Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses home prices.Key points:

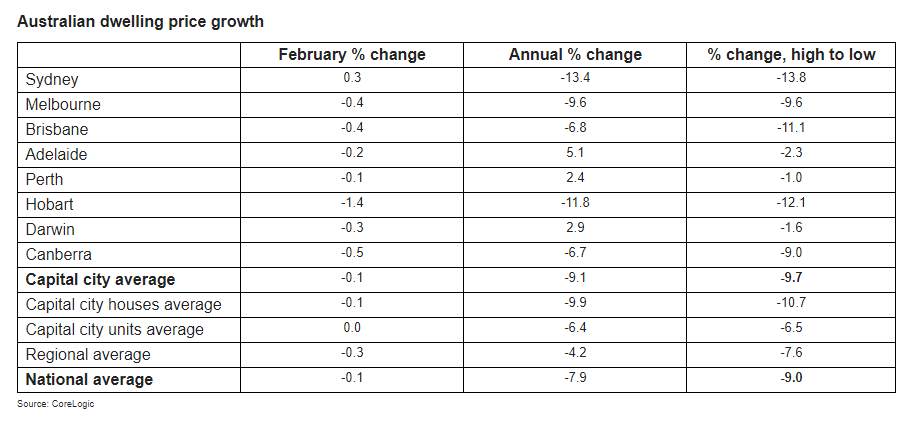

- Australian national average home prices fell 0.1% February, making it their tenth monthly fall in a row but it’s also their smallest monthly fall since May last year.

- From their April 2022 high national average prices are now down 9%, their biggest fall on CoreLogic records back to 1980.

- But Sydney prices actually rose 0.3% in February (after a 13.8% fall).

- And while prices in other cities and regional areas continued to fall their rate of decline slowed, except in Darwin.

- The February stabilisation suggests some upside risk to our home price forecasts but we continue to expect a 15-20% top to bottom fall out to the September quarter, as the full impact of rate hikes flows through and as economic conditions slow sharply this year resulting in rising unemployment.

- Reflecting this, and given the 9% fall in prices that has already occurred, we still see around another 8% or so fall in prices ahead.

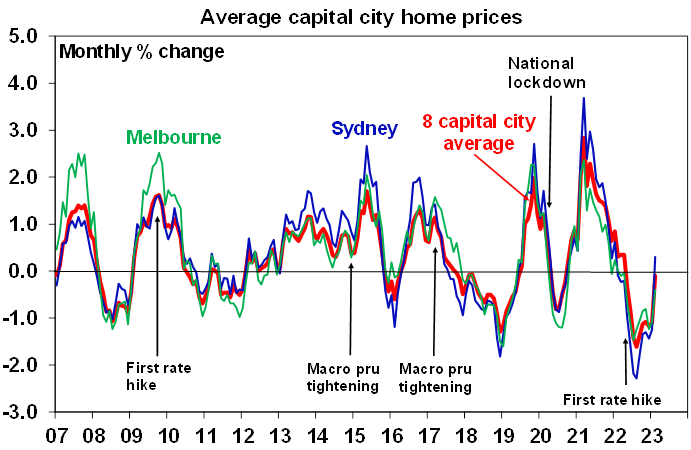

Is the Australian home price cycle turning back up?

After falling a record 9% from their high early last year based on CoreLogic data back to 1980, February home price data saw a sharp slowing in average home price falls across most cities and regional areas with Sydney prices even rising slightly. It is consistent with a solid February for auction clearance rates. This begs the question whether the home price cycle is now turning up again. It’s possible that it is starting to turn up again given the rapid return of immigration and the tight rental market and the Australian housing market does have a tendency to surprise on the upside.

Source: CoreLogic, AMP

However, while the stabilisation in February suggests some upside risks to our forecasts, we are a bit sceptical and our base case remains for a top to bottom fall of 15-20% in prices with about another 8% or so to go out to around the September quarter.

- The improving trend in February likely reflected the return of bargain hunters after a period of sharp price falls and a bit of “FOMO” (or fear of missing out) demand helped along by very low listings and optimism coming into the year that interest rates were close to peaking.

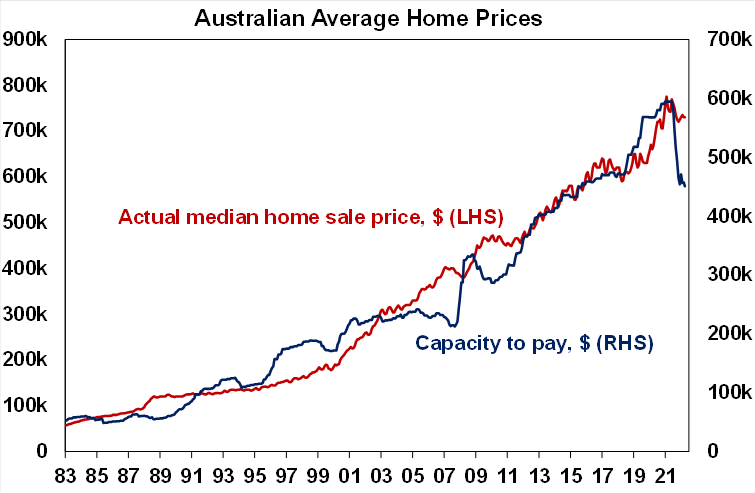

- However, we have yet to see the full impact of past rate hikes in mortgage payments, the RBA has now become more hawkish and is signalling several more rate hikes to go with the consensus now seeing the cash rate rising above 4%, the capacity to borrow and hence pay for property is down 25% from its high last year (see the next chart), the combination of the fixed mortgage reset which will see 880,000 mortgages face more than a doubling in their interest bill this year and the increasing risk of recession with much higher unemployment will weigh on demand with the risk that debt servicing problems for some home owners will start to also boost supply.

- It’s worth noting that the 2010-12 and 2017-19 price fall cycles saw periods where falls moderated or partially reversed only to resume falling.

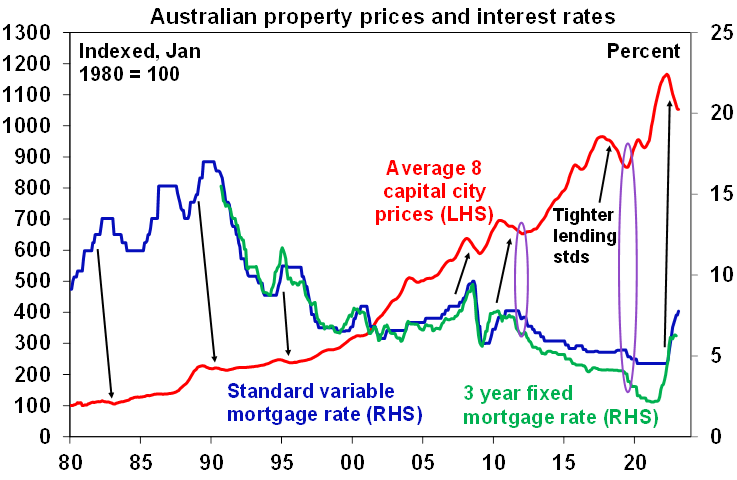

- The last two major upswings in property prices that started in 2012 and 2019 required rate cuts before prices started to rise - see the purple ovals in the final chart below. Right now, we don’t anticipate rate cuts to start until late this year or early 2024.

Partly based on a Deutsche Bank analysis. Source: RBA, CoreLogic, AMP

Source: CoreLogic, AMP

The main risks on the downside to our view is that the RBA raises the cash rate to above 4% (as many are now forecasting) and the economy enters recession. The RBA has already raised rates by more than the 2.5% interest rate serviceability buffer that applied up to October 2021 so many mortgage holders are now paying rates above those that their bank assessed them on. In this scenario home prices risk falling by around 30% from their high.

On the upside several factors will help put a floor under prices and eventually help drive recovery. These include: government support programs; the tight rental market; & rapidly rising immigration. And of course, there is always the risk that these considerations drive an upswing earlier than we are anticipating.

But for now, the property market will likely be dominated by high and still rising mortgage rates and so further falls in prices are likely despite the stabilisation seen in February.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.