Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, the coronavirus, economic activity trackers, major global economic events and Australia economic events.Investment markets and key developments over the past week

US shares pulled back a bit after their post US CPI surge, with various Fed officials noting that there is still more work to do on inflation. This left US shares down 0.7% for the week and Japanese shares down 1.3%, but European shares rose 0.8% and Chinese shares rose 0.4%. Reflecting the soft US lead, Australian shares fell but only by 0.1% for the week with gains in material and IT stocks offset by falls in property and telco shares. Bond yields were little changed in the US and Japan but fell in Europe and Australia. Oil and metal prices fell sharply on growth concerns but the iron ore price rose. The $A fell back a bit as the $US rose but is still around $US0.67.

While share markets ran a bit ahead of themselves after the lower-than-expected October US CPI and we could see more volatility in the short term, there have been more positive developments over the past week:

US producer price and import price inflation for October slowed more than expected adding to signs that we have seen peak inflation in the US.

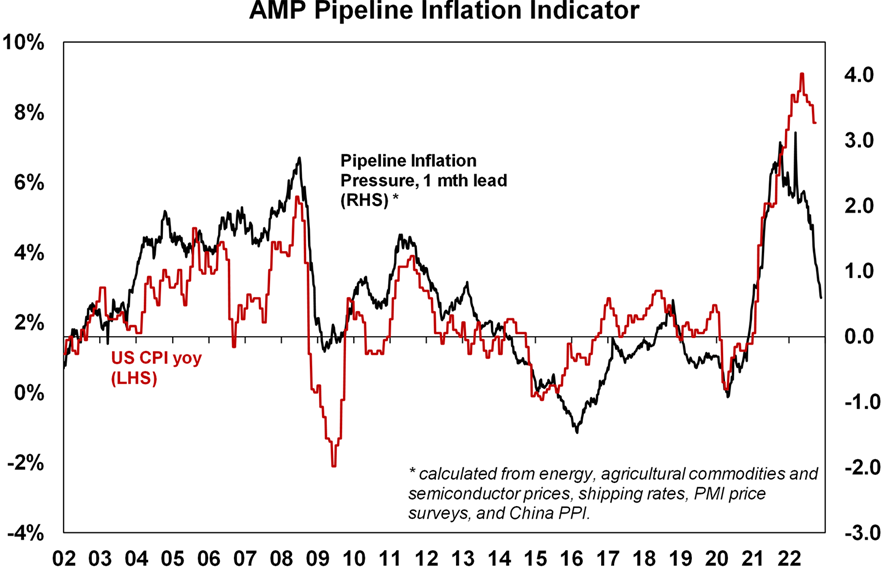

Our Pipeline Inflation Indicator is continuing to trend down (with falls in gas and coal prices and lower shipping rates in the last week) and points to a further fall in US inflation.

Source: Bloomberg, AMP

While numerous Fed speakers over the last week indicated the Fed has more work to do as inflation remains too high, most noted the importance of lags in the way monetary policy impacts and indicated an openness to slowing the pace of rate hikes. The Fed seems to be moving to get off the hamster wheel of 0.75% hikes as monetary policy is now tight and there are signs of slowing growth & easing inflation pressures. This is a positive sign for investment markets.

In Australia, the minutes from the last RBA board meeting were balanced but reiterated an openness to pausing interest rate hikes for a while as it assessed the outlook. Strong September quarter wages growth and jobs data for October along with the absence of an RBA meeting in January suggest that a pause is unlikely in December though and we continue to expect another 0.25% rate hike but a pause is likely from early next year where we expect the cash rate to peak at 3.1% (or if not then at 3.35%).

Meetings between President Biden and PM Albanese on the one hand and President Xi Jinping on the other indicated a possible thawing in the relationship with China that had become fraught lately.

China is showing more signs of supporting its economy with an easing in covid policies and property support measures.

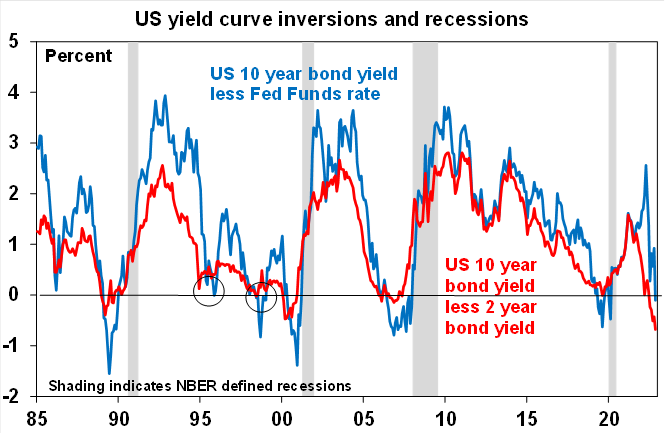

Of course, various countries inflation rates (including in the UK with 11.1% inflation in October, and in Australia) are lagging the US, central banks are still hawkish, the risk of a hard landing globally and in Australia remains high (with US yield curves now more firmly inverted) and geopolitical risks remain high so the ride for shares is likely to remain choppy and new short-term lows can’t be ruled out. However, increasing evidence of a peak in US inflation – which led inflation in other countries including Australia - and less hawkish central banks help provide confidence that shares will be higher on a 12-month horizon.

Source: Bloomberg, AMP

Take outs from the US mid-terms – no GOP wave, just a little ripple. Given the state of the US economy and inflation the Republicans should have easily picked up around 50 seats in the House and got control of the Senate. As it turns out thanks to the abortion issue and some Republicans turning off Trump and Trump supported candidates, they look to have picked up around just 8 seats giving just a wafer thin majority in the House & the Democrats kept control of the Senate. Here are key take outs:

This is still divided Government (which will limit extreme economic policies that may be negative for investment markets) and the uncertainty is out of the way so shares are not precluded from their usual rally over the 12 months following the mid-terms.

With the passage of domestic policies through Congress now more difficult President Biden is likely to adopt a more hawkish foreign policy stance keeping geopolitical risk high.

Battles over funding the Government (to avoid a shutdown) and to raise the debt ceiling (to avoid default) are still likely. Fortunately, in terms of the former a one-year funding bill may pass by the 16th December deadline.

While Trump has confirmed he will run again in 2024, the chances of him returning and causing the sort of mayhem seen in 2017-2020 may be low as many Republicans now blame him for the poor mid-term result, their 2020 loss and the 2020 loss of the Senate so now that he is no longer seen as a vote winner he may struggle to get the Republican nomination for 2024 with Florida GOP Governor DeSantis far better placed.

The Democrats relatively strong result & GOP infighting means they have a better chance of winning back the House & retaining the presidency in 2024

The crypto crumble. Trying to unravel what went wrong at FTX crypto exchange will take a while. I gave up after getting lost in jargon. The best quotes I saw in relation to it were: “Who could’ve predicted an asset with no intrinsic value would become worthless?” (New York Times Pitchbot Twitter account) and “its partly fraud and partly delusion” (Charlie Munger). Maybe both are a bit harsh as there is value in blockchain technology and in tokenising real asset ownership, but disentangling that from the mania around crypto is next to impossible. The idea that someone can just create a coin and start trading it is, as Munger said, “crazy”. And crypto currencies have not delivered on their claimed benefits – to be a hedge against inflation, a reliable store of value, a diversifier against other assets and to allow quick and cheap transactions. Bitcoin’s adoption in El Salvador has not gone well, to say the least. Cryptos remain incredibly volatile and lately their price moves have just been a souped-up version of shares. And cryptos have remained beset by hackers and fraud along with vehicles for criminals to extort ransoms. With no clear intrinsic value they have just been things to speculate on but have required an ongoing flow of new “investors” coming in to keep prices rising. And it’s not at all clear that regulation will solve the problems. Wasn’t their unregulated nature supposed to be a key benefit? And regulation risks breaking the beliefs that allowed cryptos to rise. The key for investors is not to invest in things: where the use case is unclear and value is very hard to determine; where the investment is so complex you can’t understand it; and where the case for it rests heavily on past performance.

The RBA to stick to simpler, qualitative guidance after the difficult experience of the last year. Through the pandemic the RBA like many central banks moved to provide quite specific guidance about how long it would keep interest rates down and what would be required to raise them. The RBA concluded that this helped the economy early in the pandemic by lowering funding costs but caused problems more recently as the guidance not to raise rates before 2024 was misinterpreted as a “promise” and then the forecasts it was based on turned out to be wrong requiring rate hikes from May leading “to considerable reputational damage to the Bank”. While the RBA was well intentioned in trying to help the economy in a period of extreme uncertainty and in trying to be transparent, and the media played a role in misinterpreting the guidance, the whole episode highlights the problems for the RBA (and any central bank) in providing too much information and providing precise forecasts for interest rates either in level or time based terms. Precise forecasts for anything either in terms of levels or timing tend to be latched on to and imply greater precession in forecasting than is ever warranted and get interpreted in a way that dominates any qualitative conditions that may accompany them. Moving back to a more qualitative approach (unless in exceptional circumstances and even then staying away from time based guidance) and letting the market work out expected moves in rates is welcome.

If the inflation in prices re-sellers are asking for Taylor Swift’s New Eras stadium tour – up to $US28,000 - are any guide then the Fed has lots more to do. That said, while demand in a fan pre-sale was huge (with 3.5 million registered verified fans) it was exaggerated by “bot attacks” driving 3.5 billion ticket requests on Ticketmaster causing its website to crash. Ah well, one can always settle for searching for easter eggs in Taylor’s videos of which there are lots in Bejeweled.

Coronavirus update

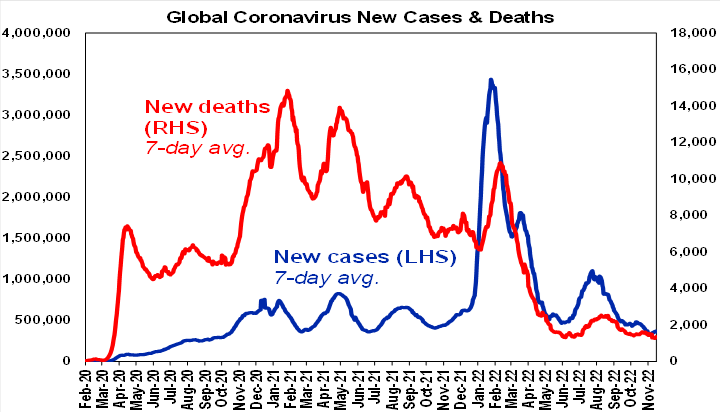

New global covid cases rose slightly in the last week due to a rise in Asia but new cases and deaths remain low. New cases in China have continued to surge, but China appears to be getting closer to an exit from zero Covid next year.

Source: ourworldindata.org, AMP

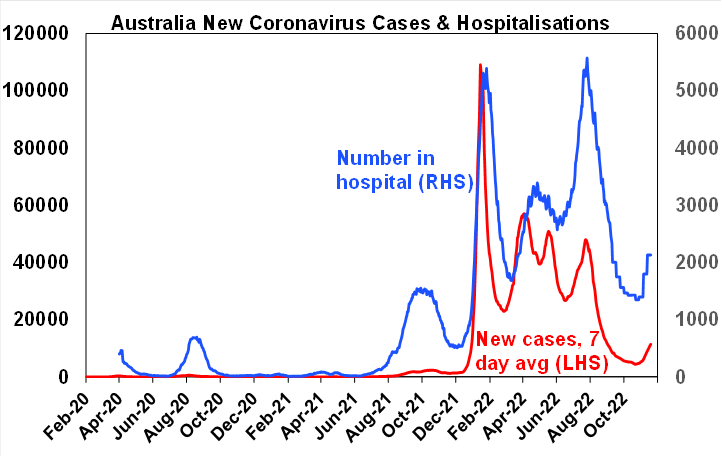

New cases and hospitalisations are continuing to rise in Australia, but the new Omicron variants do not appear to be more harmful and fully vaccinated people remain less likely to fall seriously ill. Singapore saw a similar wave recently that quickly rolled over again. So, significant economic disruption is unlikely.

Source: covidlive.com.au, AMP

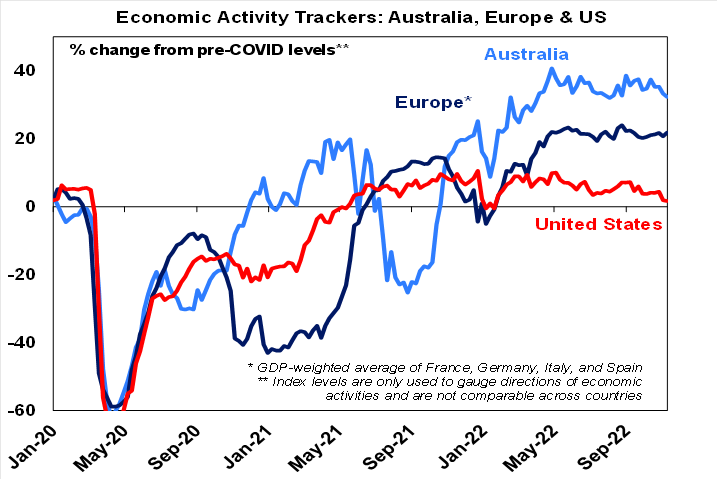

Economic activity trackers

Our Australian Economic Activity Tracker fell over the last week with card spending and restaurant and hotel bookings down. Our US Tracker also fell but our European Tracker rose.

Based on weekly data for eg job ads, restaurant bookings, confidence, credit & debit card transactions, retail foot traffic hotel bookings. Source: AMP

Major global economic events and implications

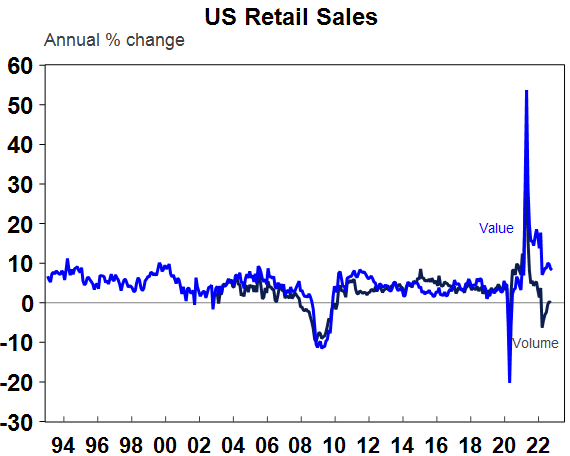

US economic data was mostly weak. Retail sales were far stronger than expected in October resulting in the Atlanta Fed’s GDP Now estimate for December quarter GDP growth rising to 4.4% annualised. So, still no real recession yet. New York regional manufacturing conditions improved in November, but they fell sharply in the Philadelphia region giving a weak average reading. Industrial production unexpectedly fell, home builder conditions fell to a new low and housing starts, home sales and the US leading index fell further. Initial jobless claims fell, but continuing claims rose further.

Source: Macrobond, AMP

Canadian inflation for October was unchanged at 6.9%yoy, remaining down from a high of 8.1%yoy in June.

UK inflation rose further to a 41 year high of 11.1%yoy in October. Higher food and energy prices were the main drivers though with core inflation unchanged at 6.5%yoy. This may prove to be the peak in UK inflation as the economy has slowed sharply and may have already slipped into recession, but the Bank of England is still likely to hike rates by another 0.5% at its December meeting taking its key rate to 3.5%. Meanwhile, the UK Government’s fiscal statement confirmed significant fiscal austerity with spending cuts and tax hikes amounting to around 2% of GDP after five years, although its mainly backloaded.

Japanese September quarter GDP unexpectedly fell, but this was mainly due to a surge in imports which looks like a bit of an aberration but could also be a sign of strength as consumer spending and business investment both rose. Meanwhile, CPI inflation rose further to 3.7%yoy with core (ex food and energy) inflation also rising but still only at 1.5%yoy. The BoJ won’t be rushing into monetary tightening, but it may slowly be getting closer.

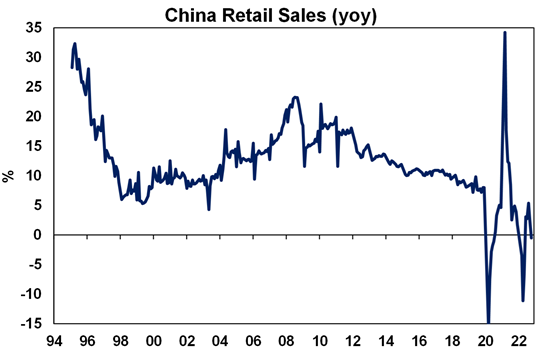

China slowed again in October, but the Government appears to be starting to focus more on boosting growth. Chinese economic activity data for October was weak with industrial production growth slowing again, retail sales falling 0.5% on a year ago, residential property sales and investment down sharply on a year ago and home prices continuing to fall. However, the Chinese Government has announced 20 measures to optimise is Covid policy (with some easing to contain the economic impact of restrictions and more medical preparations) and 16 measures to support the ailing property market.

Source: Bloomberg, AMP

Australian economic events and implications

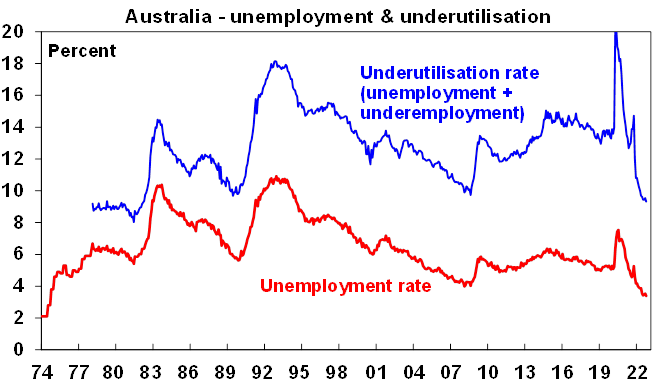

Jobs strong, wages up. Labour market data released over the last week was strong. Employment rose by a stronger than expected 32,200 in October driven by full time jobs, unemployment fell to a new post 1974 low of 3.39%, labour market underutilisation fell to 9.3% which is its lowest since 1982 and hours worked rose sharply (although this was partly due to less people than normal on annual leave). However, there are signs of a slowing. Reflecting a see-saw monthly pattern, average monthly jobs growth over the last 4 months has slowed to a crawl and a further slowing is likely in the months ahead as the cumulative impact of rate hikes slows demand and this plus the rapid return of net immigration boosting labour supply will start to push unemployment back up. And job openings are showing signs of having peaked.

Source: ABS, AMP

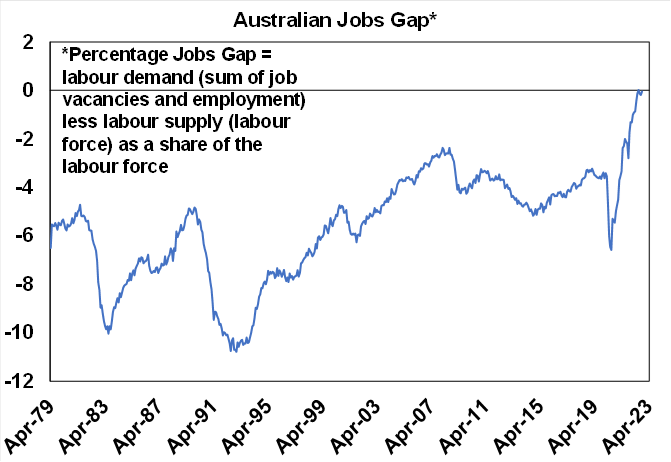

But for now, the jobs market remains very tight. This is evident in the “jobs gap” – defined as job vacancies plus employment less the labour force all as a percentage of the labour force – being at zero! As this hasn’t been seen until recently in the last 40 years at least it highlights just how tight the jobs market is. Slowing demand plus rising immigration will likely see it widen next year.

Source: ABS, AMP

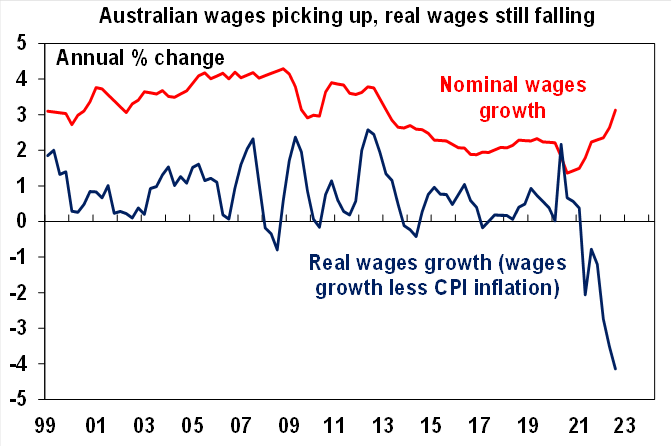

The tight jobs market is showing up in much stronger wages growth with a stronger than expected 1% rise in the September quarter taking annual wages growth to 3.1%yoy, its fastest since 2013. The acceleration has been mainly driven by those on individual agreements and the 4.6-5.2% rise in award wages.

Source: ABS, AMP

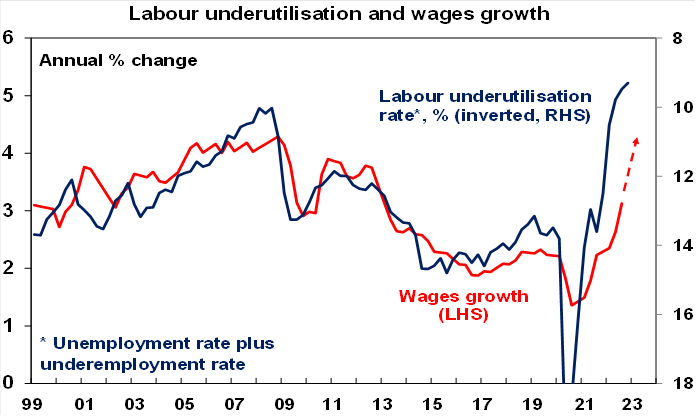

While real wages are falling, wages are clearly responding to the tight labour market with low labour market underutilisation pointing to a further rise in wages growth ahead.

Source: ABS, AMP

With wages growth rising & the jobs market tight, along with inflation still rising, it’s hard to see the RBA pausing next month and we continue to expect another 0.25% rate hike in December. That said, jobs and wages are lagging indicators and the RBA has indicated that its well aware of the lags and we continue to expect that by early next year there will be enough evidence of a slowing in growth and easing in inflation pressures to enable the RBA to stop tightening at 3.1% (albeit with upside risk to 3.35%).

What to watch over the next week?

The focus in the week ahead is likely to be on business conditions PMIs for November for major countries including Australia, which are likely to show ongoing soft conditions but will be watched for further easing in price and cost pressures.

In the US, the minutes from the last Fed meeting (Wednesday) will likely remain hawkish but will be watched for more commentary around slowing the pace of hikes going forward. Business conditions PMIs for November are likely to remain weak and new home sales are likely to show a further fall with both also due on Wednesday.

Eurozone business conditions PMIs for November (Wednesday) are likely to remain weak and Japanese business conditions (Thursday) may pull back a bit from October’s reasonable level.

The RBNZ (Wednesday) is expected to hike its official cash rate by another 0.5% taking it to 4%.

In Australia a speech by RBA Governor Lowe on “Price stability, the supply side and prosperity” will be watched for any more clues on interest rates – although its hard to see how he can add anything new and it would be kind of nice to have a speech on something other than the near term economic outlook and interest rates as its been done to death this year! Australian business conditions PMIs for November (Wednesday) are likely to slow a bit further.

Outlook for investment markets

Shares are not completely out of the woods yet as central banks continue to tighten, uncertainty about recession remains high and geopolitical risks continue. However, we are now in a favourable part of the year for shares from a seasonal perspective and we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary brakes.

With bond yields likely at or close to peaking for now, short-term bond returns should improve.

Unlisted commercial property may see some weakness in retail & office returns & the lagged impact of higher bond yields is likely to drag down unlisted property and infrastructure returns.

Australian home prices are expected to fall 15 to 20% top to bottom into the September quarter next year as poor affordability & rising mortgage rates impact. This assumes the cash rate tops out in the low 3’s but if it rises to 4% or so as the money market is assuming then home prices will likely fall 30%.

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

The $A remains at risk of further falls in the short term as global uncertainties persist and as the RBA remains a bit less hawkish than the Fed. However, a rising trend is likely over the medium term as commodity prices ultimately remain in a super cycle bull market.

Eurozone shares rose 1.1% on Friday and the US S&P 500 rose 0.5%. Reflecting the positive global lead ASX 200 futures rose 24 points, or 0.3%, pointing to a positive start to trade for the Australian share market on Monday.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.