Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses Australian retail spending.Australian retail spending rose solidly again in August, rising by 0.6%mom after a 1.3%mom gain in July and beating market expectations for a 0.4% lift.

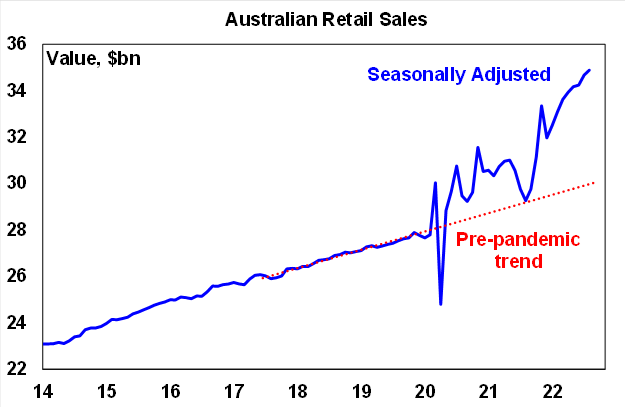

They are now up 19% on lockdown depressed year ago levels and are 16% above their pre-covid trend.

Spending was strongest in department stores (+2.8%) and household goods retailing (+2.6%), which may seem perverse given that spending in both areas is discretionary and hence most vulnerable to higher rates and cost of living pressures. That said the rise in spending on household goods followed two months of falls, and spending on clothing (-2.3%) and “other retailing” (-2.5%) fell.

Source: ABS, AMP

The continuing strength in retail sales so far likely reflects a combination of accumulated savings built up through the pandemic which has provided a buffer for households, positive wealth effects from the rise in home prices into early this year, the still strong jobs market and lags in the flow through of RBA rate hikes into home borrowers’ debt interest payments.

However, while retail sales have remained stronger for longer than we have been expecting, we continue to expect a slowdown ahead as rate hikes are fully reflected in mortgage payments, rates continue to rise, negative wealth effects from now falling home prices start to impact, consumer confidence remains depressed and the run down in the saving rate runs its course. Retail sales being well above their pre-covid trend leaves them particularly vulnerable on a longer-term basis as the rotation back to services continues.

That said, the upside surprise in retail sales on the back of still strong jobs data and ongoing high and still rising inflation adds to the risk that the RBA will hike by another 0.5% next week, whereas we continue to think they should be slowing the pace of hikes to better allow time to assess the impact of past hikes and allow for their lagged impact.

Meanwhile, the Federal Government has confirmed that the final 2021-22 budget deficit was $32bn (1.4% of GDP), down from $80bn projected in March and $99bn in December.

The improvement had long been evident in monthly budget data and reflects a combination of soaring corporate tax (with high commodity prices) and personal tax (with the strong jobs market), lower welfare payments and delays in some spending. Normally this would flow through to sharply lower deficit projections for subsequent years but the flow through this time will likely be limited as: the Government will continue to assume that commodity prices will fall back at some point; unemployment will rise as the economy slows; some of the delayed 2021-22 spending will be pushed into this year; structural pressures from health, aged care, the NDIS, defence and debt interest costs will boost spending in future years; and a likely lower long term productivity growth assumption will lead to lower long term revenue assumptions. So the October Budget is likely to project ongoing deficits in the years ahead, albeit they may be a bit lower than projected in March. The lower deficit last year will likely delay the time when Federal public debt rises above $1trn from 2023-24 into 2024-25.

Ends

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.