Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, the coronavirus, economic activity trackers, major global economic events and Australia economic events.Investment markets & key developments

Shares had another volatile week, falling initially on interest rate and recession fears with a sharp intraday fall in US shares on Thursday after another worse than expected inflation reading, then having yet another (technical) bounce before falling again in the US on Friday not helped by bank earnings reports and higher inflation expectations. This left US shares down 1.6% for the week, Eurozone shares up 0.1%, Japanese shares down 0.1% and Chinese shares up 1%. The US bounce on Thursday also helped push the Australian share market up to end the week down just 0.1% with strong gains in financials offset by sharp falls in IT, utilities and health shares. Bond yields rose. Oil and iron ore prices fell but metal prices rose slightly. The $A fell below $US0.62 as the $US rose.

After another volatile week the near-term downside risks for shares remain reflecting the array of macro risks – ultra hawkish global central banks, high and still rising recession risks, the $US still trending up on global safe haven demand risking a financial accident, ongoing policy mayhem in the UK, an escalation in the conflict in Ukraine and continuing downwards revisions to earnings expectations. And despite lots of bounces share markets remain stuck around or just below their June lows – a decisive break of which could open up another 5-7% leg down. In particular, in the last week:

- The message from central bankers remains hawkish – with the minutes from the last Fed meeting noting that most Fed saw more risk in tightening too little than in tightening too much, most Fed and ECB officials remaining hawkish, and the Bank of Korea raised rates by another 0.5%.

- US September consumer and producer price inflation surprised on the upside with the CPI up 8.2%yoy and the core CPI up 6.6%yoy. While goods inflation continues to slow, services inflation is continuing to pick up driven particularly by strong gains in shelter (which is mainly rent), medical care and transport services. This will keep the Fed hawkish for now and on track for a 0.75% rate hike next month with the risk it does another 0.75% in December rather than slowing to 0.5%.

Source: Macrobond, AMP

- The UK saw another rough week with bond yields rising further as the BoE ended its bond market supporting QE, PM Truss fired chancellor Kwarteng and reversed corporate tax cuts but did little to inspire confidence with £24bn in unfunded tax cuts remaining. The BoE is forcing Truss to face reality. A key lesson is that when inflation is high markets won’t tolerate fiscal policy that looks inflationary - the “bond vigilantes” are back! Not that they ever really went away. The UK experience probably reduces the risk the new Italian Government will try & do the same.

- The IMF followed the OECD a few weeks ago in downgrading its global growth forecasts and, like everyone, is warning of recession.

Source: Bloomberg, IMF, AMP

However, as we have been pointing out for several weeks now the news is not all bleak:

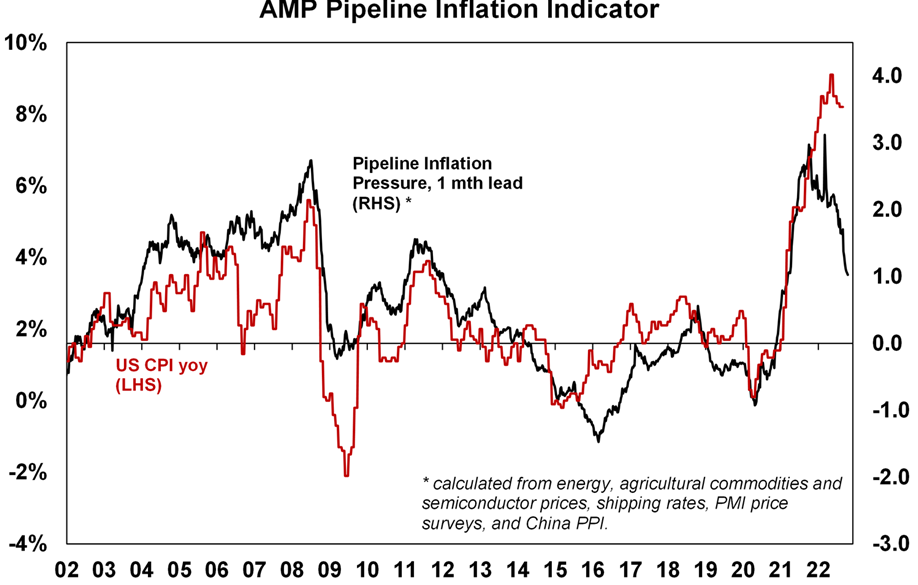

- Our Pipeline Inflation Indicator continues to slow reflecting improving global supply conditions and falling corporate pricing power.

Source: Bloomberg, AMP

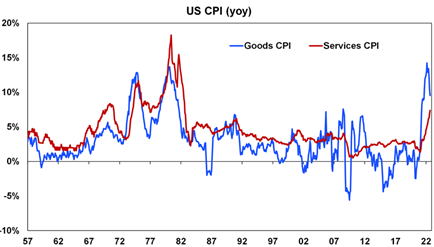

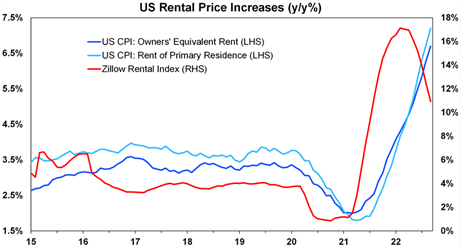

- While US services price inflation is still rising, goods price inflation has rolled over and in the past, it has often led services price inflation at major turning points. See the first chart. Moreover, a big driver of the surge in services inflation has been the surge in rents (as tenants roll on to new higher market rents) but the Zillow rental index indicates that market rents are now slowing after their reopening rebound and with a lag this will feed into the CPI measures of rents and owners’ equivalent rents (which impact a third of the CPI) in the next six months. And there are more and more anecdotes of discounting. Strong wages growth is still a concern for services inflation but there are tentative signs of a cooling in the jobs market. We continue to expect slowing inflation from later this year and particularly through next year as slower demand growth combines with improved supply.

Source: Bloomberg, AMP

- A dovish group appears to be emerging at the Fed who in the minutes are referred to as “several participants”. They appear to want to slow down the pace of hikes to reduce the risk of significant adverse effects. They appear to be led by Vice Chair Lael Brainard who reiterated the need to allow for policy lags, the impact of the rising $US and the combined impact of policy tightening globally. Thanks to the poor September CPI report this group is most unlike to get the upper hand by November’s meeting but it may slow things down thereafter.

- Global and Australian forward PEs have fallen back to around 16 times and 14 times respectively which is closer to longer term averages. Of course, continuing earnings downgrades risk undermining this.

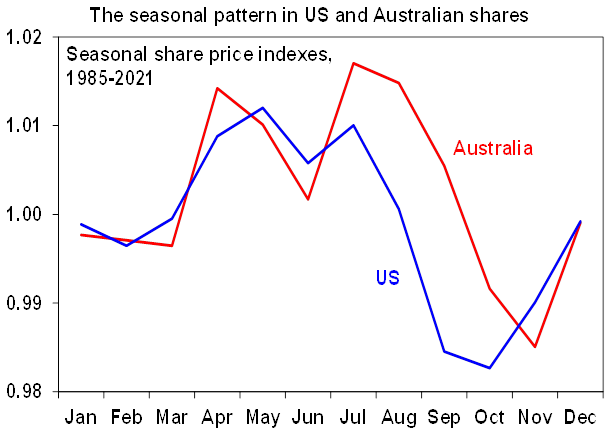

- US shares have consistently rallied after US mid-term election years with year 3 being a strong year on average in the 4 year election cycle after year 2 (ie this year) which is normally a poor year. Share market seasonality also starts to turn more positive in the months ahead.

Source: Bloomberg, AMP

These considerations may not stop further near term downside in shares but hold out the likelihood that global central banks (led by the Fed) will start to slow the pace of rate hikes from later this year. Which should help minimise any recession and then see share markets refocus on recovery.

The Australian Government’s 25th October Budget is likely to see a focus on implementing election promises. Key measures are likely to be include expanding the childcare subsidy, extending paid parental leave to six months, more for Medicare and aged care, spending on renewable energy and the implementation of some of its housing schemes. There may also be some cost-of-living measures, but these are likely to be minimal and there may be more on trying to keep energy costs down. This is likely to be offset by a cut in public sector spending, another crackdown on tax avoidance & increased tax on multinationals. The Government has deferred any decision on the Stage 3 tax cuts due in 2024. Of interest will be whether the Government goes ahead with its $52bn in off budget funds (including the $10bn Housing Australia Fund) as it adds to public borrowing and upwards pressure on interest rates. A revenue windfall – partly due to higher inflation will likely allow lower budget deficits than projected in March but the projections are unlikely to show a surplus due to spending pressures (on aged, NDIS, health, defence and interest) and lower real growth assumptions. The 2022-23 deficit is likely to be above the $32bn seen last year but below the $78bn projected in March.

Should the RBA be worried about the falling $A? The short answer is no unless it falls a lot further: Yes, a rising interest rate differential between the US and Australia tends to push the $A down relative to the $US, all other things being equal. But most currencies have been falling against the $US – some like the pound and the Yen more than the $A. So the trade weighted index for the $A (which takes into account other currencies is only just below its long term average which means that the potential boost to inflation from the falling $A is far less than would be implied by just looking at the fall in the $A versus the $US. And in any case the evidence suggests that a 10% fall in the trade weighted $A will only add about 1% to inflation over 3 years which is just 0.3% per annum. So far the fall in the trade weighted index is just 6% which would add just 0.2% per annum to inflation. And 40 years ago we floated the $A so the RBA can have an independent monetary policy. Rising rates to match the Fed just to keep the $A up would defeat the purpose of floating the $A in the first place. The RBA also has to allow that Australia has less of an inflation problem than the US with much lower wages growth, Australian households are far more vulnerable to higher rates than US households (because of more debt and short-term mortgage rates) so there is no reason to raise rates as much as the Fed. Of course this is not to say that the RBA won’t react to the falling $A, particularly if it continues to fall sharply – but doing so could be a big mistake, needlessly boosting the risk of recession here.

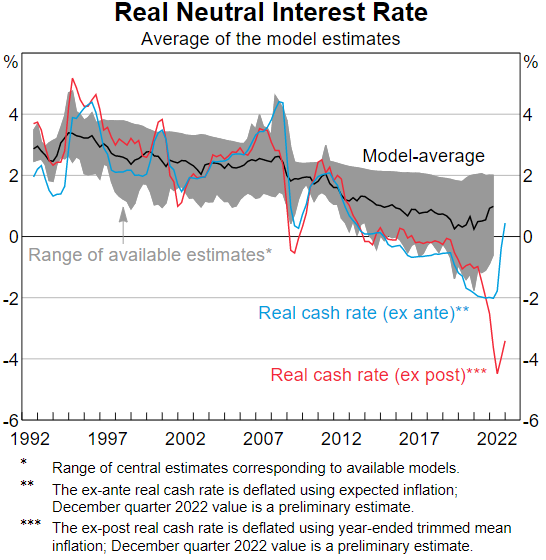

Is the RBA still well below “neutral” on interest rates? RBA Assistant Governor Luci Ellis presented estimates showing the neutral real rate on average is just below 1% in real terms which would be around 3.5% in nominal terms assuming target inflation with the implication being that the cash rate at 2.6% is still well below neutral. But the neutral rate concept needs to be treated with care: the cash rate was way below most estimates of neutral in much of last decade (see chart) and yet growth stayed soft and inflation kept falling resulting in even lower interest rates; the RBA’s various estimates for it range from -0.5% to 2% which is a huge range; and its not observable so we won’t really know where it is until we go past it. As such Assistant Gov Ellis is right to describe it as a “pole star casting a faint light” not a “prescription for what [monetary policy] should do”. Which leaves the RBA data dependent. While it was highly likely the cash rate was well below neutral when it was at 0.1%, its far less clear now and we think its likely tipped into slightly tight.

Source: RBA

Are Australian electricity prices really going to jump another 35% on top of increases of up to 18% recently – or we just being buttered up? This could add another 0.7% or so to inflation next year and is based on current wholesale prices and the capital costs of transitioning from dirty to renewable energy supply. I suspect it may not be that bad – the transition will come with a big cost but if the world goes into recession next year, gas and coal prices may start falling back towards earth from being 6 to 13 times above where they were at the start of 2020. Of course, much of this could have been avoided if we had stuck with carbon pricing. Well done to SA for moving ahead of the crowd when it cost a lot less!

NSW stamp duty reform on the way, but its disappointingly narrow and looks like yet another flawed demand side “solution” to housing problems. Replacing stamp duty with land tax makes fundamental sense – stamp duty is a huge up-front impost that distorts decisions to buy and sell property. But NSW’s first step down this path is so small it may cause more problems than its worth. It only applies to first home buyers on properties worth less than $1.5million. As such it brings forward first home buyer demand without boosting sales by downsizers and so runs the risk of simply boosting demand, resulting in higher than otherwise prices in the sub $1.5million part of the market. And it could lock in FHBs into their first property for longer because once they trade up they will no longer be FHBs and face a big stamp duty impost. Of course, FHBs will also need to allow for their long term land tax bill and banks will likely allow for this in determining how much they will lend. So FHBs may find it easier to save the upfront costs of getting into a property but banks may then lend them less to allow for their need to pay land tax. The barrier to more fundamental stamp duty reform is that stamp duty accounts for 20% of NSW government revenue so swapping stamp duty for land tax entails a short-term revenue loss.

Coronavirus update

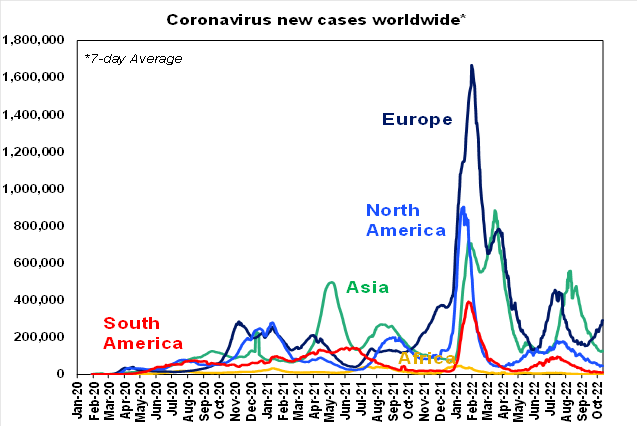

New global & Australian covid cases & deaths are trending down. However, new cases are up in Europe & China.

Source: covidlive.com.au, AMP

Economic activity trackers

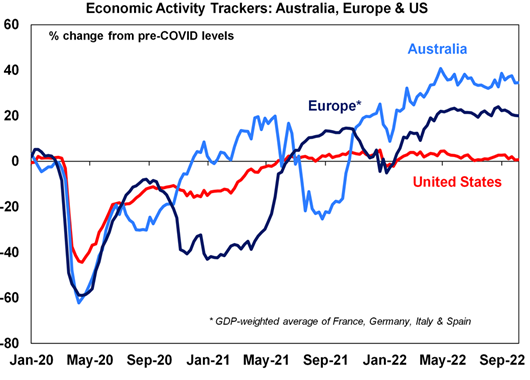

Our Australian, US and European Economic Activity Trackers were little changed in the last week.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

US retail sales were flat in September & consumption looks to have been soft last quarter. Consumer & small business confidence edged higher, but both are weak. Year ahead consumer inflation expectations rose to 5.1% and 5-10 year inflation expectations rose but only to 2.9%. The good news is that, as in surveys of bigger businesses, small businesses are reporting an easing in wages and price growth.

UK unemployment fell to 3.5%, its lowest since early 1974 with average weekly earnings up 6%yoy, highlighting the tight economy and pressure on the BoE to cool inflation which hasn’t been made easier by big fiscal stimulus.

Chinese inflation data remained soft in September with headline CPI inflation rising to 2.8% but core CPI inflation falling to 0.6% and producer price inflation slowing to 0.9%. Credit growth came in stronger than expected in September rising to 10.6%yoy, suggesting policy stimulus may be starting to impact.

Australian economic events and implications

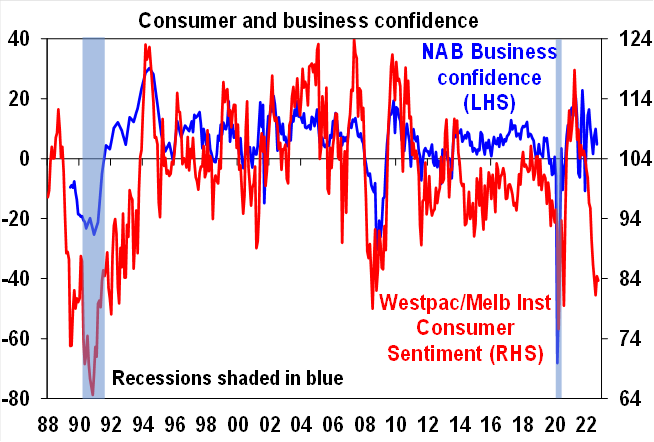

Sad consumers, happier businesses. The latest consumer and business surveys from Westpac/Melbourne Institute and the NAB showed the same mix of depressed consumer confidence but strong business conditions and softish but still reasonable business confidence. Part of this reflects the fact that the weakness in consumer confidence has been yet to show up in actual spending (as consumers have been drawing down saving built up through the pandemic, spending in some areas has still been recovering from the pandemic, the full impact of rate hikes has yet to be seen in actual mortgage payments and the jobs market has been strong). But given the hits to household free cash flow its likely that spending will slow ahead and this will weigh on business conditions. While there is some sign that the shift to a more modest rate hike helped confidence with post RBA rate announcement survey responses being stronger it was still weak and its hard to see it having much of a bounce given all the talk of recession and 35% energy price rises next year.

Source: Westpac/MI, NAB, AMP

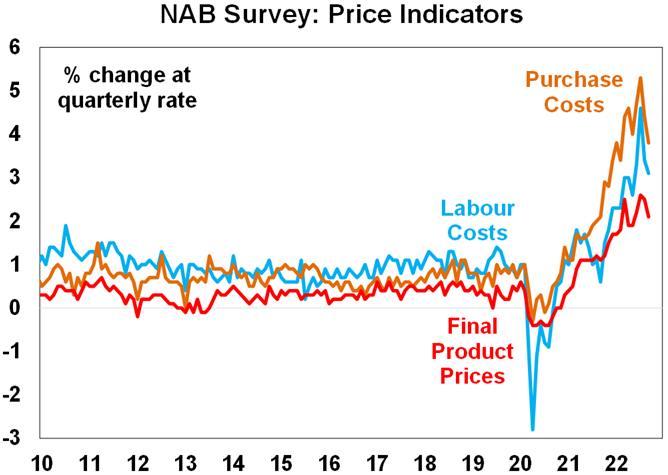

A notable aspect of the NAB survey was a further easing in the growth of labour costs, purchase costs and final prices. They all remain high but they are consistent with an easing in inflation pressures. The rapid rebound in permanent and long-term arrivals to Australia evident in monthly data particularly driven by students suggests some easing of Australia’s labour shortages ahead.

Source: NAB, AMP

Meanwhile. new home sales continue to fall (down another 4.2% in September based on HIA data) reflecting the ongoing impact of higher interest rates.

What to watch over the next week?

In the US, data for industrial production and home builder conditions (Tuesday), housing starts (Wednesday) and existing home sales (Thursday) are all expected to fall and manufacturing conditions in the New York and Philadelphia regions for October are likely to have remained weak. The September quarter earnings reporting season will start to ramp up. Consensus expectations are for earnings to have risen just 2.6% over the year to the September quarter, but with earnings revised down by more than normal over the last few months and nominal economic growth remaining strong there is probably upside to this to around 5%. Energy and industrials are likely to be the strongest.

UK inflation for September is expected to stay at 9.9%yoy and Canadian inflation is expected to fall to 6.6%yoy (both Wednesday). New Zealand’s September quarter inflation rate (Tuesday) is also expected to drop back to 6.6%yoy. All are expected to see ongoing high underlying inflation.

Japanese September inflation data (Friday) is expected to have increased further but with core inflation remaining below 2%.

Chinese GDP for the September quarter (Monday) is expected to show a 3.5%qoq rebound after a 2.6qoq contraction in the June quarter taking annual growth up to 3.4%yoy (from just 0.4% in the June quarter) reflecting the relaxation of covid restrictions from around midyear. September activity data is likely to remain soft though with industrial production up 3.7%yoy and retail sales up 3.1%yoy.

Australian jobs data for September (Thursday) is expected to show a moderation in employment growth to +20,000 but with unemployment remaining low at 3.5%.

Outlook for investment markets

Shares remain at high risk of further falls in the short term as central banks continue to tighten, uncertainty about recession remains high and geopolitical risks continue. However, we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary brakes.

With bond yields likely at or close to peaking for now, short-term bond returns should improve.

Unlisted commercial property may see some weakness in retail & office returns & the lagged impact of higher bond yields is likely to drag down unlisted property and infrastructure returns.

Australian home prices are expected to fall 15 to 20% top to bottom into the September quarter next year as poor affordability & rising mortgage rates impact. This assumes the cash rate tops out around 3% but if it rises to 4% or more as the money market is assuming then home prices will likely fall 30%.

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

The $A remains at risk of further falls in the short term as global uncertainties persist and as the RBA remains a bit less hawkish than the Fed. However, a rising trend in the $A is likely over the medium term as commodity prices ultimately remain in a super cycle bull market.

Eurozone shares rose 0.7% on Friday, but the US S&P 500 fell 2.4% reversing most of Thursday’s bounce with soft bank earnings reports and higher US consumer inflationary expectations. The poor US lead saw ASX 200 futures fall 102 points, or 1.5%, pointing to a weak start to trade for the Australian share market on Monday.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.