Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the labour market and the implications for the RBA.Key points:- Employment rose by 4000 in April, with full time up by 92,400 but part-time employment down by 88,400

- Hours worked rose by 1.3% in April and by 2.8% over the last year

- Unemployment is now 3.9%, with March unemployment also revised down to 3.9%

- The participation rate fell slightly to 66.3% from 66.4%

- Underemployment fell to 6.1% from 6.3%

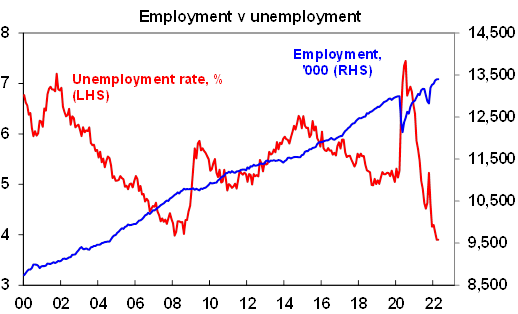

Another strong jobs reportEmployment rose by less than expected and participation fell slightly. But the level of employment in prior months was revised up and the quality of jobs growth was very strong with a surge in full time jobs such that hours worked rose strongly.

Source: ABS, AMP

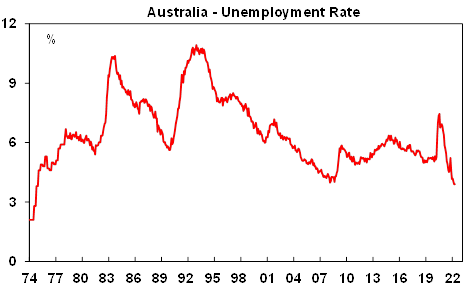

And most importantly unemployment is now at 3.9%, and in fact got there in March after a revision, which is its lowest level since 1974.

Source: ABS, AMP

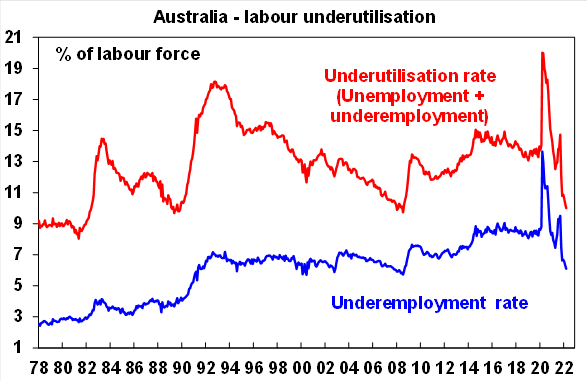

Similarly, underemployment fell to 6.1% taking labour underutilisation down to 10% which is its lowest since 2008.

Source: ABS, AMP

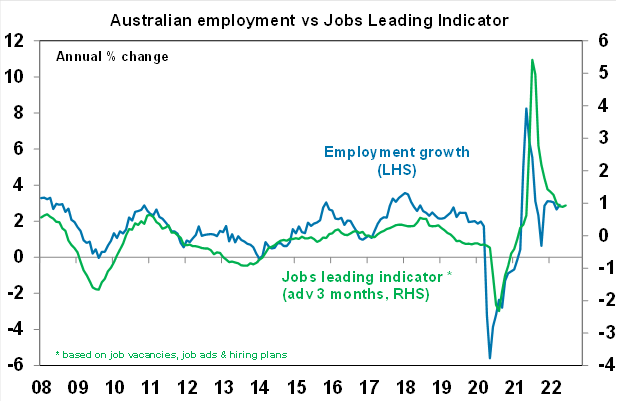

Looking forward our Jobs Leading Indicator which is based on job openings points to continued strong employment growth. As a result, we continue to see unemployment falling to around or below 3.5% by year end.

Source: ABS, NAB, ANZ. AMP

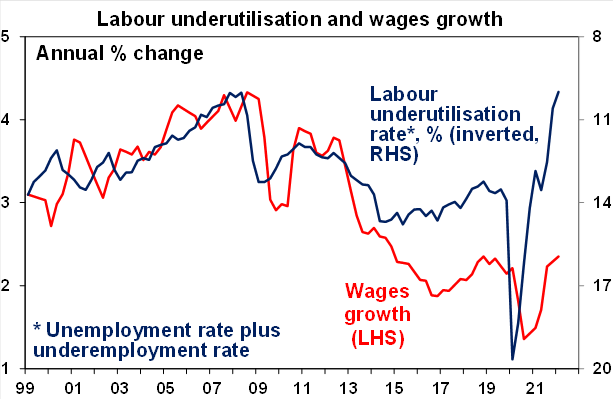

The tight labour market evident in the fall in both unemployment to its lowest since 1974 and labour underutilisation to its lowest since 2008 point to an acceleration in wages growth ahead.

Source: ABS, AMP

Implications for the RBA

The strong April jobs report keeps the RBA on track for raising rates again at its June meeting. While March quarter wages growth was on the soft side it was in line with RBA expectations and the tight labour market along with numerous business surveys and the RBA’s own business liaison point to an acceleration in wages growth ahead. As a result and given RBA concerns that inflation psychology might rise it is likely to step up the pace of tightening in June in order to get on top of inflation and so we expect a 0.4% hiking taking the cash rate to 0.75%. By year end we continue to see the cash rate rising to between 1.5% and 2%.

Of course the one fly in the ointment is the comparison to 1974 after which things were not so flash – hopefully history does not repeat but in any case the lesson from the 1970s is that the RBA needs to act quickly to make sure inflation expectations do not rise significantly because if they do it will be much harder to get inflation back down.

Ends

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.