Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the cash rate.

Key points- The RBA raised its cash rate by 0.25% taking it to 4.35%.

- The RBA retained a tightening bias underpinned by relatively hawkish commentary in its post meeting statement but softened it somewhat.

- The move was in line with the consensus of economists and our view (although we thought it was a close call and until a few weeks ago thought that the RBA was finished hiking). The money market had priced in about a 60% probability of a rate hike for November.

- The decision to hike is consistent with hawkish commentary from the RBA in the last few weeks, higher than expected underlying inflation in the September quarter and recent stronger than expected retail sales and lower than expected unemployment.

- However, it’s likely to have been a close call for the Board given ongoing signs of slowing in the jobs market, weak per capita consumer spending, rising levels of mortgage stress, the ongoing downtrend in inflation and the significant rise in interest rates that has already occurred.

- Our concern remains that the RBA has tightened more than necessary with a high risk of recession.

- As a result, while the risk is still on the upside for the cash rate in the short term with 40% chance of another hike, the RBA probably won’t have to act again on its tightening bias, and we continue to see it cutting rates next year starting around mid-year.

The RBA has lived up to its reputation of interest rate moves on Melbourne Cup Day, clearly sees the higher-than-expected September quarter inflation outcome as “material” and reinforced the inflating fighting credentials and independence of the RBA under new Governor Michele Bulloch.

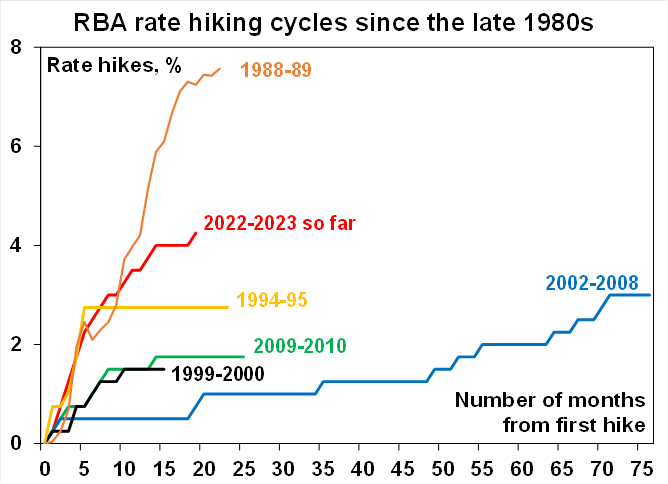

The resumption of rate hikes after a four month pause adds to what is already the biggest interest rate hiking cycle (13 rate hikes totalling 425 basis points over 17 months) since the late 1980s which preceded the early 1990s recession. While interest rates are still much lower today than back then, the risks to the household sector are much higher now because household debt to income levels are three times greater than they were in the late 1980s.

Source: RBA, AMP

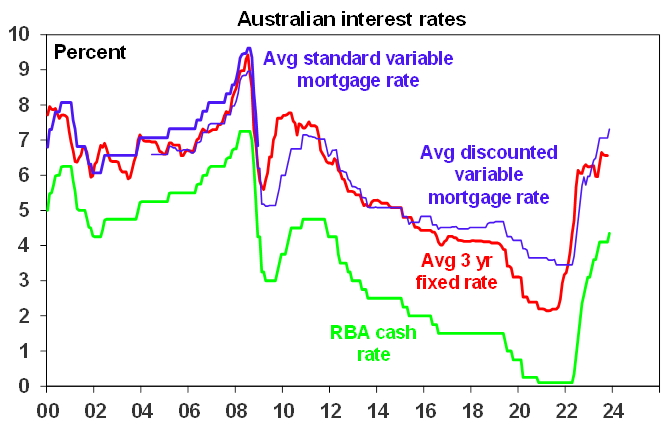

The rise in the cash rate is likely to be fully passed through to bank mortgage rates which will take them to levels last seen in 2008, which for some who were on sub 2% fixed rates two years ago will mean an almost four-fold increase in their mortgage rate.

Source: RBA, AMP

In resuming rate hikes, the RBA noted that since the August Board meeting when it last revised its economic forecasts: the risk of higher for longer inflation has increased; while growth has slowed it has been stronger than expected; labour market conditions have eased but are still tight; and home prices are continuing to rise. In particular it notes that while inflation is falling, its still too high and proving to be more persistent than thought back in August with many services prices rising briskly. As a consequence, it has revised up its inflation forecast for the end of next year to 3.5% (from 3.25%) and appears to have revised up its end 2025 inflation forecast to the top of 3% (from 2.75%). Its also revised down the expected rise in unemployment to 4.25% from 4.5%.

As such it clearly regards the upwards revision to its inflation forecasts as “material” and something that it warned it would have no hesitation in raising rates again in response to – which they have now done. The RBA remains concerned that higher for longer inflation will boost inflation expectations making it even harder to get inflation back to target. As a result, “the Board judged that an increase in interest rates was warranted…to be more assured that inflation would return to target in a reasonable timeframe.”

In noting that “there are still significant uncertainties around the outlook” today’s decision is likely to have been another close call with the Board also considering the case to remain on hold but deciding the stronger case was to raise rates again.

Interestingly the RBA softened somewhat its tightening bias by replacing “some further tightening of monetary policy [ie rate hikes] may be required to ensure that inflation returns to target in a reasonable timeframe” with “whether further tightening of monetary policy is required…”, but its still a tightening bias and its been underlined by relatively more hawkish language in its post meeting statement compared to last month. And it effectively reiterated that this will depend on how the data evolves and that it will continue to look closely at the global economy, domestic demand, inflation and the labour market.

We would concede that the near-term risk of another rate hike is high particularly with still high inflation, the risk that higher petrol prices will add to inflation expectations and some signs of a pickup in wages growth. Our assessment is that the risk of another hike is around 40%. Key to watch ahead of the December Board meeting as to whether there will be another rate hike will be September quarter wages data on 15 November, October jobs data on 16 November and retail sales and monthly inflation data later this month.

However, our assessment remains that that the RBA has already done more than enough to slow the economy in order to rebalance demand and supply and bring inflation back to target. Rate hikes impact the economy with a long lag as it takes a while for the hikes to be passed through to borrowers and for them to adjust their spending. This time around the lag has been lengthened by savings buffers built up in the pandemic, the reopening boost, more than normal home borrowers locking in at 2% of so fixed mortgage rates in the pandemic and the highly competitive mortgage market which has meant that actual mortgage rates paid on outstanding mortgages have gone up by less than the cash rate. However, these protections are now wearing off.

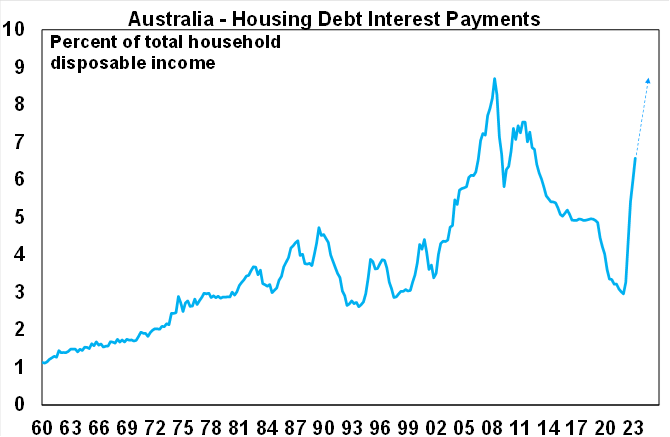

Consistent with this, mortgage interest payments as a share of household income are already on their way to a record high as past rate hikes flow through and today’s move will accentuate this. The latest 0.25% rate hike will mean an extra $100 a month in additional debt servicing payments on a $600,000 loan and would take the total increase since April last year to an extra $1400 a month or $17,000 a year. Even if a borrower has secured a 0.5% cut to their mortgage rate their payments would be up an extra $14,900 a year since April last year. And the RBA’s own analysis points to around one in seven households with a mortgage already being cash flow negative in July which will likely have now increased further. This will mean a big hit to household spending power which will remain whether rates have stopped rising or not.

Source: RBA, ABS, AMP

While the data is noisy, we are seeing ongoing evidence that rate hikes are biting with real per person retail sales down 4% on a year ago, a sharp fall in building approvals from their highs, slowing business investment plans, a slowdown in GDP growth and job vacancies well down from their highs and combined this is likely to continue to bear down on underlying inflationary pressures. While high petrol prices are a concern, the rise since mid-year in the context of stretched household budgets is more likely to act as a tax on spending rather than as a further impetus to underlying inflation.

Continuing to raise interest rates will only add to the already very high risk of unnecessarily knocking the economy into recession.

So while the risk of another near term rate hike remains high and we have been too optimistic on rates, our base case is that rates have peaked and that the cash rate will gradually start to fall through the second half of next year.

Given the lags involved and the increasing signs that monetary tightening is working it makes sense for the RBA to remain on hold so it can better assess the impact of the rate hikes so far and its latest move.

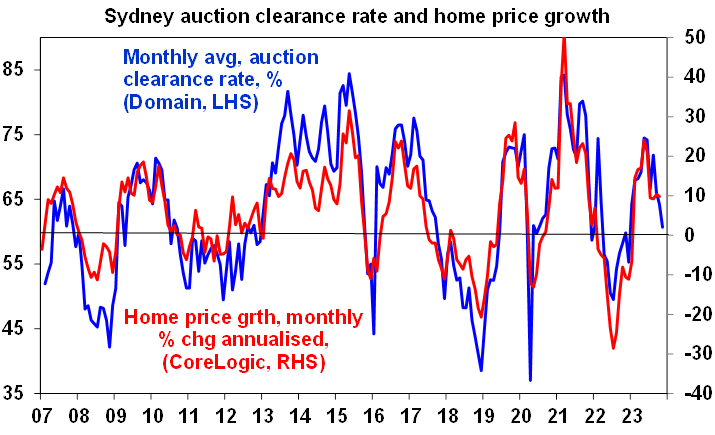

And finally... the latest interest rate rise along with the fear of more to come adds to the risk that high interest rates are starting to get the upper hand again in the property market after gains this year on the back of the housing supply shortfall in the face of booming immigration. The downtrend in auction clearance rates since May is already pointing to a sharp loss of momentum in home price growth.

Source: Domain, CoreLogic, AMP

EndsImportant note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.