Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, economic activity trackers, major global economic events and Australian economic events.Investment markets and key developments over the past weekShare markets were mixed over the last week with US shares up 0.2% for the week helped by still solid but cooling jobs data and Eurozone shares rose 2% on dovish ECB comments, but Japanese shares fell 3.4% on speculation of a BoJ rate hike soon (which also pushed the Yen up) and Chinese shares fell 1.7%. Australian shares rose by 1.7% helped by speculation that the RBA has finished tightening. Bond yields rose slightly in the US and Japan but fell in Europe and Australia. Oil prices fell 3.8%, briefly falling below $US0.70 on oversupply concerns. Metal prices also fell but iron ore prices rose. The $A fell below $US0.66 as the $US rose.

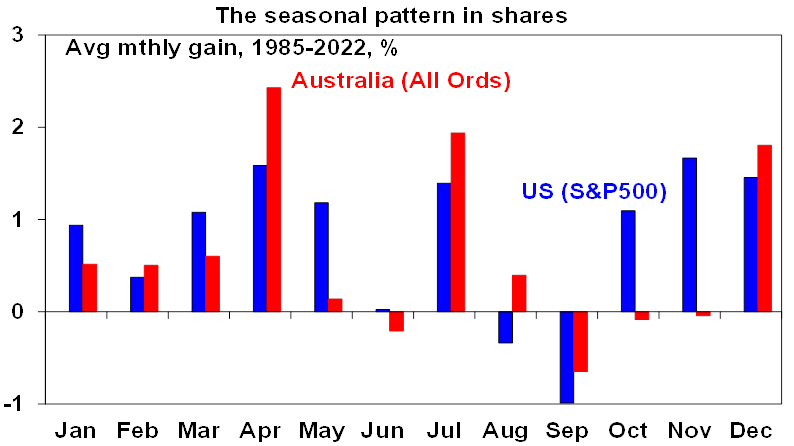

Despite the rebound in share markets since the October lows there remain significant risks to keep an eye including: sticky services inflation which could mean the risk of “high for longer” rates and another RBA rate hike; the still high risk of recession; uncertainty about the Chinese economy and property sector; and geopolitical threats around US politics, Israel and Taiwan. However, while shares remain vulnerable to a very short term consolidation or pull back after strong gains since October they are likely to see more upside in the months ahead as inflation continues to ease, the monetary policy environment turns progressively less threatening, economic indicators remain consistent with a soft landing, geopolitical threats likely take a back seat for a while and positive share market seasonality remains in place with the Santa Rally normally kicking in later this month. So while we should expect lots of bumps along the way our base case remains that global and Australian shares can trend up.

Source: Bloomberg, AMP

The past week saw more evidence of easing inflation and major central banks being at the top on rates. Inflation in Thailand, Taiwan, the Philippines and South Korea all fell further in November, the Bank of Canada left rates on hold and more ECB officials are turning less hawkish or even dovish.

The Bank of Japan is an exception of course having not even started to raise rates but may do so in the next few months with comments by BoJ Governor Ueda (that his job will get more challenging from year end) and one of his deputies (playing down the adverse impact of a rate hike) interpreted as paving the way for a hike. Any BoJ hikes are likely to be gradual through leaving Japanese interest rates well below those in other countries for some time to come meaning that any impact globally should turn out to be modest (after any initial shock) – it will imply some upward pressure on US and Australian bond yields but this should be more than offset next year by falling inflation.

RBA on hold and most likely at the top ahead of rate cuts from the September quarter. As widely expected the RBA at its December meeting left rates at 4.35% noting that data since the last meeting was consistent with its expectations. While it retained the softened tightening bias used after the November meeting that “whether further tightening of monetary policy will be required…will depend upon the data and the evolving assessment of risks” the Governor’s commentary post the November meeting remained pretty hawkish and the same could happen again given the RBA’s ongoing concerns about inflation taking too long to get back to target. As such the risk of another rate hike remains high at around 40% - and if it occurs it will probably be at the February meeting. Key to watch ahead of this meeting will be December quarter inflation data and the next two rounds of retail sales and jobs data. However, we remain of the view that the RBA has already done enough as the September quarter GDP data shows a sharply slowing economy and struggling consumer, October data suggests that consumer spending growth may be turning negative this quarter and monthly CPI inflation is likely to have a three in front of it by December. So our central view is that economic data between now and the February meeting won’t provide the justification for another rate hike and that the cash rate is at the top and we are continuing to allow for rate cuts starting from the September quarter next year. The money market is attaching no probability to any further rate hike with nearly a full rate cut priced in by September.

The new Statement on the Conduct of Monetary Policy agreed by the Treasurer and Governor of the RBA contains no surprises and is unlikely to lead to a different path for interest rates but does contain some big risks. Basically, the Statement affirms that both price stability and full employment as the RBA’s objectives with an overarching objective being the “economic prosperity and welfare of the Australian people”. The flexible 2-3% inflation target will remain in place but with the RBA setting policy to return inflation to the mid-point of the target but with the timeframe dependent on balancing this with its full employment objective. And the full employment objective is defined in terms of “maximum employment consistent with low and stable inflation” (which is basically NAIRU) which really means no change for the RBA and leaves the Government focussed on effectively trying to lower the NAIRU as it should. The removal of “on average over time” regarding the inflation target and the new focus on 2.5% is a bit hawkish given the RBA does not currently see inflation falling to 2.9% until the end of 2025 but given this is balanced by the full employment objective its marginal and unlikely to make any significant difference to the level of rates set by the RBA. Maybe its just semantics, but I struggle with the logic behind making this change as the previous approach was worked well.

The rest of the Statement formally responds to the recommendations from the RBA Review and seeks to boost communications and transparency around policy setting and tools, commits to regular five year reviews and commits to the setting up of a Governance and Monetary Policy Board (MPB) with both to be chaired by the Governor and the latter to comprise six outsiders (chosen by the Treasurer) along with the Governor, Deputy Governor and Treasury Secretary. The Monetary Policy Board will publish an unattributed record of votes. Our concerns remain that the: dominance of the MPB by outsider macro policy experts means that they can outvote the RBA on monetary policy decisions which would see the RBA at times having to explain decisions that it does not support which will risk reducing its authority, accountability and potentially morale; the perceived increased power of the new MPB runs the risk that the Government will seek to stack it with members with a particular bias; having each MPB member conduct at least one speech a year will likely add to confusion as we often see with multiple Fed speakers; & the extra communications from the RBA including press conferences risks further adding to the drama and confusion around what the RBA will do and to the obsession with it which is not seen in other countries.

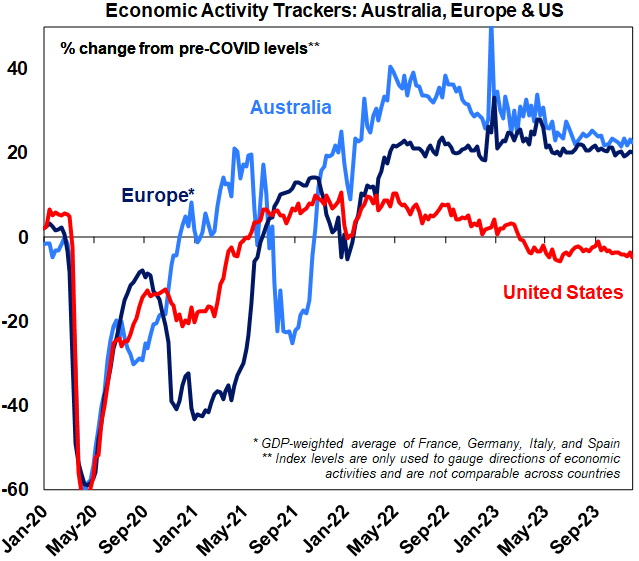

Economic activity trackersOur Economic Activity Trackers are still not showing anything decisive for the direction of economic activity.

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence and credit & debit card transactions. Source: AMP

Major global economic events and implicationsUS economic data was mixed consistent with a slowing in growth this quarter and a continuing easing in the labour market. The services conditions ISM rose slightly in November and remains ok and consumer confidence rose. November payrolls came in stronger than expected at 199,000 but - with the gains narrowly concentrated in health, education and government, roughly 38,000 workers returning from strikes, temporary employment falling, and prior months revised down by 35,000 - the underlying trend remains consistent with a slowing jobs market. Unemployment fell back to 3.7% due to volatile household survey employment but the trend is up, and wages growth was flat at 4%yoy and well down from highs. What’s more job openings fell sharply. All of this suggests that while the US labour market remains tight its easing. Falling job openings will reduce wages pressure even if unemployment remains low. All of which is another pointer to easing inflation pressures. Consistent with this and partly reflecting falling gasoline prices, consumer 1 year ahead inflation expectations fell to 3.1%pa (from 4.5%) and 5-10 year ahead inflation expectations fell to 2.8% (from 3.2%).

Source: Bloomberg, AMP

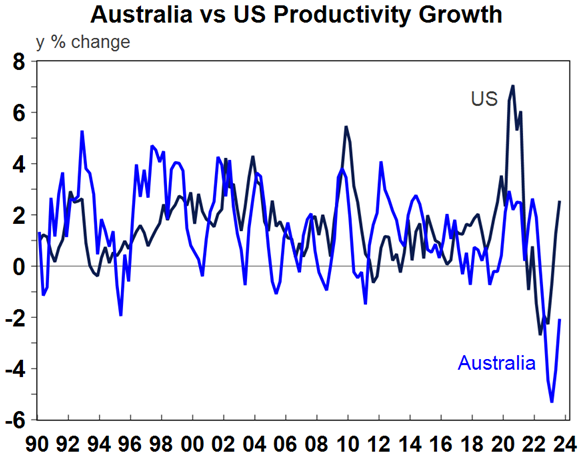

Rebounding US productivity. US productivity growth was also revised up to a strong 5.2% annualised rate in the September quarter which takes pressure off inflation by lowering unit labour costs. Hopefully the rebound in US productivity - which like Australia also saw a reopening slump, albeit not as deep – is leading a rebound in Australian productivity.

Source: Macrobond, ABS, AMP

Bank of Canada on hold. No surprises from the BoC which left rates at 5%. It retains a tightening bias but it dropped a reference from its last meeting to rising inflationary risks. Expect the BoC to remain on hold for the next few months, with June quarter rate cuts.

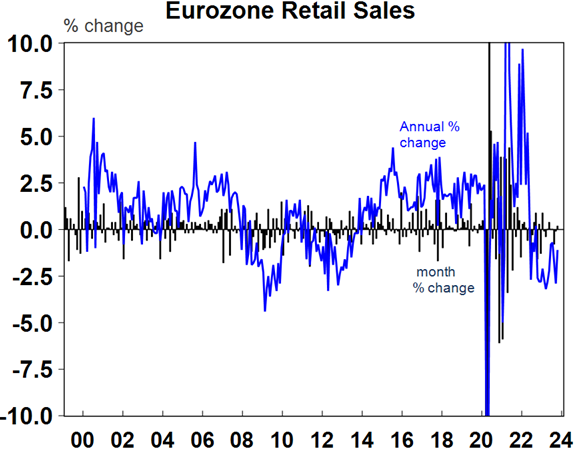

Eurozone retail sales remained weak in October, German factory orders fell another 3.7% and ECB officials are starting to sound less hawkish, with notable hawk Schnabel acknowledging the remarkable progress in reducing inflation and not ruling out a rate cut in the next six months.

Source: Macrobond, AMP

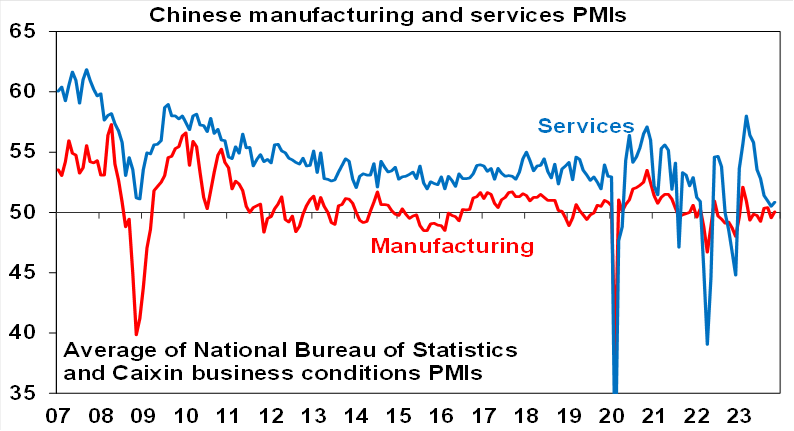

Chinese business conditions PMIs for November are maybe not as soft as first reported but are still soft. In contrast to the official PMIs which fell in November, the Caixin private sector survey which fosses more on smaller private businesses improved slightly, pulling up the average of the two. Its still softish though but at least its not falling.

Source: Bloomberg, AMP

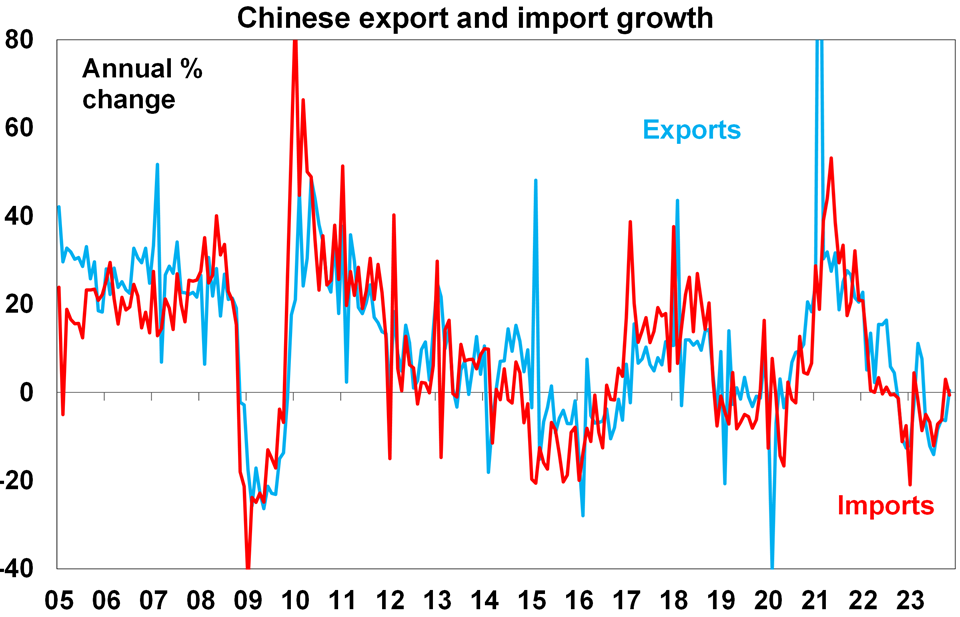

Meanwhile, Chinese exports and imports for November were roughly flat on a year ago – not great, but better a few months ago.

Source: Bloomberg, AMP

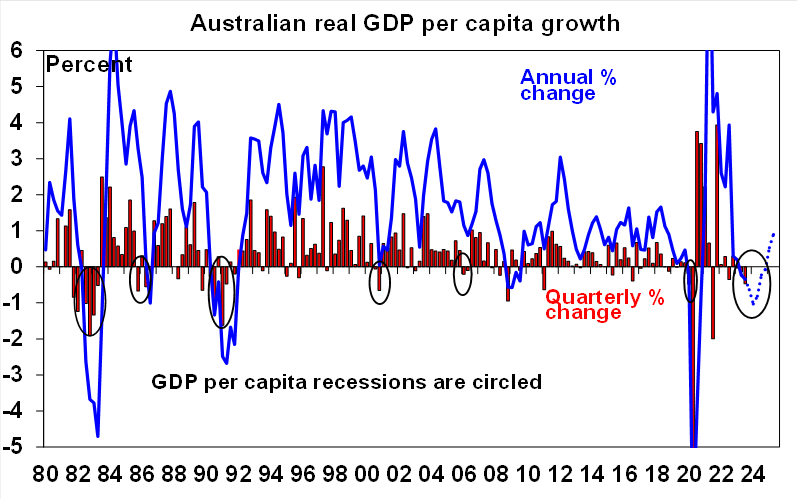

Australian economic events and implicationsMonetary policy works - rate hikes are clearly hitting growth. September quarter GDP and other data released over the last week leave no doubt that the household sector is getting hit hard by rate hikes. While annual GDP growth was stronger than expected at 2.1%yoy, this reflected upwards revisions to past quarters with September quarter GDP growth coming in well below expectations at 0.2%qoq. In fact, were it not for strong growth in public spending (including power and childcare subsidies to households) and a contribution from inventories the economy would have gone backwards. Strong population growth is masking the fact that the economy is in a “per capita recession” which is likely to continue.

Source: ABS, AMP

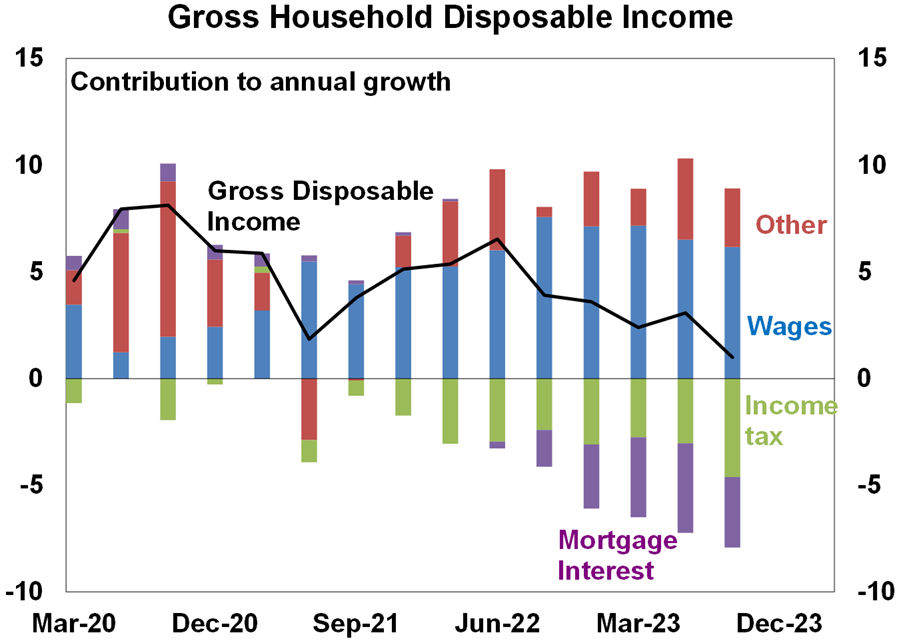

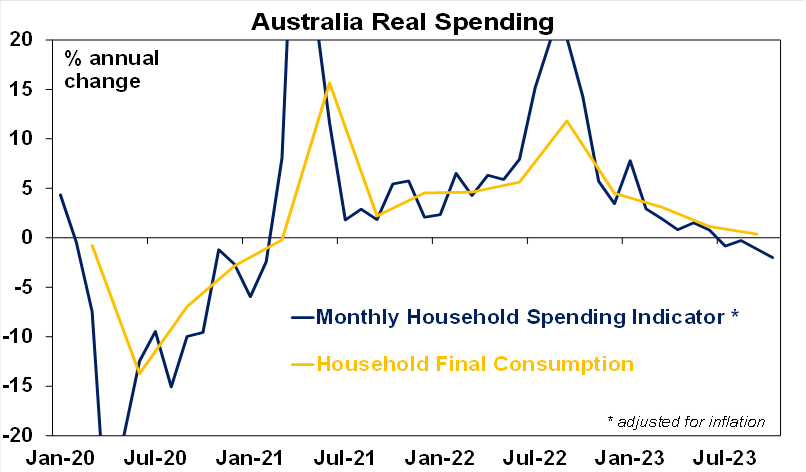

Weakness is concentrated in the household sector with the national accounts showing consumer spending stalling in the September quarter and down 2% per person over the last year highlighting that the average Australian is cutting back discretionary spending (its just that there are more of us!). While labour income has been strong this is being swamped by increasing mortgage payments and higher tax payments. This saw nominal income growth fall to 1% and once inflation is allowed for real growth in household disposable income is down nearly 5%yoy. Of course, many households are surviving by cutting saving but the household saving rate has already collapsed so there is a limit to this.

Source: ABS, AMP

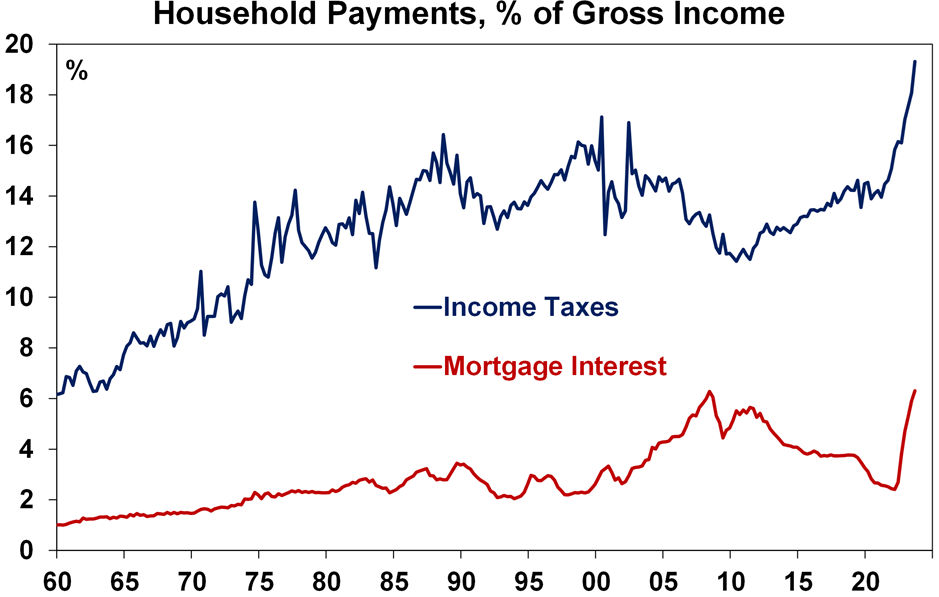

The share of gross household income devoted to mortgage payments and tax payments are now both at or around record highs. Yes the surge in tax payments was impacted by the end of LMITO and more people in employment is playing a role but a big part of it reflects “bracket creep” flowing from rising wages. This is occurring right across the tax scales as workers tip into tax brackets that were never intended for them resulting in stealth tax hikes. This has taken the income tax share back above where it was just before the GST was introduced which was designed to reduce reliance on personal tax. Unfortunately its now looking like we are back where we started highlighting the need for another round of tax reform. With tax taking up an additional 5% of gross household income compared to two years ago and mortgage interest rates taking up and additional 4% its pretty obvious that the household sector as a whole is under pressure to cut back spending.

Source: ABS, AMP

With the lagged impact of rate hikes still feeding through further weakness in consumption is likely. In fact, the ABS Household Spending Indicator for October suggests that real consumer spending will go negative this quarter. The risk of this driving a traditional GDP recession remains high.

Source: ABS, AMP

In other data ANZ job ads fell again in November and are down 17% on a year ago pointing to a softer jobs market. Housing finance rose a solid 5.4% in October, but it’s still down 21% from their record 2022 high (despite home prices being at a record) and may since have been dampened by the November rate hike and slowing home price gains and auction clearance rates.

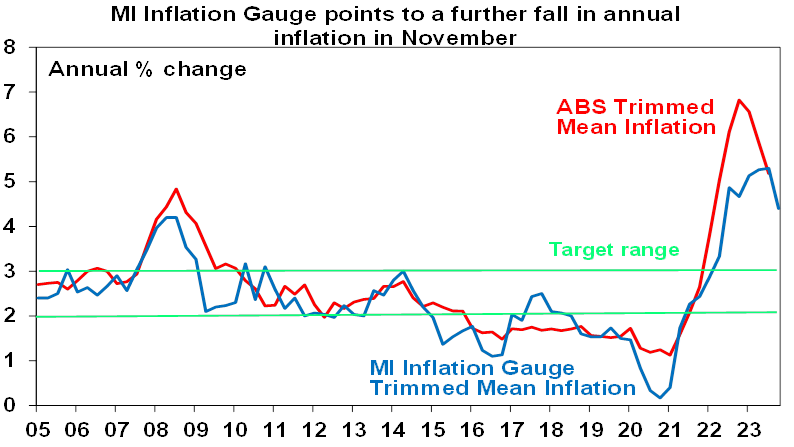

There was some more good news on inflation with productivity up in the September quarter after several quarters of falls (which is good because it lowers unit labour costs) and the Melbourne Institute’s Inflation Gauge for November continues to slow.

Source: Melbourne Institute, AMP

What to watch over the next week?The week ahead will be a big one for central banks with final meetings for the year in the US, Eurozone, Switzerland, Norway, the UK, Mexico, Taiwan and the Philippines but all are expected to leave rates on hold reflecting lower inflation.

In the US, the Fed (Wednesday) is expected to leave the Fed Funds rate at 5.25-5.5% helped by softer than expected inflation and ongoing signs of a cooling labour market. Chair Powell is likely to acknowledge the improvement in inflation and reiterate that the Fed is proceeding carefully but he is also likely to indicate a preparedness to raise rates again if needed and may push back against market expectations for 4 to 5 interest rate cuts next year starting from around March. The dot plot of Fed officials’ interest rate expectations is likely to only show two cuts for next year. On the data front in the US expect: small business optimism to remain weak (Monday); CPI inflation for November (Tuesday) to fall to 3.1%yoy (from 3.2%) but core CPI inflation unchanged at 4%yoy; November retail sales (Thursday) to remain weak and fall 0.1%mom; industrial production (Friday) to rise 0.2%mom; and slight falls in the December New York regional manufacturing conditions index and business conditions PMIs (also Friday).

The ECB (Thursday) is expected to leave its main refinancing rate unchanged at 4.5% reflecting the faster than expected fall in inflation and weak economic data with President Lagarde likely to relax her guidance implying no rate cuts before second half 2024. Business conditions PMIs (Friday) are likely to remain weak.

The Bank of England (also Thursday) is expected to leave its key policy rate on hold at 5.25%.

The Bank of Japan’s December quarter Tankan business survey (Wednesday) is likely to remain reasonably solid. Japanese business conditions PMIs (Friday) will also be released.

Chinese economic activity data for November (Friday) is likely to show an acceleration in annual growth for industrial production and retail sales, but this will mainly reflect low year ago base levels due to Covid restrictions at the time.

In Australia, the Westpac/MI measure of consumer confidence might see a slight boost for December following news of the RBA holding rates steady but its likely to remain depressed. The NAB business survey for November will be watched for any slowing in business conditions as already seen in PMIs. Jobs data for November (Thursday) is likely to show a 7,000 fall in employment after the boost from referendum workers in October with unemployment rising to 3.8%. And business conditions PMIs for December (Friday) are likely to have remained soft. June quarter population data (Thursday) will likely confirm the surge in immigration this year. A speech by RBA Governor Bullock (Tuesday) will be watched for any new clues on the interest rate outlook and it will be interesting to see if the pattern of a less hawkish post meeting Statement followed by relatively hawkish commentary continues.

The Federal Government’s Mid-Year Economic and Fiscal Outlook (MYEFO) to be released on Wednesday is likely to show a downwards revision to the $13.9bn projected deficit for this financial year (reports suggest the Government is not yet likely to show a surplus although monthly results point to one). Compared to the May Budget economic forecasts are likely to show unchanged growth but lower unemployment for this financial year and slightly higher inflation forecasts for this financial year and next.

Outlook for investment marketsThe next 12 months are likely to see a further easing in inflation pressure and central banks moving to get off the brakes. This should make for reasonable share market returns, provided any recession is mild as we expect. But sticky services inflation, still high recession risk, China worries and geopolitical risks are likely to ensure a few significant bumps along the way.

Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become dovish.

Unlisted commercial property and infrastructure are expected to see soft returns, reflecting the lagged impact of the rise in bond yields on valuations. Commercial property returns are likely to remain negative as “work from home” continues to hit space demand as leases expire.

With the lagged impact of high interest rates appearing to get the upper hand again we now expect national average home prices to fall around 5% in 2024. The supply shortfall should prevent a sharper fall and we expect a wide dispersion with prices still rising in Adelaide, Brisbane and Perth but sharper falls in Sydney and Melbourne. A deep recession and sharply higher unemployment would risk pushing prices below their January 2023 low.

Cash and bank deposits are expected to provide returns of around 4-5%, reflecting the back up in interest rates.

A rising trend in the $A is likely into next year, reflecting a downtrend in the overvalued $US and the Fed moving to cut interest rates before the RBA.

Eurozone shares rose 1% on Friday and the US S&P 500 rose 0.4% helped by solid but still cooling jobs data (there was a stronger than expected rise in payrolls but plenty of evidence of further cooling beneath the surface), a rise in consumer sentiment and falls in consumer inflation expectations. The positive global lead saw ASX 200 futures rise 16 points, or 0.2%, pointing to a positive start to trade for the Australian share market on Monday.

EndsImportant note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.