Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the cash rate hike.Key points:

- The RBA raised the cash rate by another 0.25%, taking it to 2.85% as widely expected.

- This is the seventh-rate hike in a row, and brings the total increase in rates to 2.75% since April.

- While inflation surprised on the upside again in the September quarter and is still rising, sticking to the more moderate 0.25% pace of rate hikes makes sense given the sharp rise in interest rates seen so far, to allow time for the lags in the way monetary tightening impacts the economy to play out and given the rising risk of global recession.

- We expect the RBA to raise the cash rate by another 0.25% next month and now see the peak at 3.1%, albeit the risk remains on the upside in the short term. By end next year or early 2024 we expect the RBA to start cutting rates.

- Governor Lowe’s remarks tonight will no doubt be watched for any further guidance on rates.

- Market expectations for the cash rate to peak around 4.2% in a year’s time still look too hawkish and if realised would likely plunge the economy into recession and push home prices down by 30% or so from their highs earlier this year, resulting in financial stability issues.

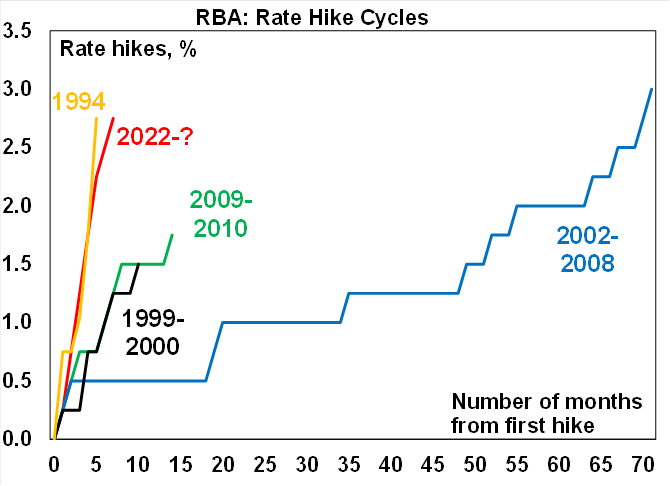

The 2.75% increase in cash rates has now caught up to the tightening cycle in 1994, although that one was a bit faster being over five months compared to over seven months this time around. The speed of the rate hikes compared to the last three tightening cycles though reflects the extent of the blow out in inflation and the low starting point for the cash rate.

Source: RBA, AMP

In raising rates again the RBA noted that: inflation remains too high; it has raised its inflation forecast profile for this year and next (now seeing 8% inflation by year end and 4.75% next year); the economy is still growing solidly; the labour market remains tight; wages growth is continuing to pick up; and its “priority is to return inflation to the 2-3% target” and remains “resolute” in its determination to do this and “will do what is necessary” to achieve it.

However, the RBA also noted that: it has already increased interest rates materially; monetary policy operates with a lag; it has further revised down its growth forecasts to 1.5% for the next two years; and it wants to keep the economy on an even keel. All of which probably explains why it has opted to stick to a 0.25% hike rather than revert to 0.5%. This makes sense in our view – despite the upside surprise in September quarter inflation now is the time for the RBA to stay in the slower lane to give it time to assess the impact of past rates hikes, particularly as downside risks to the global and Australian economic outlooks are now rising rapidly.

The RBA’s bias remains hawkish reiterating that it expects to raise “interest rates further over the period ahead”.

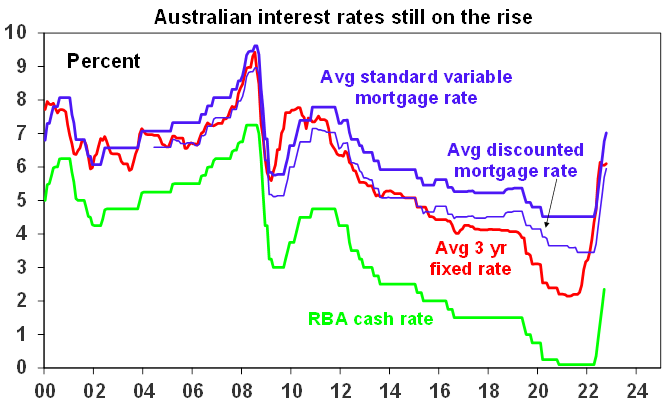

Banks are likely to pass the RBA’s rate hike on in full to their variable rate customers. This will take variable mortgage rates to their highest levels since early 2012. This may not have hit spending much yet, but it will in the months ahead and through next year.

Source: RBA, Bloomberg, AMP

So far the jobs market remains tight and consumer spending has been strong. However, based on the experience in the late 1980s ahead of the early 1990s recession this is not particularly surprising and its only a matter of time before spending starts to slow. So the RBA is right to be treading more carefully now.

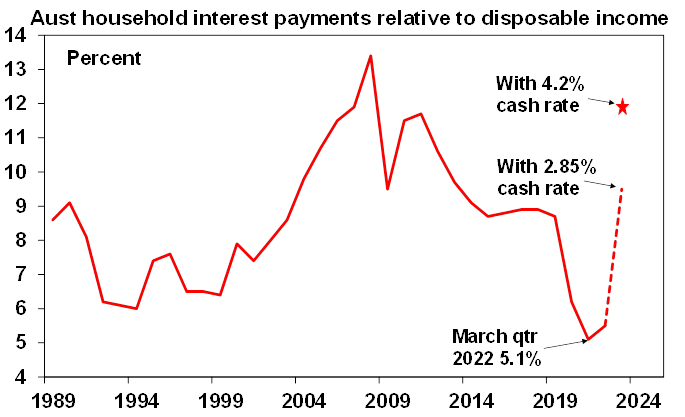

Money market expectations for a cash rate peak of around 4.2% in 12 months’ time are still too hawkish and would likely knock the economy unnecessarily into recession (as total mortgage payments would be pushed to record levels as a share of household income) and push property prices down 30% from their high of earlier this year.

While global central banks are continuing to move rates up in faster increments its worth noting that the RBA meets 11 times a year compared to 8 or less for many other central banks and so it gets more goes at it. And compared to the US where 95% of mortgages are 30 year fixed rate loans Australian households are far more sensitive as 60% of mortgages are variable rate and the 40% on fixed rate loans are only short dated mostly going out 2 or 3 years. Finally, while the $A has fallen against the $US, its been far more stable on a trade weighted basis and this is far more important for local inflation. So, there is no logical reason for the RBA to follow the Fed and other central banks with supersized rate hikes.

While we have revised up our cash rate forecast to a peak of around 3.1%, we remain of the view that the RBA won’t have to go much higher before demand cools enough to take pressure off inflation and keep inflation expectations down.

- First, global supply bottlenecks are continuing to show signs of improvement with reduced delivery delays, lower freight costs and most commodity prices off their highs.

- Second, while electricity prices likely have more upside, oil and hence petrol prices may have peaked which means their contribution to ongoing inflation may go to zero or negative through next year.

- Third, many households will experience a significant amount of pain from the combination of falling real wages and higher mortgage rates. In terms of the latter, a variable rate borrower on an existing $500,000 mortgage (which is the average) will see roughly another $75 added to their monthly payment from today’s RBA hike which will take the total increase in their monthly payments since April to around $810 a month. That’s an extra $9700 a year which is a massive hit to household spending power. And there is roughly a quarter of mortgaged households with fixed rates who will see a doubling or more in their payments when their fixed term expires by the end of next year. This will result in a sharp slowing in consumer spending which will sharply reduce corporate pricing power.

- Fourth, there is increasing evidence that rate hikes are starting to bite: housing related indicators are all very weak; falling home prices will depress consumer spending via a negative wealth effect; consumer confidence remains depressed; bank card spending data indicates a slowing in discretionary spending; retail sales have been roughly flat in real terms over the last two months; and there are some signs of slowing jobs growth. While inflation remains high and is still rising it is one of the last indicators to turn down in an economic downturn – so relying on the most recent inflation data to get a guide as to what future inflation will be is like driving using only the rear vision mirror.

- Finally, the risk of global recession next year is now high and this will weigh on imported inflation and further dampen Australian economic growth which we see slowing sharply next year.

Source: ABS, RBA, AMP

In summary, we see the RBA remaining in the slow lane and raising rates again by another 0.25% next month taking the cash rate to 3.1% which we expect to be the peak for this cycle as next year is likely to see a sharp slowing in growth and a significant fall in inflation. By late next year or early 2024 we expect the RBA to start cutting rates. We would concede though that the risk to rates remains on the upside in the near term.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.