By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

Key points

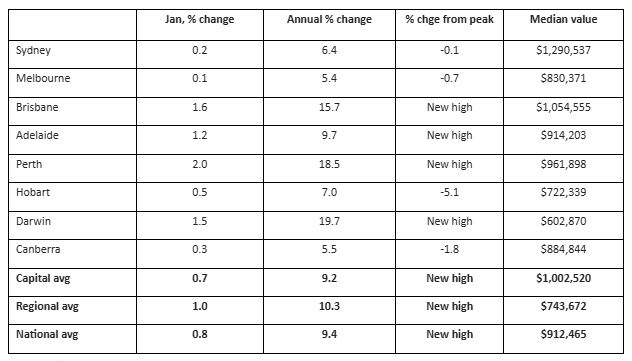

- National average home prices rose 0.8%mom in January, but with Sydney and Melbourne seeing only very weak growth and Brisbane, Adelaide and Perth continuing to see strong growth, but with some slowing from late last year. Average monthly gains remain robust but have slowed since October as buyers have become more cautious on the back of rate hike talk.

- Low vacancy rates contributed to a rise in rents of 0.6%mom in January, pushing annual rental growth up to 5.4%yoy.

- The lagged impact of last year’s rate cuts, the expansion of the 5% low deposit scheme and the startup of the Help to Buy Government equity scheme along with the ongoing housing shortage are expected to drive further gains in home prices this year.

- But gains are likely to slow reflecting the less favourable interest rate outlook, poor affordability and possibly further macro-prudential tightening by APRA.

- After 8.6% growth in 2025 we expect property price growth to slow to around 5-7% in 2026. If rates rise significantly, home prices could fall.

Home price growth up in January, but down from last year’s high

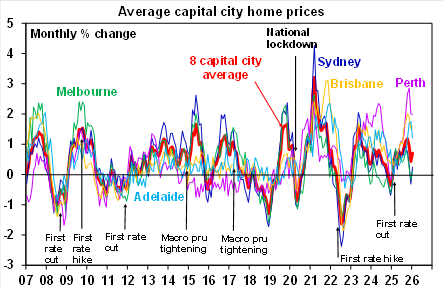

Cotality data shows that national average home prices rose 0.8%mom in January with all capital cities seeing growth. This was up on December which saw a 0.6%mom rise as Sydney and Melbourne prices rose after falls in December which partly reflected seasonal weakness. But both cities only saw weak gains.

Australian dwelling price growth

Source: Cotality

The broad picture remains one of a slowing in price gains since October as talk of rate hikes has gradually replaced expectations for rate cuts at the same time that affordability is increasingly biting after another surge in prices to record highs. Even the boom time cities of Brisbane, Adelaide and Perth have seen some loss of momentum since late last year.

Source: Cotality, AMP

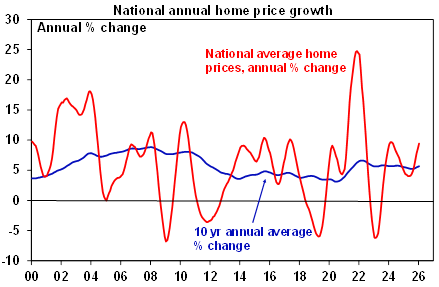

Annual home price growth continued to accelerate though to 9.4%yoy as softer monthly growth a year ago dropped out of the annual calculation. The pick-up in home price growth over the last year got underway when the RBA started to cut interest rates in February and was helped along by the expanded first home buyer 5% deposit scheme which was announced prior to the Federal election and commenced in October, improved consumer confidence and the ongoing shortage of housing. It was also helped by below average levels of listings as vendors held back for higher prices and as lower interest rates relieved the pressure to sell for some distressed mortgage holders. These considerations more than offset the impact of poor affordability.

Source: Cotality, AMP

The housing shortage remains…

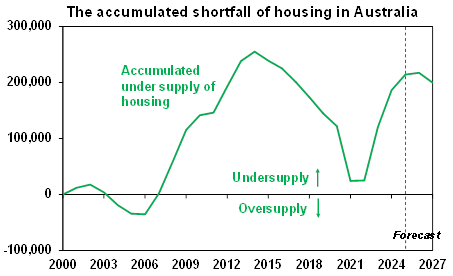

With slowing population growth and slightly improved housing completions the property market is now in better balance on annual basis. But there remains an accumulated housing shortfall – of around 200,000 to 300,000 dwellings – that has built up after several years of very strong population growth. Related to this, listings remain below longer-term average levels. The shortage of homes relative to underlying population driven demand remains the key driver of upwards pressure on property prices in Australia and poor affordability

Source: ABS, AMP

…but we expect home price growth to slow this year, with a high risk of falls on rate hikes

The combination of the lagged effect of last year’s rate cuts, the expanded first home buyer 5% deposit scheme and the Help to Buy scheme with 10,000 places a year and the ongoing shortage of housing are likely to keep the upswing in property prices going this year. However, the pace of gains is likely to slow further from that seen in 2025 as the interest rate outlook has turned far less favourable with the RBA possibly going to raise rates as early as this week, APRA starting to ramp up controls to slow risky or speculative lending and affordability now being worse than ever.

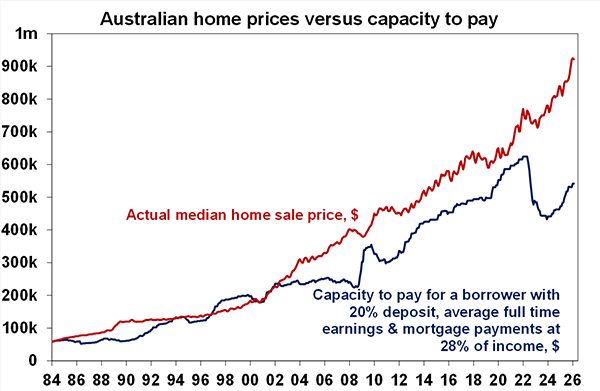

· The RBA’s decision on rates this week is close call with annual inflation rates running above target and above expectations pointing to a hike, but a downtrend in underlying inflation since the September quarter leaving open the possibility that rates may hold ahead of more information. Whether rates go up this week or not, ongoing talk of rate hikes will continue to act as a dampener on buyer demand. If rates have bottomed as now looks very likely it will mean the cycle low in mortgage rates will have been well above their record lows seen in 2021 of around 2 to 3%. As such, the buying capacity of home buyers will remain well below the levels seen in 2021-22, at a time when home prices are 15-20% above their 2021-22 high. This will limit the upside in property prices.

Source: Cotality, ABS, AMP

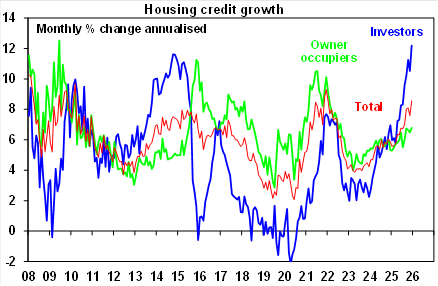

· APRA is starting to ramp up macro prudential regulatory controls to cool riskier forms of property lending and further moves are possible. The initial move late last year won’t have much impact, but it’s clearly a pre-emptive move designed to cool investor activity before it gets too hot. If it doesn’t work – and some borrowers may try to get in ahead of the cap becoming binding, so it could actually boost investor lending in the near term – APRA is likely to do more like putting a cap on investor credit growth like the 10%yoy cap it applied in late 2014. Investor lending is already running at a pace above that seen in 2014 and in excess of a 10% annualised pace.

Source: RBA, AMP

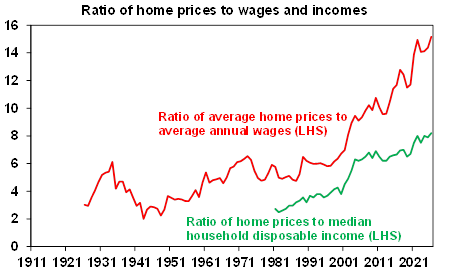

· Housing affordability has deteriorated further from already very poor levels. This is evident in the ratio of home prices to wages and incomes being at record levels. This could limit the upside in property prices. Its already evident lower priced homes seeing stronger growth than upper priced homes as poor affordability pushes buyers towards lower price points. This could also start to favour units over houses.

Source: Cotality, ABS, AMP

· Finally, slower population growth, reflecting a crackdown on student visas, may also take some pressure off the home buyer market. Population growth has already slowed from a peak of 662,000 over the year to the September quarter 2023 to 420,000 over the year to the June quarter with the Government’s immigration forecasts implying a fall to around 365,000 in 2025-26.

Overall, Australian home price growth this year is likely to be constrained by the less favourable interest rate outlook, the potential for more APRA moves to slow investor lending and poor affordability. After 8.6% growth in 2025 we anticipate a slowing in national average home prices growth to around 5-7%yoy this year. If rates rise much home prices could fall.

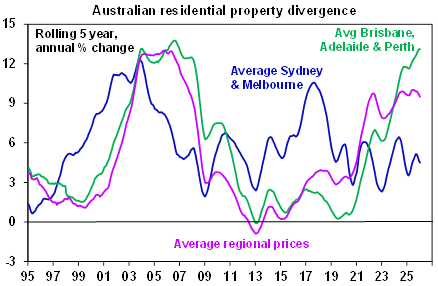

With FOMO running hot in the boom time cities of Brisbane, Perth and Adelaide they are likely to remain the strongest of the state capitals in the near term. But as their relative affordability continues to deteriorate with average prices around or above those in Melbourne and price to income ratios being well above that in Melbourne they are at risk of a sharp slowdown in the second half of the year. Particularly in Adelaide and Brisbane.

Source: Cotality, AMP

What to watch?

The key things to watch will be interest rates, unemployment and population growth. A return to rate hikes, a sharply rising trend in unemployment and a sharp slowing in net migration could result in a resumption of property price falls. On the flipside a resumption of rate cuts and faster than expected population growth could drive a stronger rise in property prices.