy so far the Government for this financial year has revised up its growth forecasts slightly and revised down its unemployment forecasts. But its revised up the unemployment forecast for next year to a peak of 4.5%. The Government’s forecasts are similar to those in the RBA’s latest Statement of Monetary Policy although it sees unemployment peaking at 4.5% in contrasts to the RBA’s forecast peak of 4.25%.

While the Government has revised up its inflation forecast for this year, its inflation forecasts are about 0.25% below those of the RBA and it sees inflation falling below the 2-3% target by mid next year which is six months earlier than the RBA is forecasting. If the Government is right it may justify a slightly lower profile for the cash rate and an earlier start to rate cuts than the RBA’s forecasts would imply, but there is not much in it.

Source: Australian Treasury, AMP

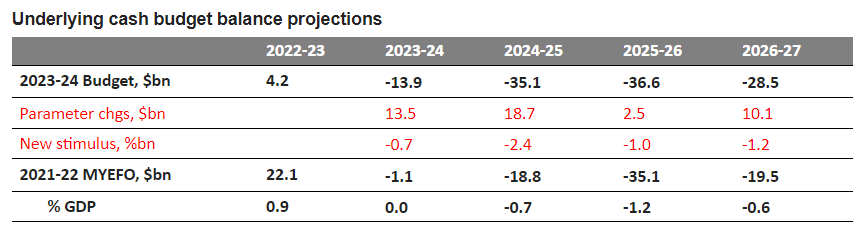

Budget deficits revised down with a surplus likely this financial yearThe Government is now projecting sharply lower budget deficits, with the deficit forecast to fall to $1.1bn this financial year from the Budget forecast of $13.9bn. With the budget for the first four months of the year running $9bn ahead of May Budget estimates it could easily turn into a surplus for this year.

The key drivers of the improvement are $64bn in estimated higher receipts over the four years to 2026-27 due to higher company tax payments (on the back of higher commodity prices) and higher personal tax (due to stronger employment and bracket creep) along with a $7.4bn delay in infrastructure payments.

As can be seen in the next table the bulk of the saving (called parameter changes) are being used to reduce the budget deficit with only $1-2bn a year in new spending.

While the Government should ideally be further cutting spending to take pressure off inflation at least it’s allowing the bulk of the revenue windfall to go to the budget bottom line and so is sucking money out of the economy compared to what otherwise would have been the case and this also helps slow inflation.

That said the currently projected Federal and State budget balance projections imply around a 1.5% of GDP in fiscal stimulus this financial year after a 3.1% of GDP contraction last financial year. Of course, a continued improvement in the budget into surplus will reduce this.

Source: Australian Treasury, AMP

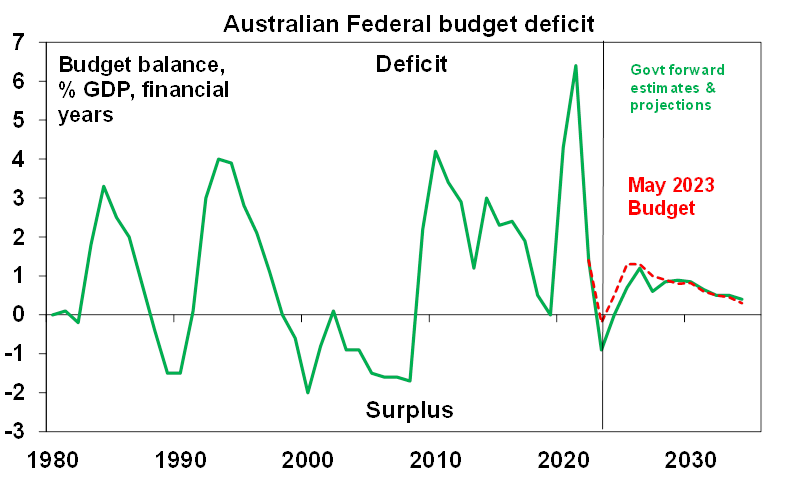

The budget is in far better shape than projected just two years ago. As a result of the improvement in the MYEFO net debt is projected to be $624bn in June 2027, down from $703bn projected in the May Budget. But note that the MYEFO projections show basically no improvement beyond the four year forward estimates and show ongoing deficits for the next decade

Source: RBA, Australian Treasury, AMP

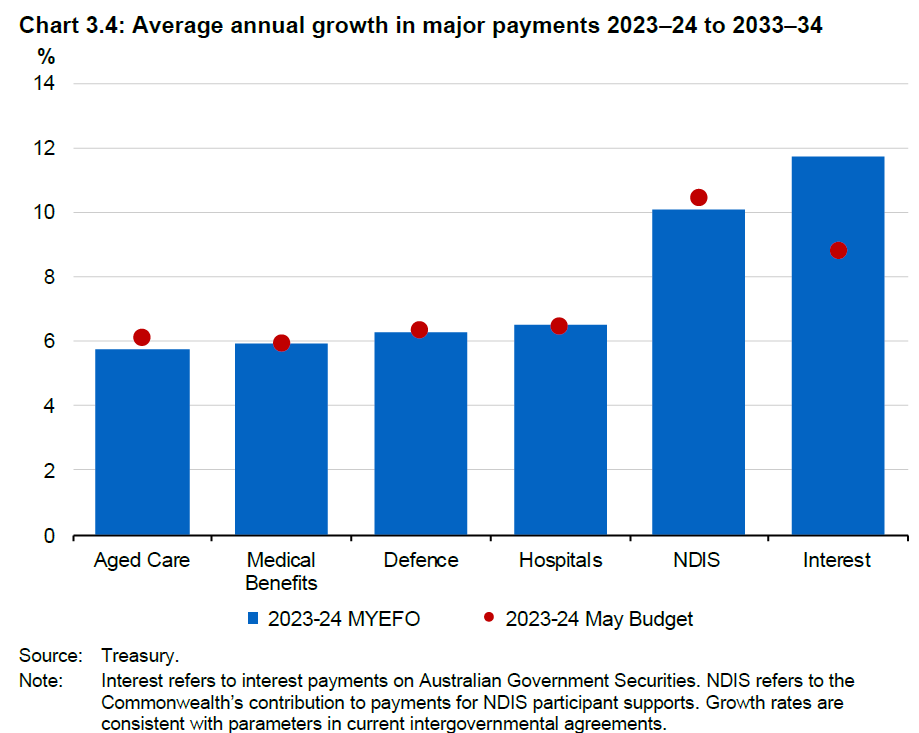

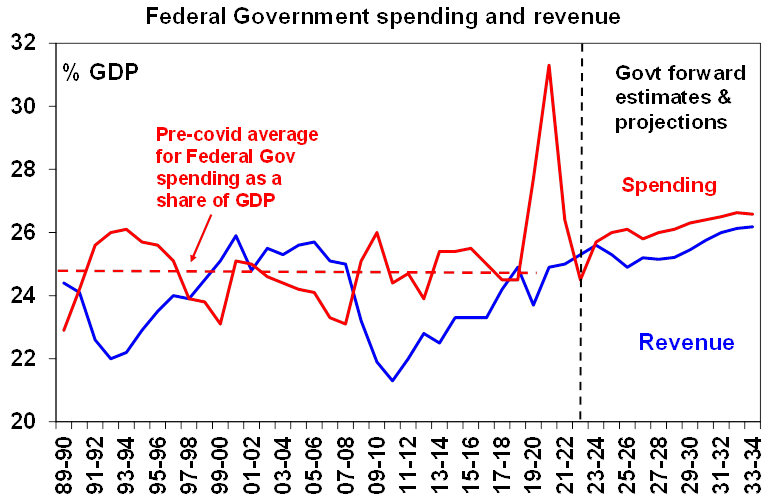

This largely reflects structural spending pressures – particularly for interest costs - which are now expected to show the fastest growth over the next decade, the NDIS, health, defence and aged care.

As a result, the level of Government spending is projected to rise steadily as a share of GDP over the decade ahead, taking it well above the 24.8% of GDP that prevailed pre-covid. Ever bigger government won’t help improve Australia’s deteriorating productivity performance and hence living standards.

Source: Australian Treasury, AMP Capital

Net overseas migration to be reduced – but it will still be very high this yearThe Government’s move to overhaul the visa system to better control long term (mainly student and work) arrivals and hence total net overseas migration is good news after net migration in 2022-23 blew out to an estimated record 510,000 from a projection of 180,000 in the March 2022 Budget. The Government estimates that as a result there will be 185,000 fewer net arrivals over the next 4 years, but net migration is still projected to be 375,000 this financial year (which is up from the May Budget forecast of 315,000) and fall to 250,000 in 2024-25 (similar to the Budget’s forecast of 260,000).

Moving to get immigration under control is good news but it’s still above pre-covid average levels (which were around 230,000 a year) and will still be adding to the housing shortfall which we estimate to have been around 120,000 dwellings in June rising to around 180,000 by June next year. This is because underlying demand will continue to run above housing completions of around 170,000 dwellings a year. As a result, the supply shortfall will remain a source of underlying upwards pressure on rents and home prices, although an affordability constraint and high interest rates will likely dominate and push prices lower in the year ahead.

Ends Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.