Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, the coronavirus, economic activity trackers, major global economic events and Australia economic events.Investment markets and key developments over the past week

Share markets mostly fell over the last week on fears that still rising inflation will trigger faster rate hikes and recession. While Japanese shares rose, US, European and Chinese shares fell. The fall in Eurozone shares was magnified by the risk of a permanent shutdown of Russian gas flowing through the Nordstream 1 pipeline to Germany following a maintenance shutdown and another political crisis in Italy with the Five Start Movement withdrawing support for the Draghi Government. Australian shares reversed much of their gains of the previous week led by sharp falls in miners on plunging commodity prices, with utility, financial and property shares also down sharply. Bond yields generally fell on recession fears as did oil, metal and iron ore prices. The growth sensitive $A also fell as the $US continued to rise.

Inflation and interest rate hikes, and the fear it will drive recession continued to dominate investment markets over the last week.

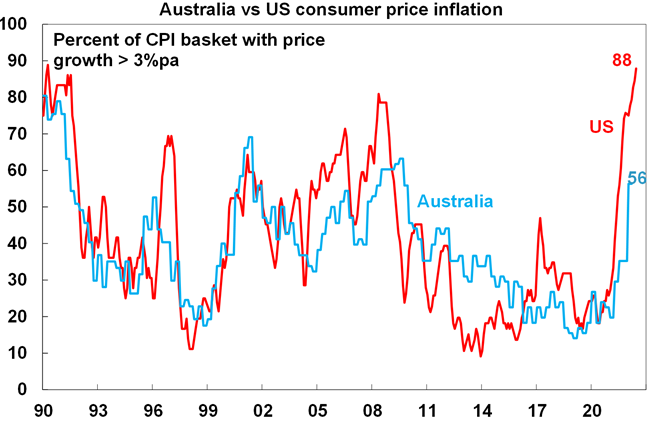

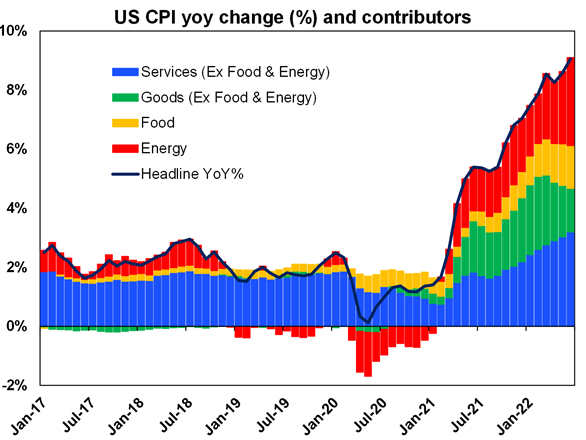

US June CPI inflation came in far stronger than expected at 9.1%yoy with core (ie ex food and energy) inflation at 5.9%yoy. Annual core inflation fell again but its still way too high and rapid price rises are now widespread with 88% of CPI items seeing price gains greater than 3%yoy (see the first chart below) and median inflation now running around 6%. Headline inflation is likely to slow in July helped by a sharp fall in gasoline prices and falling upstream price pressures point to slowing inflation later this year. But given the breadth of sharp price rises in July for now the Fed will remain aggressive seeking to slow demand and cool the labour market which is likely contributing the ongoing acceleration in services inflation (see the second chart below). We expect the Fed to hike again by 0.75% later this month but there is a high risk that it will hike by 1.00%. This increases the risk that the Fed goes too far knocking the US economy into recession.

Source: Bloomberg, AMP

Source: Bloomberg, AMP

The Bank of Canada hiked its cash rate by a greater than expected 1% taking it to 2.5% citing high inflation and the need to keep inflation expectations down. It signalled more hikes ahead, although the pace may slow.

The Reserve Bank of New Zealand raised its cash rate by another 0.5% taking it to 2.5%. It also expects more rate hikes ahead despite downside risks to growth.

The Philippines Central Bank hiked by 0.75% and the Bank of Korea hiked by 0.5% all in response to high inflation.

In Australia there has been nothing new from the RBA but continuing strong jobs growth in June pushing unemployment down to 3.5% a year ahead of when it expected it to be reached will keep the RBA on track for more rate hikes. We expect another 0.5% hike in August, but another blowout inflation result (with the June quarter CPI released on 27th July) could push it to a 0.75% hike.

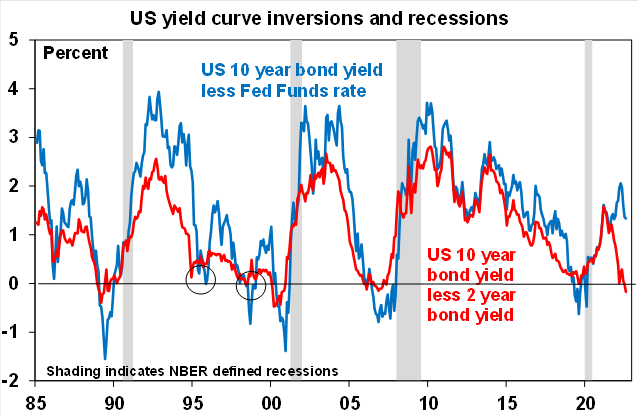

The basic message from central banks is that they are determined to get inflation under control, even if it means the risk of recession. And of course, the ongoing upside surprises on inflation add to the risk that central banks have to go further – with market expectations for Fed and RBA rate hikes rising again over the last week - adding to the risk of recession. This was reflected in a further inversion of the 10 year-2 year US yield curve. And if a recession eventuates shares likely have more downside as earnings start to fall, because the falls in markets so far mainly reflect a valuation adjustment (ie lower PE’s) in response to higher bond yields.

Source: Bloomberg, AMP

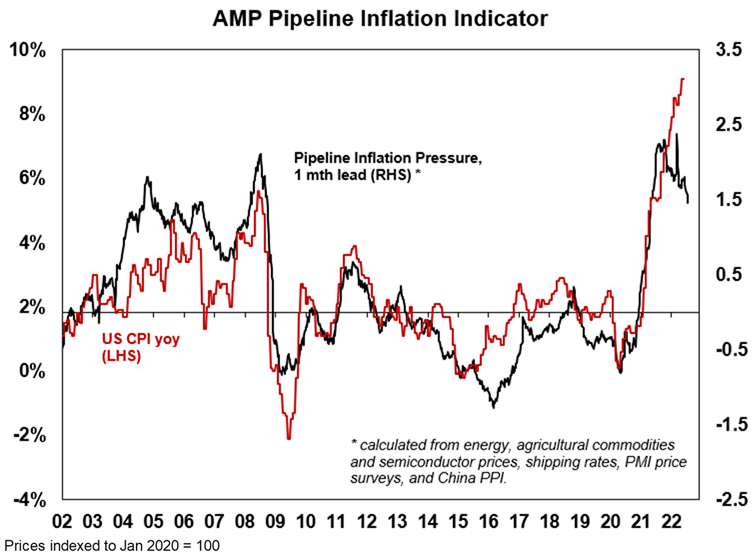

Our view remains that recession or at least a deep recession can be avoided and if so, this should enable shares to rise on a 12-month horizon. Forward looking economic indicators – like PMIs and consumer confidence – are starting to cool and this will take pressure off demand and hence inflation. And our US Pipeline Inflation Indicator is continuing to trend down reflecting a combination of falling work backlogs, freight rates, metal prices, grain prices and even oil prices. This is likely to flow through to cooler monthly inflation readings over the next 6 months in the US and then eventually elsewhere which should start to take pressure off central banks and slow the pace of rate hikes in time to avoid a recession. Of course, there is a long way to go and the risks have increased.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Bloomberg, AMP

The bottom line remains that with central banks still tightening and the risk of recession high and still rising, shares remain at high risk of further falls in the short term. This could well run out to September or October.

Coronavirus update

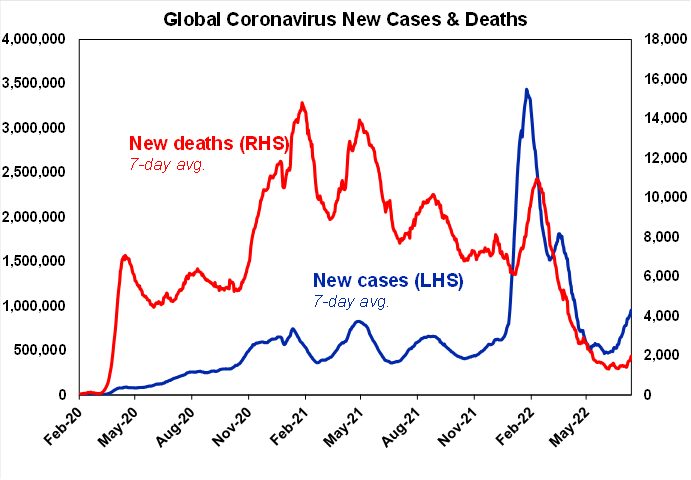

New global Covid cases continue to edge up as the more transmissible Omicron BA4 and BA5 subvariants come to dominate. The rise is being led by Europe, but the US, Asia (notably Japan) and South America are seeing modest increases. Hospitalisations and deaths generally remain subdued in most countries relative to cases compared to pre-Omicron waves and note that cases are now being increasingly under reported.

Source: ourworldindata.org, AMP

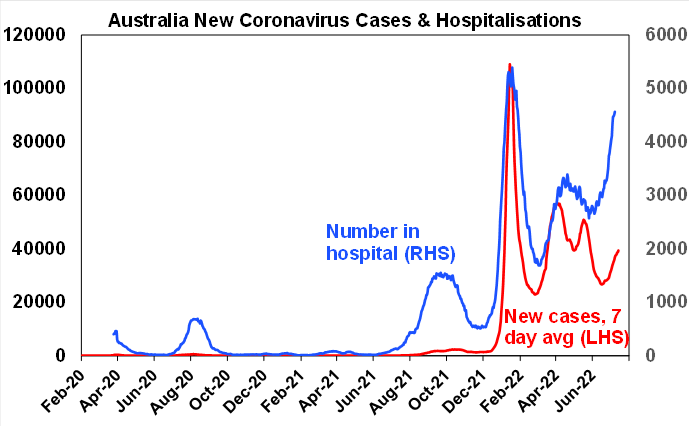

Australia is seeing a sharp rise in hospitalisations – again suggesting that cases are being under reported. With Omicron BA4 and BA5 being far more transmissible than earlier Omicron variants and prior exposure offering little protection soft restrictions such as mask requirements and work from home advice are starting to return and likely to spread further in order to avoid hospitals being overwhelmed. While eligibility for a fourth vaccine has been widened a concern remains that the proportion of the population to have had a third vaccine is only at around 54%. While another significant economic disruption like those seen in 2020 and 2021 is unlikely, increasing work absences due to illness and even less CBD activity may become an issue over the next month.

Source: covidlive.com, AMP

Fortunately, South Africa’s experience with Omicron BA4 and BA5 in April/May augurs well in that it saw a brief spike in new cases but hospitalisations and deaths remaining subdued.

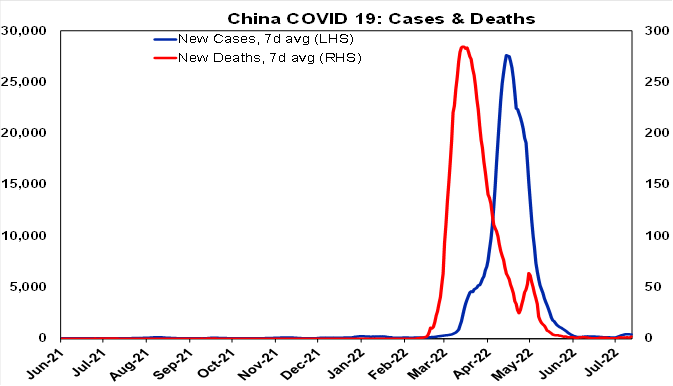

New Covid cases remain low in China, but various breakouts highlight the high risk of a return to lockdowns.

Source: ourworldindata.org, AMP

Economic activity trackers

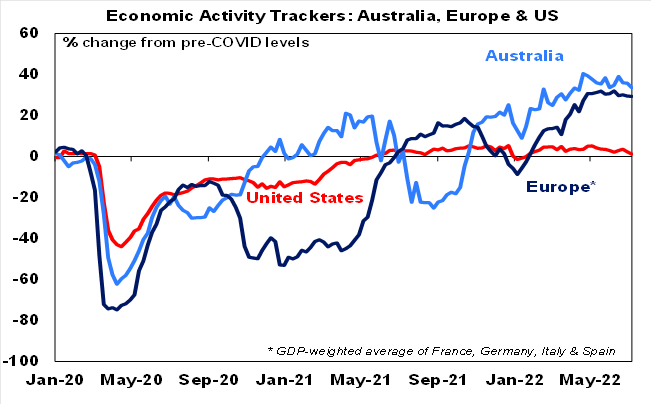

Our Australian Economic Activity Tracker fell again in the last week as did our US Tracker and our European Tracker was flat. All have lost momentum consistent with at least a slowdown in growth.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

US economic data was soft with another fall in small business optimism and a continuing rising trend in unemployment claims. Its early days in the June quarter earnings reporting season with so far only 24 S&P 500 companies having reported, with 62% ahead of expectations.

The latest bout of political turmoil in Italy raises the chance of an early Italian election which would favour more populist parties. While this is unlikely to threaten the Euro, it could weaken European resolve against Russia.

Japanese producer price inflation remained high at 9.2%yoy in June.

China’s economy slumped in the June quarter, but more recent data has continued to recover. June quarter GDP contracted by 2.6%qoq bringing annual growth down to just 0.4%yoy its weakest since March quarter 2020 as the March/April Covid lockdowns impacted. However, industrial production, retail sales, investment and credit growth all continued to recover in June and unemployment fell as the lockdowns eased and policy stimulus measures impacted. Export growth also surprisingly accelerated. This is all consistent with the improvement seen in business conditions PMIs. The main risks going forward relates to the return of Covid restrictions if cases continue to rise and ongoing problems in the Chinese property market with homebuyers now boycotting mortgage payments on stalled projects. Chinese CPI inflation rose to 2.5%yoy but remains low with core inflation at just 1%yoy and producer price inflation continuing to slow.

Australian economic events and implications

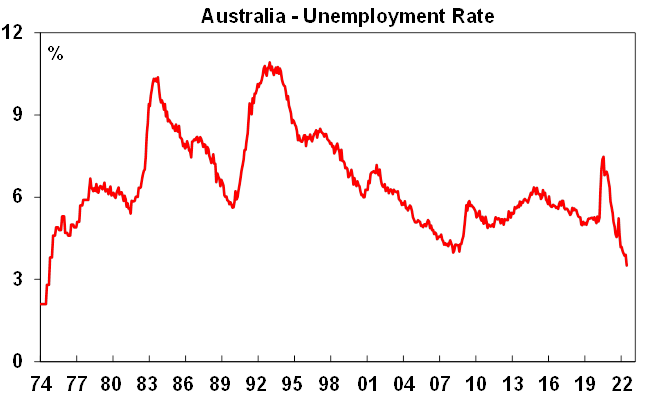

June saw another very strong jobs report in Australia with employment up far more than expected, unemployment falling to 3.5% which is its lowest since 1974, total labour market underutilisation remaining at its lowest since 1982 and labour force participation rising to a record high.

Source: ABS, AMP

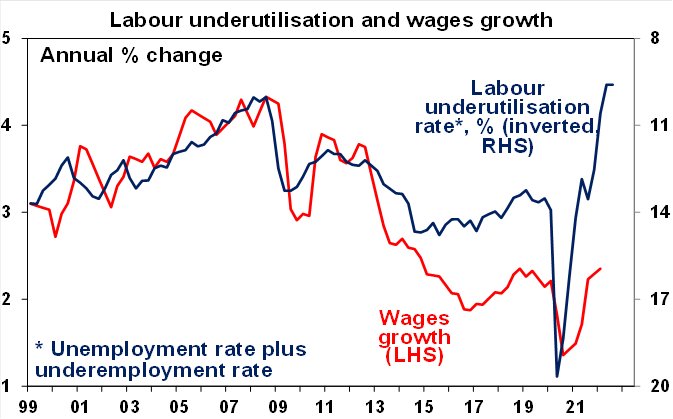

Faster wages growth ahead. Job vacancy data is still strong and so we now see the unemployment rate falling to around 3.2% over the next 3-6 months. This is well below full employment (which is around 4%) and along with the low labour underutilisation rate points to stronger wages growth ahead.

Source: ABS, AMP

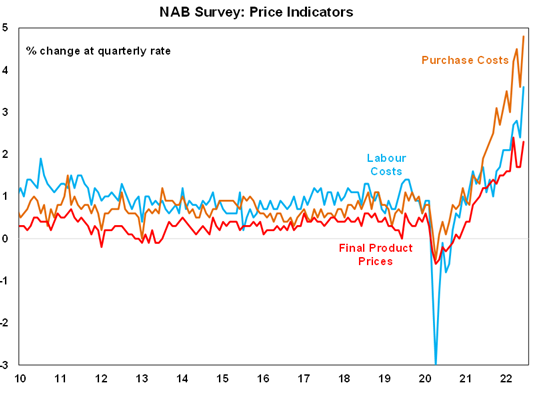

This is consistent with the July NAB businesses survey which showed a further acceleration in labour costs along with high readings for increases in purchase costs and final product prices.

Source: Macrobond, AMP

Given the strong jobs market and the ongoing concern about high and still rising inflation and the need to prevent inflation expectations moving higher we expect another 0.5% RBA rate hike in August. The move by the Bank of Canada to hike by 1% and the possibility of the same by the Fed later this month suggest that the RBA may hike by 0.75%, particularly if the June quarter CPI is another shocker (ie well beyond our expectation for a rise to 6.2%yoy). However, we lean to the view that 0.75% plus hikes will be avoided in Australia given that the RBA meets monthly whereas the Fed and BoC only meet 6 weekly and inflation and wages pressures are a bit less in Australia than they are in the US and Canada. We continue to see the peak in the cash rate being around 2.5% in the first half of next year, but the risks are on the upside and the peak could come earlier given the extent of inflation pressures. Key to watch in the near term will be the June quarter inflation data on 27th July.

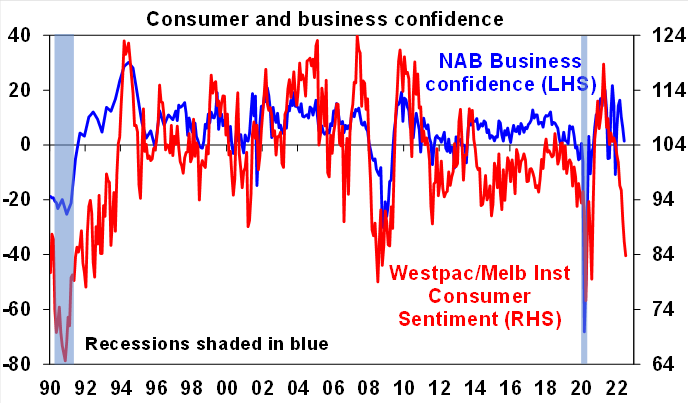

Bear in mind though that the labour market is a lagging economic indicator. Confidence is more of a leading indicator and while its slowing but still around average levels for businesses (as measured by the NAB survey), it’s now very weak and still falling for consumers with consumer confidence down another 3% in July to levels normally associated with recession or very weak growth. This points to weaker economic growth ahead and points to a rising unemployment rate through next year. All of which will ultimately put a lid on how much the RBA will ultimately be able to (and will need to) raise rates by. Which is why we expect the cash rate peak to be around 2.5%.

Source: Westpac/MI, AMP

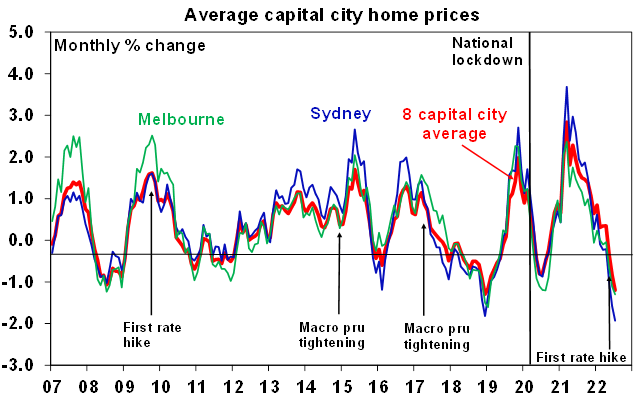

Meanwhile, the plunge in home prices is continuing to accelerate so far in July with Sydney home prices falling at their fastest monthly pace since the mid-1980s. This along with falling real incomes will act as a drag on consumer spending ahead. Hiking the cash rate to the 3.5% or so level expected by the money market risks crashing the property market and hence the economy. So, we remain of the view that rates won’t get that high.

Source: CoreLogic, AMP

What to watch over the next week?

Business conditions PMIs for July for the US, Europe, Japan and Australia will be released on Friday and will likely show further signs of a slowdown. Hopefully, pricing pressures, supplier delivery lags and work backlogs with have continued to improve pointing to a peaking in inflation pressures.

In the US, expect home builder conditions for July (Monday) to remain solid but off their highs, housing starts (Tuesday) to rise slightly, existing home sales to fall slightly and the Philadelphia Fed manufacturing conditions index to improve slightly but remain weak. US June quarter earnings reports will continue with the consensus expecting a 5.5%yoy rise but solid demand conditions in the quarter point to upside surprise of around 4%. Corporate commentary is likely to be cautious though and highlight cost pressures.

The ECB is expected to increase its policy rate by 0.25% on Thursday, joining other central banks in rate hikes. This will take its main refinancing rate to 0.25% and its deposit rate to -0.25%. The ECB’s guidance is likely to foreshadow more rate hikes ahead despite the deterioration in the growth outlook. It is also expected to unveil a mechanism to prevent spread widening between member country bond yields and market reaction may largely depend on hwo robust this is seen to be.

The Bank of Japan is expected to leave monetary policy on hold on Thursday, but there is some risk that it may weaken its bond target given the plunge in the Yen. Japanese inflation for June is expected to fall to 2.4%yoy (from 2.5%) and core inflation is expected to rise to 0.9%yoy (from 0.8%).

In Australia, the minutes from the RBA’s last meeting (Tuesday) and a speech by Governor Lowe on Wednesday are likely to reiterate the RBA’s upbeat view of the economy, concern about high inflation and commitment to do “what is necessary” to return inflation to target with more rate hikes expected.

Outlook for investment markets

Shares remain at high risk of further falls in the months ahead as central banks continue to tighten to combat high inflation, the war in Ukraine continues and fears of recession remain high. However, we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary policy brakes.

With bond yields looking like they may have peaked for now short-term bond returns should improve.

Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-covid levels and office occupancy remains well below pre-covid levels). Unlisted infrastructure is expected to see solid returns.

Australian home prices are expected to fall by 15 to 20% into the second half of next year as poor affordability and rising mortgage rates impact. Sydney and Melbourne prices are already falling aggressively, and most other cities and regions are seeing price gains slow ahead of likely falls.

Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

The $A is likely to remain volatile in the short term as global uncertainties persist. However, a rising trend in the $A is likely over the medium term as commodity prices ultimately remain in a super cycle bull market.

Ends

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.