Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, the coronavirus, economic activity trackers, major global economic events and Australia economic events.Investment markets and key developments over the past week

Shares had another volatile week, seeing yet another bounce earlier in the week and then falling again as inflation, rate hike and recession fears continued not helped by a continuing rise in bond yields. This left US and Eurozone shares up but Japanese and Chinese shares down. The Australian share market also fell with sharp falls in materials, health, utility and industrials more than offsetting gains in property shares. Bond yields fell in the UK as the 23rd September fiscal stimulus was largely reversed, but rose elsewhere with the US 10 year bond yield rising to its highest since 2007. Oil, metal and iron ore prices fell but the $A rose slightly as the $US fell.

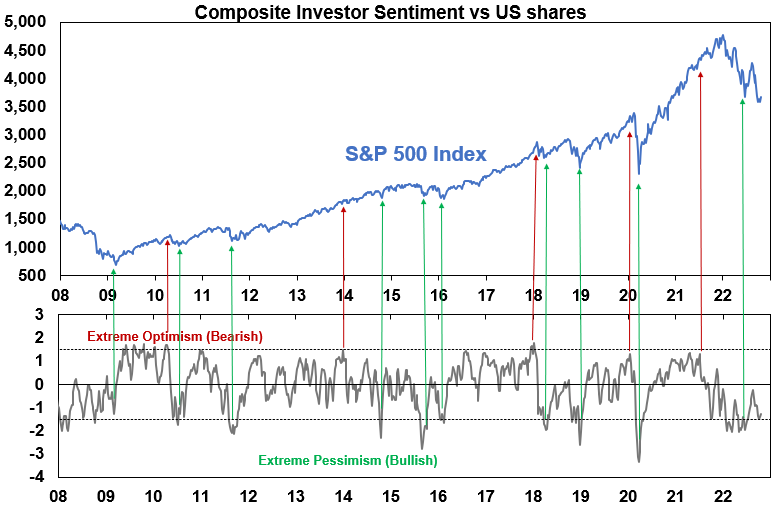

It’s been more of the same for investment markets. Shares have managed yet another bounce from technical support levels for US shares, and extremely bearish investor sentiment and oversold conditions suggest that they may have more upside.

Source: Bloomberg, Sentimentrader, Investors Intelligence, AMP

However, the macro backdrop for shares remains tenuous – with high inflation, hawkish global central banks, high recession risks and ongoing geopolitical problems – suggesting the near term risks remain on the downside. Specifically in the past week:

The UK, Canada and New Zealand all saw another round of high and greater than expected inflation readings for September pointing to 0.75% rate hikes from their central banks when they next meet.

German producer price inflation remained at a whopping 46%yoy.

US economic data was generally weak with housing indicators pushing to levels often associated with recession.

Fed officials remained hawkish and given this its hard to see the Fed paring back its quantitative tightening (ie running down its bond holdings) in order to stabilise bond yields as some appear to be suggesting.

Chinese President Xi’s Party Congress speech offered nothing really new but represented a continuing greater focus on national stability and security at the expense of economic reform and growth with no mention of an easing in covid policies (although some easing is likely as new treatments and vaccines become available) and easing of tensions over Taiwan (with Xi reiterating an intention to reunify Taiwan with China).

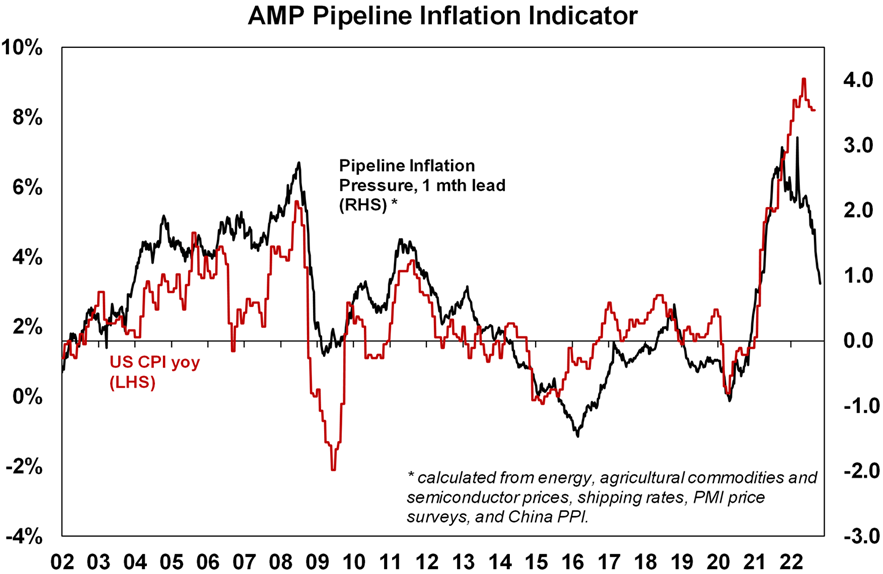

On the positive side though, signs of a slowing ahead in US inflation continue to build. A year ago global growth, US wages data, rents, commodity prices, US government spending, anecdotes, car prices, money supply growth, freight rates, business surveys and inflation expectations were all point up for US inflation. Now they are all slowing or clearly pointing down. And consistent with this, our Pipeline Inflation Indicator continues to slow. Once these start to show up in actual inflation they should enable the Fed to slow down the pace of hikes, hopefully early enough to avoid a recession or at least a severe recession. Inflation in Australia is lagging the US by around 6 months so if the lead from the US continues then it should start to decline here early next year.

Source: Bloomberg, AMP

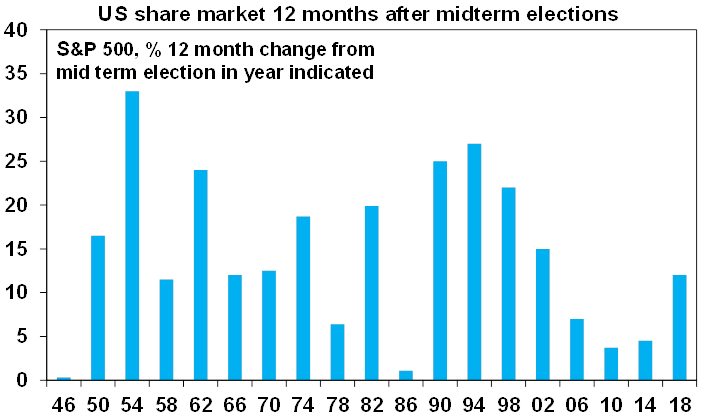

Seasonality also starts to become more positive for shares into year end and the US share market has consistently rallied after US mid-term election years with year 3 in the 4 year presidential cycle being a strong year on average after year 2 (ie this year) which is normally a poor year.

Source: Bloomberg, AMP

The recent UK financial mayhem has limited direct relevance to Australia, but does hold some important lessons. The past week saw the new UK Chancellor reverse most of the remainder of (former) PM Truss’ 23rd September fiscal stimulus and this further helped settle the UK bond and currency markets. Truss has now resigned with a new leader likely to be determined next week. An obvious question is what is the risk of the same happening elsewhere, including Australia. However, there is a danger in extrapolating the UK financial crisis of the last few weeks to other countries as it largely arose from UK specific factors. First the inexperience and poor timing of the new UK Government in embarking upon a surprise massive fiscal stimulus at a time of high inflation. And second the prevalence of defined benefit schemes in the UK pension industry which led to forced selling of assets like bonds and shares once pension fund asset values started to move out of whack with the liabilities of such funds. Which in turn accentuated the rise in UK bond yields. By contrast in Australia, the Government is not proposing a massive fiscal stimulus – if anything next week’s Budget is likely to see lower than previously projected budget deficits and the Stage 3 tax cuts are irrelevant as they are already budgeted for and don’t kick in for nearly two years. And our mostly accumulation superannuation funds (where the member gets what the fund is worth when they retire) do not face the same asset liability mis-matching issues as UK defined benefit funds (where the member is paid a ratio of final salary at retirement). However, the UK experience does hold some lessons for other countries.

First, bond investors won’t tolerate a surprise fiscal stimulus that looks inflationary in the current environment.

Second, it reminds us that there is a high risk in the current environment of tightening monetary policy and a rising $US of financial accidents. This is more an issue in emerging countries with high $US debt levels but could show up in leveraged or high-risk parts of developed countries investment markets.

The UK experience both in the last few weeks and its post Brexit debacle probably helps reduce the risk that the new Italian Government will go down a similar path - an Itexit remains off the table and any fiscal stimulus in Italy is likely to be small.

The RBA’s minutes from its last meeting and a speech by Deputy Governor Bullock highlighted that its prepared to take its own path to return inflation to target. The decision to hike 0.25% or 0.5% at the last meeting was “finely balanced” but it went with 0.25% for what I see as all the right reasons: the rapidity of rate hikes so far; the lags in the way rate hikes impact the economy; clear evidence that rate hikes were impacting in the housing market; more modest wages growth in Australia compared to other countries; the deteriorating global outlook; to allow time to assess the impact of rate hikes so far; drawing rate hikes out would underline its resolve; and the RBA meets more frequently than other central banks. The RBA clearly remains hawkish with its reference to “drawing out policy adjustments” and that returning inflation to target “was likely to require further increases in interest rates”. So it’s not done yet. But absent a shock horror inflation result in the week ahead its likely to stick to 0.25% increments going forward. Signs of slowing jobs growth also support the case for more cautious moves going forward and our assessment that we are near the peak in the cash rate. Our base case remains for a peak of 2.85% in the cash rate, but we accept the risk is on the upside but probably only to 3.1%. Money market expectations for the cash rate to rise above 4% next year still look way too hawkish as they would crash the economy and the property market.

The latest round of floods in Australia will disrupt growth and add a bit to inflation – but are unlikely to change the path for the RBA. Its still early days yet but my rough assessment would be that it will add around 0.2-0.3% to inflation in the current quarter mainly via higher fruit, vegetable and possibly diary and poultry prices. Its probably not going to change the outlook for the RBA’s cash rate unless the occurrence of yet another supply shock threatens to add to inflation expectations. It could knock 0.1-0.2% off December quarter GDP but as we have seen in the past its likely to be offset in subsequent quarters by rebuilding so I can’t see much impact on annual GDP growth. It could add $2bn or so to the budget deficit though.

Taylor Swift’s new album Midnights is imminent. A colleague suggested Out of the Woods from 1989 is a good one for investors right now with its chorus: “Are we out of the woods? Are we in the clear?” Out of interest Elvis had a song about Midnight – which was reportedly Priscilla’s favourite.

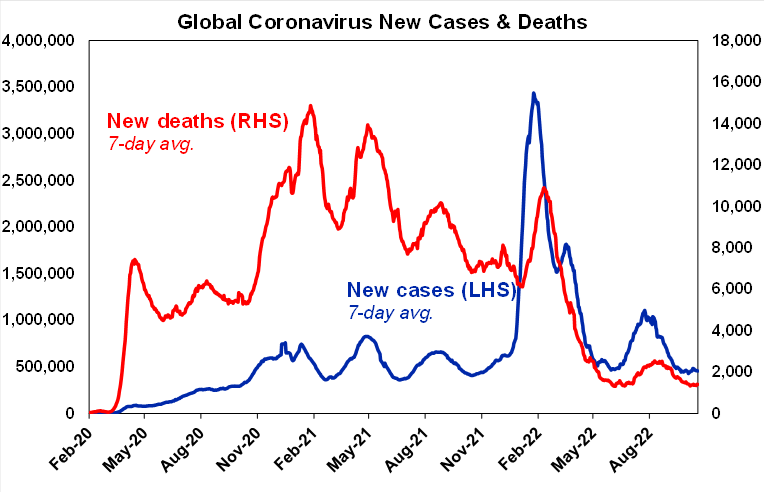

Coronavirus update

New global covid cases & deaths fell over the last week and remain low. Asia has seen a bit of a rise, but Europe looks to have slowed, China is trending down again and new cases, hospitalisations and deaths are still falling in Australia.

Source: covidlive.com.au, AMP

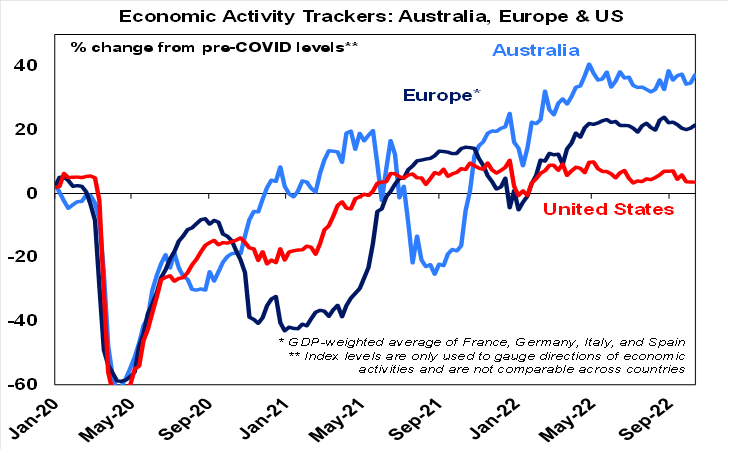

Economic activity trackers

Our Australian and European Economic Activity Trackers rose over the last week, but our US Tracker was little changed.

Based on weekly data for eg job ads, restaurant bookings, confidence, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

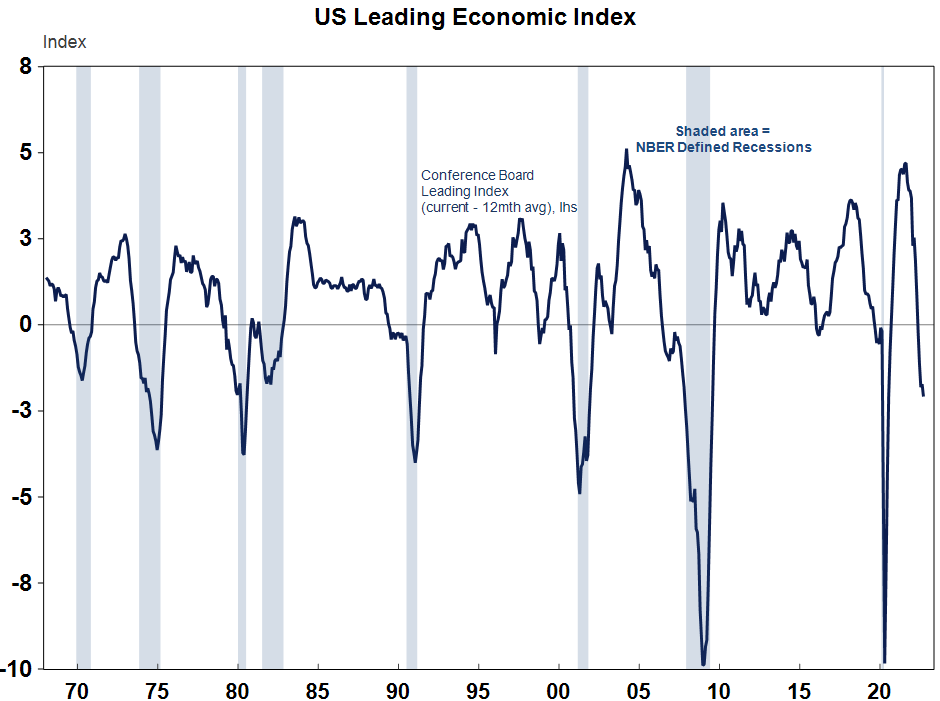

US economic data was mostly soft. Jobless claims remain low and industrial production was solid, but business surveys point to weakness ahead with both the New York and Philadelphia manufacturing surveys for October being weak. The US leading index in September fell to levels around where recessions have started in the past. Housing starts, home sales and home builder conditions all fell indicating that the interest sensitive housing sector is being hit hard by higher rates. Interestingly the Fed’s Beige Book of anecdotal evidence notes that while price and wages growth remain elevated there are pockets of easing.

Source: Macrobond, AMP

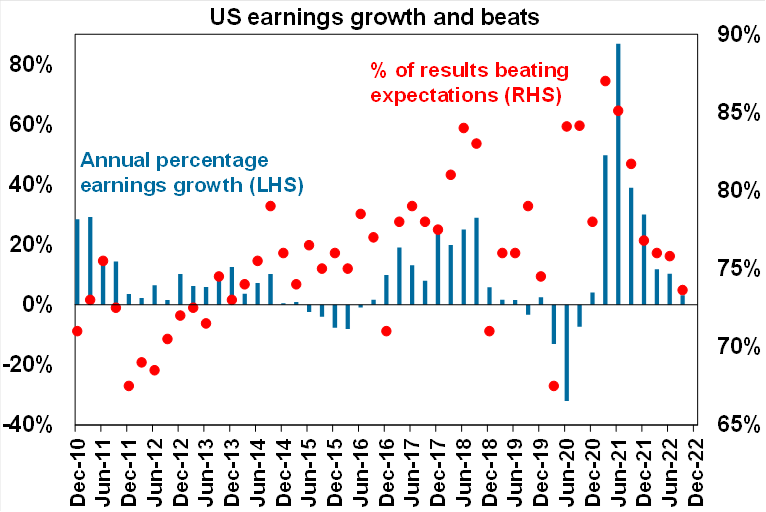

18% of US S&P 500 companies have now reported September quarter earnings with so far 74% ahead of expectations. Earnings growth expectations for the quarter have risen to 3.2%yoy but are likely to come in around 5%yoy. Excluding financials, results are expected by the consensus to be much stronger at 6.7%yoy. Outlook comments have been mixed reflecting the uncertainty regarding the growth outlook. Earnings growth outside the US is running stronger again than in the US.

Source: Bloomberg, AMP

More higher than expected inflation data for September in Canada, the UK and NZ. Canadian inflation rose slightly to 6.9%yoy, with core at 5.3%yoy. UK inflation rose back to 10.1%yoy, with core at 6.5%yoy. And in New Zealand inflation came in well above expectations at 7.2%yoy with trimmed mean inflation at 6.4%yoy. The good news is that inflation is showing signs of peaking, but its still too high so these countries’ central banks are probably all going to raise rates by another 0.75% at their next meetings, albeit with a slowing pace of tightening likely thereafter.

German producer price inflation remained at 45.8%yoy in September which will maintain pressure on the ECB.

Japanese CPI inflation for September held at 3%yoy, but core (ex food and energy) inflation was just 0.9%yoy suggesting that once food and energy prices stabilise inflation will still be well short of the BoJ’s 2% target.

Australian economic events and implications

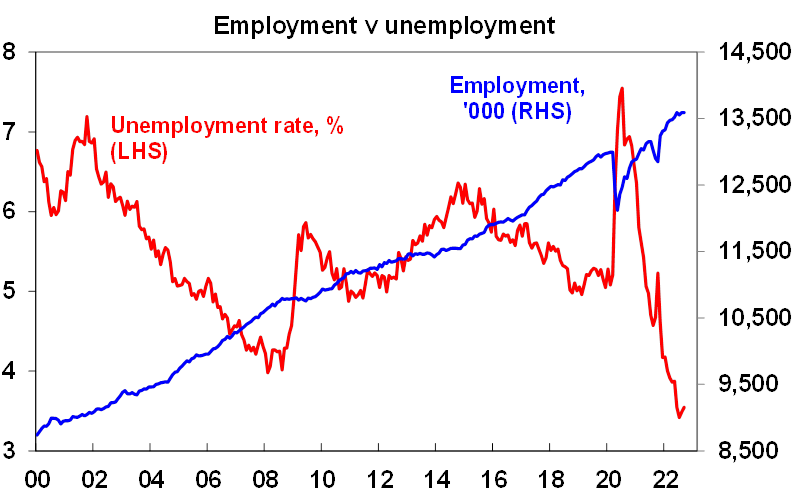

The jobs market remains tight but looks to be starting to cool. Employment was virtually flat in September as were hours worked and both unemployment and underemployment were unchanged at 3.5% (around its lowest in more than 48 years albeit up from 3.41% to 3.54%) and 6% respectively. While the labour market remains very tight it appears to be softening at the edges. Three month average jobs growth has slowed to just 200 jobs a month down from 54,000 jobs a month six months ago and monthly job opening data also appears to be slowing. Unemployment may still fall a bit further, but through next year its likely to be rise above 4% as the reopening surge in jobs is behind us, rate hikes will hit demand and foreign workers and immigrants are returning rapidly which will add to labour supply. With the jobs market still tight and likely to feed through to faster wages growth the RBA is likely to hike rates again next month, but the signs of softening are likely to see it stick to a 0.25% hike rather than revert to 0.5%.

Source: ABS, AMP

What to watch over the next week?

In the US, September quarter GDP (Thursday) is expected to rise 2.3% at an annual rate ending a technical recession over the March and June quarters. In other data, October business conditions PMIs (Monday) are expected to remain softish, home prices and consumer confidence are expected to fall (Tuesday) as are home sales data (Wednesday and Friday) but durable goods orders (Thursday) are expected to show a modest rise. September core private final consumption deflator inflation is expected to rise to 5.2%yoy (from 4.9%) but September quarter growth in employment costs is expected to slow slightly (with both due Friday). The September quarter earnings reporting season will continue.

The Bank of Canada (Wednesday) is expected to hike rates by another 0.75% taking its official rate to 4%.

The ECB (Thursday) is expected to raise its key policy rates by another 0.75% taking its main refinance rate to 2% and flag more rate hikes ahead given high inflation (10%yoy in September). Eurozone business condition PMIs for October (Monday) and economic confidence (Friday) are expected to soften further.

The Bank of Japan (Friday) is expected to leave unchanged is ultra easy monetary policy, although there is some chance it may adjust its 10-year bond yield control to help support the Yen. Japanese business conditions PMIs for October (Monday) and jobs data (Friday) will also be released.

Delayed Chinese data may finally be released. Chinese GDP for the September quarter is expected to show a 2.8%qoq rebound after a 2.6qoq contraction in the June quarter taking annual growth up to 3.3%yoy (from just 0.4% in the June quarter) reflecting the relaxation of covid restrictions around midyear. September activity data is likely to remain soft though with industrial production up 4.8%yoy and retail sales up 3.0%yoy. Import and export growth are expected to slow further.

In Australia, the focus will be on the Government’s Budget (Tuesday) which is likely to be mainly about the implementation of election promises.

Key measures are likely to include: expanding the childcare subsidy; extending paid parental leave to six months; more for Medicare, aged care and the NDIS; cheaper prescription drugs; spending on renewable energy; increased defence spending; increased spending on TAFE and universities; and the implementation of some of its housing schemes.

The Budget will likely also make much of infrastructure spending but we are unlikely to see much in the way of additional infrastructure spending than what has already been budgeted for.

There may be some minimal & targeted cost-of-living measures and maybe something more on trying to keep energy costs down and subsidies for electric cars.

Increased spending is likely to be offset by a cut in public sector spending, a cut in “waste and rorts”, cuts to regional infrastructure funds, a crackdown on tax avoidance, increased tax on multinationals and a possible cap on superannuation balances around $5m.

The Government has deferred any decision on the Stage 3 tax cuts due in 2024.

Of interest will be whether the Government goes ahead with its $52bn in off budget funds (including the $10bn Housing Australia Fund) as it adds to public borrowing and upwards pressure on interest rates.

A revenue windfall – due to higher commodity prices, lower unemployment and higher inflation - will likely allow lower budget deficits in the next year than projected in March but the projections are unlikely to show a surplus due to spending pressures (on aged, NDIS, health, defence and interest) and lower real growth assumptions.

The Budget is likely to put the 2022-23 deficit at around $40bn, above the $32bn seen last year but below the $78bn projected in March. Subsequent years are likely to see only a modest reduction in the deficit from that projected back in March reflecting structural spending pressures and an assumption that commodity prices fall to more modest levels.

On the data front in Australia, September quarter CPI inflation (Wednesday) is expected to come in at 1.7%qoq, taking annual inflation to 7.1%yoy (from 6.1%yoy). Petrol prices are expected to fall but food, rents, insurance, new dwellings & holiday travel are likely to see strong increases. Electricity prices are a source of uncertainty as regulated prices rose sharply but this may be offset by WA and Queensland subsidies. Trimmed mean inflation is likely to be 1.5%qoq with the annual rate rising to 5.5%yoy. Both CPI and trimmed mean inflation are expected to rise to their highest since 1990. As this is broadly expected to be in line with RBA forecasts its likely to be consistent with another 0.25% rate hike in November. Producer price inflation for the September quarter will also be released on Friday. October business conditions PMI’s (Monday) will be watched for any slowing.

Outlook for investment markets

Shares remain at high risk of further falls in the short term as central banks continue to tighten, uncertainty about recession remains high and geopolitical risks continue. However, we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary brakes.

With bond yields likely at or close to peaking for now, short-term bond returns should improve.

Unlisted commercial property may see some weakness in retail & office returns & the lagged impact of higher bond yields is likely to drag down unlisted property and infrastructure returns.

Australian home prices are expected to fall 15 to 20% top to bottom into the September quarter next year as poor affordability & rising mortgage rates impact. This assumes the cash rate tops out around 3% but if it rises to 4% or more as the money market is assuming then home prices will likely fall 30%.

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

The $A remains at risk of further falls in the short term as global uncertainties persist and as the RBA remains a bit less hawkish than the Fed. However, a rising trend in the $A is likely over the medium term as commodity prices ultimately remain in a super cycle bull market.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.