Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the RBA rate hike.

Key points:

- The RBA raised the cash rate by another 0.25%, taking it to 3.1% as widely expected.

- This is the eighth-rate hike in a row and brings the total increase in rates to 3% since April.

- While recent data for jobs and wages were solid and the RBA is concerned about a “prices-wages” spiral, sticking to the more moderate 0.25% pace of rate hikes rather than reverting to 0.5% hikes makes sense given the sharp rise in interest rates seen so far, to allow time for the lags in the way monetary tightening impacts the economy to play out and given the high risk of global recession.

- The RBA retained its tightening bias but softened it slightly, noting in its Statement that “it is not on a pre-set course”.

- Our base case is that the cash rate has now peaked at 3.1%, but with the RBA still retaining a tightening bias and upside risks of wages growth there is a high risk of one final 0.25% hike to 3.35% in February. By end 2023 or early 2024 we expect the RBA to start cutting rates.

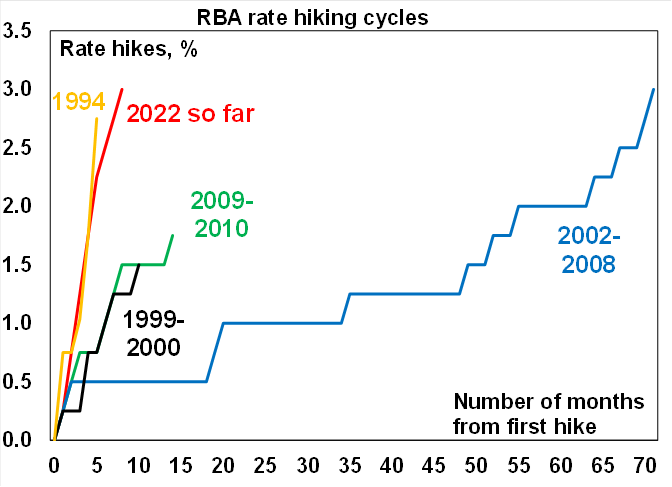

The 3% (or 300 basis point) increase in the cash rate over the eight months since April now exceeds the 1994 tightening cycle - of 275 basis points but spread over 5 months - and equals the 2002-2008 tightening cycle - which amounted to 300 basis points but spread over 71 months. The speed of the rate hikes compared to the last three tightening cycles reflects the extent of the blow out in inflation and the low starting point for the cash rate.

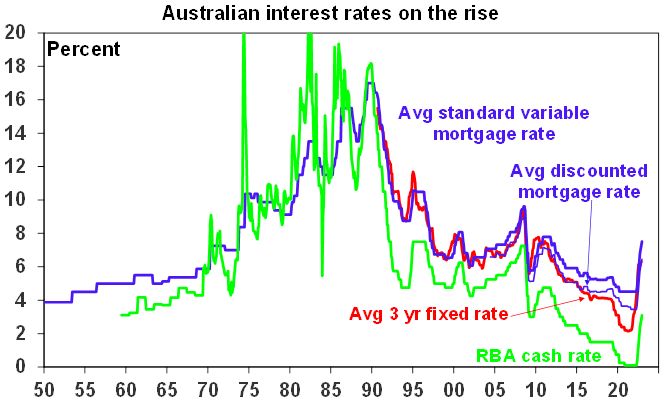

Further rate hikes from here will exceed the tightening cycles seen since 1990. Prior to 1990 the RBA cash rate was not officially announced, and short-term rates were very volatile. In the period January 1988 to November 1989 the overnight cash rate rose from 10.6% to 18.2% but mortgage rates were more regulated then and “only” rose from 13.5% to 17%. See the second chart below. Of course, household debt as a share of income was only 68% back then whereas its now 187% so rates shouldn’t have to go up anywhere near as much as they did in the 1980s to slow spending and hence inflation.

Source: RBA, AMP

In raising rates again, the RBA reiterated that: inflation remains too high; its still expected to rise to 8%yoy this quarter; the economy is still growing solidly; the labour market remains tight; wages growth is continuing to pick up; and its “priority is to return inflation to the 2-3% target” and remains “resolute” in its determination to do this and “will do what is necessary” to achieve it.

However, the RBA also reiterated that: it has already increased interest rates materially; monetary policy operates with a lag; and it wants to keep the economy on an even keel. All of which probably explains why it has opted to stick to a 0.25% hike rather than revert to 0.5%. While it has referred to the possibility of a pause the Bank probably concluded it was too early for that, particularly as it does not meet in January.

The RBA’s bias remains hawkish, restating that “the Board expects to increase interest rates further over the period ahead”, but it added the qualifier “that it is not on a pre-set course”. While it has said this before in other commentary, its addition to the post meeting Statement makes it sound a little bit less hawkish and it more clearly paves the way for a pause.

Banks are likely to pass the RBA’s rate hike on in full to their variable rate customers. This will take variable mortgage rates to their highest levels since 2012. In other words, roughly 10 years of falling mortgage rates have been reversed in eight months. This may not have hit spending much yet, but it will in the months ahead and through next year, particularly as roughly two thirds of fixed rate mortgage customers reset next year to fixed rates that are more than double current levels.

The rise in mortgage rates is now well above the 2.5% interest rate serviceability test that applied for borrowers until October last year and is now equal to the 3% that applied from October last year. So many recent home borrowers will now be seeing rates above the levels their serviceability was tested at when they took out their loan.

Source: RBA, Bloomberg, AMP

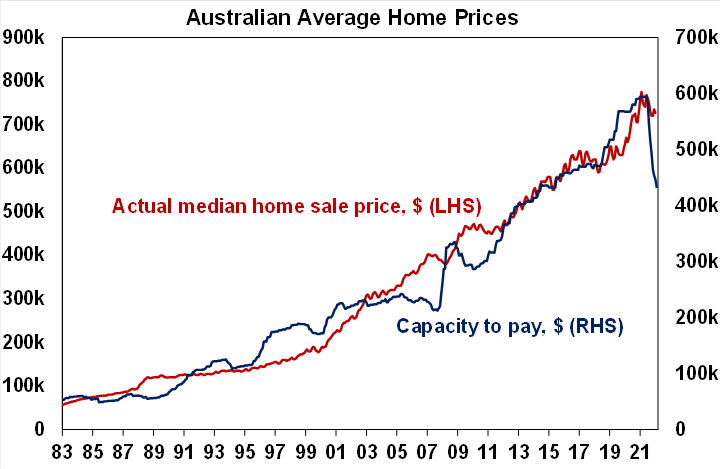

The latest interest rate hike when passed on to mortgage rates will mean that the amount a new buyer on average full-time earnings with a 20% deposit can pay for a home will have fallen 27% from what it was in April – see the Capacity to Pay line in the next chart. So the downwards pressure on property prices will continue for some time yet even if the RBA soon pauses the cash rate.

Source: RBA, CoreLogic, AMP

So far, the jobs market remains tight and consumer spending has been strong. However, based on past experience this is not particularly surprising and reflects the way interest rates changes affect the economy with a lag.

While global central banks are continuing to move rates up in faster increments its worth noting that the RBA meets 11 times a year compared to 8 or less for many other central banks and so it gets more goes at it. And compared to the US where 95% of mortgages are 30 year fixed rate loans Australian households are far more sensitive as 60% of mortgages are variable rate and the 40% on fixed rate loans are only short dated mostly going out 2 or 3 years. Finally, the $A has remained relatively resilient posing no significant risk to inflation. So, there is no logical reason for the RBA to follow the Fed and other central banks with supersized rate hikes. And in any case, even the Fed is on track to slowdown next week.

With the cash rate having reached our (admittedly previously upwardly revised) peak forecast of 3.1%, we remain of the view that the RBA is at the peak (or if not then its close to it).

- First, global supply bottlenecks are continuing to dissipate with sharply reduced delivery delays, lower freight costs and most commodity prices well off their highs.

- Second, while electricity prices likely have more upside, oil and hence petrol prices look to have peaked which means their contribution to ongoing inflation will likely be zero or negative through next year.

- Third, many households will experience a significant amount of pain from the combination of falling real wages and higher mortgage rates. In terms of the latter, a variable rate borrower on an existing $500,000 mortgage (which is the average) will see roughly another $80 added to their monthly payment from today’s RBA hike which will take the total increase in their monthly payments since April to around $900 a month. That’s an extra $11,000 a year which is a massive hit to household spending power. And roughly two thirds of the 40% of mortgaged households with fixed rates will see a doubling or more in their payments when their fixed term expires by the end of next year. This will result in a sharp slowing in consumer spending which will sharply reduce corporate pricing power.

- Fourth, there is increasing evidence that rate hikes are starting to bite: housing related indicators are all very weak; falling home prices will depress consumer spending via a negative wealth effect; consumer confidence remains at recessionary levels; bank card spending data indicates a slowing in discretionary spending; retail sales look to now be falling in real terms (only sounding high because of high prices); and there are some signs of slowing jobs growth. While quarterly inflation remains high and is still rising, the ABS monthly Inflation Indicator looks to be slowing for the roughly 70% of goods and services that it covers.

- Finally, the risk of global recession next year is now high, and this will weigh on imported inflation and further dampen Australian economic growth which we see slowing sharply next year, which will all help push down our inflation rate through next year.

In summary, we see the RBA as being at or close to the peak on rates. Our base case is that we are now at the peak, albeit with the high risk of one final 0.25% hike to 3.35% early next year. By early next year we expect that the combination of a sharp slowing in domestic demand, increasing signs that inflation has peaked and sharply weaker global growth which will in turn also drive inflation down will enable the RBA to keep rates on hold for an extended period. By late next year or early 2024 we expect the RBA to start cutting rates.

Our view remains below the consensus of economists - which sees a peak in the cash rate at 3.55% in the June quarter next year - and the money market - which sees a peak at 3.69% in December next year (which is well down from 4.2% a month ago). As noted above we concede that the risk to rates remain on the upside in the near term with the main risk being a further faster than expected pick up in wages growth running the risk of a “wage-price” spiral.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.