Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses investment markets and key developments over the week, the coronavirus, economic activity trackers, major global economic events, and Australian economic events.Investment markets and key developments over the past week

Share markets fell again over the last week with ongoing worries about monetary tightening to combat high inflation driving a possible recession. The plunge in global shares also dragged down the Australian share market which saw sharp falls in IT, material, property and industrial shares with only health stocks rising for the week. Global bond yields pulled back from their highs, oil, metal and iron ore prices fell and the risk off tone dragged the $A below $US0.69 as the $US rose.

From their bull market highs US shares are down 18%, Eurozone shares are down 18%, Japanese shares are down 14%, global shares are down 17% & Australian shares are down 8%. While European and Japanese shares initially fell harder after the invasion of Ukraine the concern recently has swung back to higher inflation and higher interest rates which has really weighed on the US share market with its higher tech exposure with Nasdaq now down 29%. The fall back in commodity prices has harmed Australian shares lately but their low exposure to tech stocks is helping them in a relative sense.

Short term risks around inflation, monetary tightening, the war in Ukraine and Chinese growth remain high and still point to more downside in share markets before they bottom. The risks around inflation and rising bond yields are the main threat at present – but Chinese Covid lockdowns and the war in Ukraine are adding to supply disruptions.

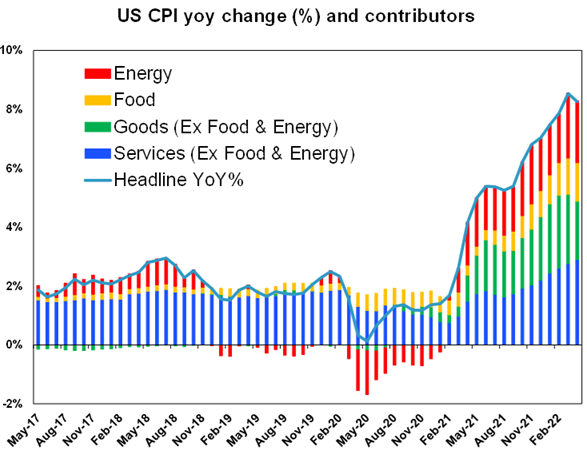

US inflation came in stronger than expected again for April. While annual inflation fell slightly (from 8.5%yoy to 8.3% for the CPI and from 6.5%yoy to 6.2% for core inflation) as higher monthly inflation readings a year ago dropped out it was still higher than expected. Goods inflation (green bars in the next chart) looks to be slowing but services inflation (blue bars) is continuing to pick up – particularly for airfares, health and rents – partly reflecting the surge in wages growth seen recently in the US. So while inflation may have peaked it looks like staying too high for comfort for the Fed (and other central banks) fr a while yet keeping it on track for 0.5% rate hikes at the next three meetings.

Source: Bloomberg, AMP Capital

ECB President Lagarde strongly hinted that the ECB will start raising rates in July. The ECB expects to stop bond buying early in the third quarter with the start of rate hikes “some time” after that.

Rising pressure for wage growth to compensate for higher inflation risks resulting in a wage/price spiral and a rise in inflation expectations that simply locks inflation in at high levels. Talk of 5% wage claims in Australia suggests that this is also rapidly becoming a risk locally. The only sustainable way to get decent wages growth above inflation is to boost productivity growth and that requires significant economic reform.

The danger is central banks won’t be able to get inflation under control without engineering a recession, particularly the longer supply constraints remain. Fed Chair Powell indicated that getting inflation to 2% will “include some pain”.

While shares are getting oversold and investor pessimism is becoming extreme, we are not yet at levels for indicators like Vix or the Put/Call ratio seen at major market bottoms.

However, there is some light at the end of the tunnel.

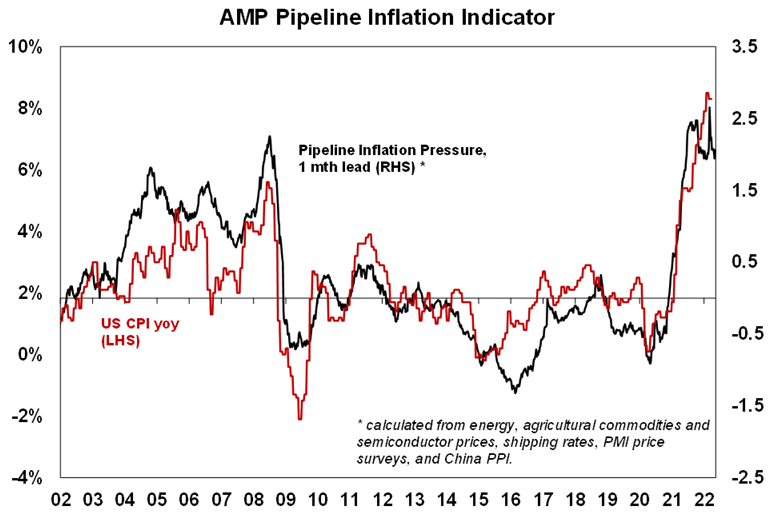

While US inflation is still too high for comfort and may remain so for some months signs of peaking remain evident in our Pipeline Inflation Indicator reflecting lower freight costs and a slowing in commodity prices including oil and gas. This could enable central banks to slow the pace of tightening later this year – in time to avoid recession.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Macrobond, AMP

While services inflation could continue to rise for a while yet there are signs monthly US wages growth may have peaked with eg monthly growth in average hourly earnings looking like it may have peaked late last year.

Share market earnings are continuing to come in stronger than expected. The US March quarter earnings reports are continuing to surprise on the upside and earnings look on track to rise around 12%yoy which is up from initial expectations for a 4.3%yoy gain. And earnings growth in Europe and Asia is averaging slightly faster.

Maybe just maybe some of the risks around a widening in the Ukraine conflict to include NATO countries may be declining. Contrary to the fears of many President Putin did not declare war on Ukraine and announce a general mobilisation signalling an escalation at his 9 May victory over Nazi Germany commemoration speech. It could become another frozen conflict which is horrible for Ukraine and those in the conflict zone but not a further disruptor to global growth. The risks still remain high though with new tensions around Finland wanting to join NATO.

Covid cases in China appear to be slowing which could enable an easing in restrictions and clear the way for policy stimulus to boost growth.

Yield curves have yet to decisively invert and even if they do now the average lead to recession is 18 months – which takes us to late next year which would be too early for share markets to discount as they only look 6 months ahead.

Just focussing on rate hikes ignores the tightening already underway from the ending of QE and the shift to QT, meaning that the Fed may have already tightened a lot and market expectations for a cash rate up to 3% in the US (and Australia) next year may be too hawkish.

So while shares could still see more falls in the short term we remain of the view that a deep (or grizzly) bear market will be avoided as US and Australian recession should be avoided over the next 18 months, which should enable share markets to be up on a 12 month horizon.

Is a terra-fying cryptogeddon unfolding? and what would it mean for global economies and markets? Crypto currencies have been behaving like a high beta version of shares. Like tech stocks they benefitted immensely from easy money and ultra low interest rates and bond yields. So now that easy money is being reversed they are suffering along with tech stocks albeit more so as there was far more hot air involved in cryptos. The risks were highlighted in the past week with the collapse of TerraUSD, an algorithmic stablecoin meant to stay at $US1 through an arrangement with another crypto currency called Luna which could be swapped for TerraUSD and vice versa in order to reduce or raise the supply of the latter to keep it stable. Stablecoins are popular in the crypto world because they allow crypto traders to trade without having to leave the crypto world – a bit like a money market fund in traditional investment markets. But TerraUSD depended on faith in Luna and this was weakened after a series of large withdrawals. It all broke down with TerraUSD falling to $US0.4 with a flow on to demand for other cryptos including Bitcoin which the Luna Foundation Guard sold to raise funds to support Terra at a time when cryptos were under pressure anyway. Bitcoin is now down more than 50% from last years high. Notwithstanding short term bounces, as with shares further downside is a risk if falls feed on themselves and the speculative mania unwinds leading to yet another 80% top to bottom fall. Or buy and HODL may kick in again. With little in the way of fundamental value its hard to know which way it goes. And to the extent that crypto currencies depend on bringing in more investors to keep moving forward a collapse now could have a more lasting impact on interest in it than in the past when it was less “mainstream.” Particularly given that Bitcoin has so far offered little hedge against the surge in inflation over the last year. For the broader financial system and economy a crypto crash poses a risk (particularly if the cash and other $US assets supposedly backing stablecoins like Tether have to be sold) but its unlikely to be another sub-prime crisis. Banking system exposure to crypto is limited and the exposure of the wider investing public is still small (contrary to various surveys claiming the contrary – but which seem more aimed at marketing interest in cryptos). Demand for Lamborghinis may suffer a set back though.

The Australian election is now rapidly approaching with polls pointing to an ALP victory. Two party preferred polling has the ALP ahead by around 55% to 45% and unlike in the run up to the 2019 election we have not seen the narrowing in ALP poll support that ultimately culminated in the Coalition retaining power. A high proportion of “soft voters” in polling suggests it is still unclear. But the key point for markets remains that unlike in 2019, apart from climate change policies the economic policy platforms of the major parties are not that different, so its hard to see a significant impact on markets from a decisive change in government to Labor. The main risk would come if neither of the main parties get enough seats to govern on their own forcing reliance on independents which could force a new government down a less business friendly path, such as the Greens demanding an ALP led minority government implement their proposed super profits taxes.

On rewatching Dark Shadows, the early sequence of the train moving along to The Moody Blues “Nights in White Satin” provided me with a reminder of just how good they are at fusing classical music with rock. “Tuesday Afternoon” also from Days of Future Passed is also one of their best.

Coronavirus update

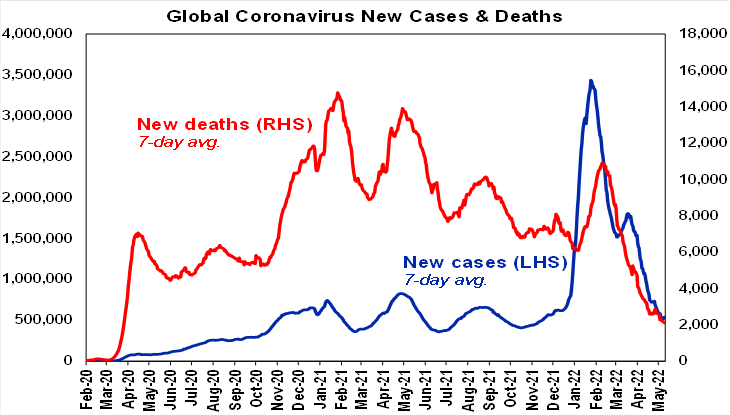

New global Covid cases and deaths have continued to trend down. However, there are signs they may be bottoming and the US is still ticking up.

Source: ourworldindata.org, AMP

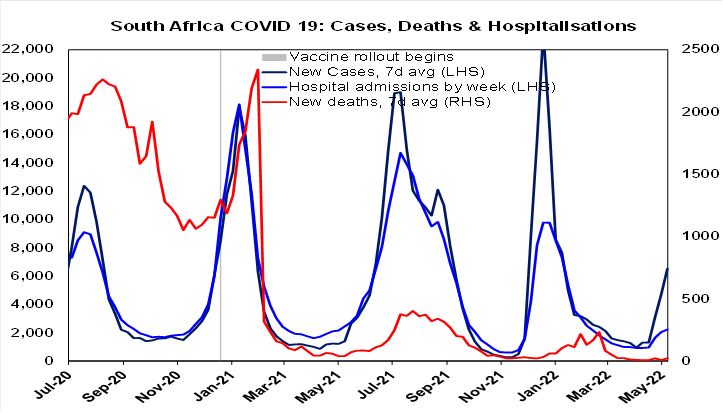

South Africa has seen a sharp upswing in new cases reflecting Omicron sub-variants BA.4 and BA.5 which appear more transmissible again than the original Omicron was and with prior Omicron exposure offering less protection against infection. Fortunately, they do no appear to be more harmful with hospitalisation and death rates remaining subdued compared to pre Omicron waves. Of course, this can still place pressure on hospitals and cause economic disruption due to absences from work if many get it at once.

Source: ourworldindata.org, AMP

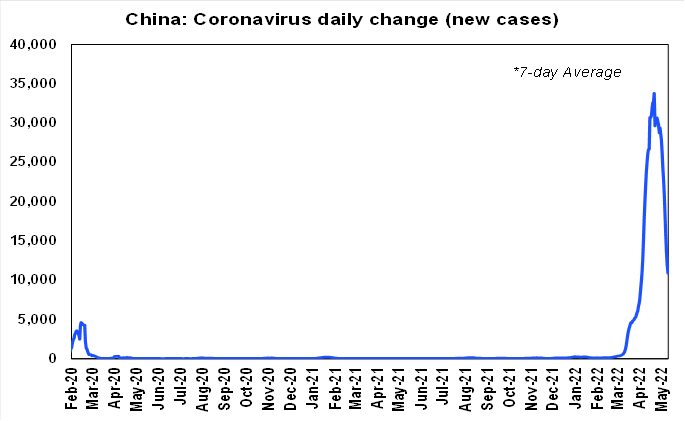

China has seen a significant slowing in new covid cases, which may allow for some easing in lockdowns which would be good news for an easing in global supply concerns. If followed up with more stimulus measures which appears likely it would also be positive for commodity prices, Australian shares and the $A. That said, China may face a far rougher ride if it continues with its zero Covid policy as Omicron is far harder to suppress than the original Covid virus.

Source: ourworldindata.org, AMP

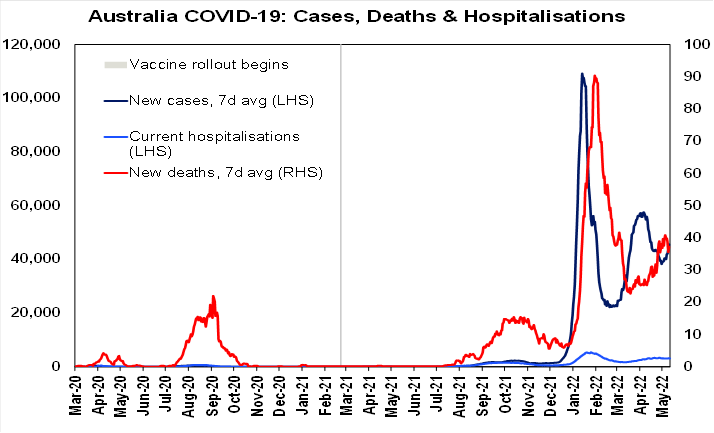

New cases in Australia are on the rise again not helped by new Omicron sub-variants. Hospitalisation and death rates should remain low compared to pre-Omicron waves helped by high rates of vaccination protecting against serious illness and the subvariants remaining mild. But a surge in cases could still cause workforce disruption as we saw in January.

Source: ourworldindata.org, AMP

Economic activity trackers

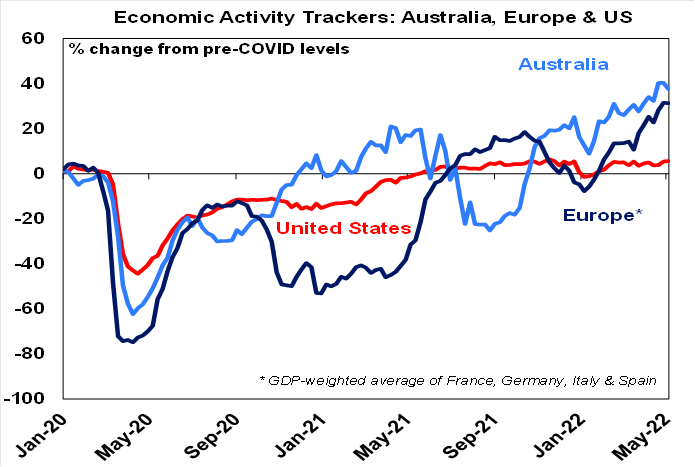

Our Australian Economic Activity Tracker fell over the last week but remains strong. Our European Tracker was little changed but the US improved.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings.

Source: AMP

Major global economic events and implications

US inflation dominated over the last week with both consumer and producer price inflation slowing a bit on an annual basis but remaining too high. Meanwhile jobless claims remain very low but small business optimism remained subdued with a low proportion of firms keen on expansion but continuing high price pressures.

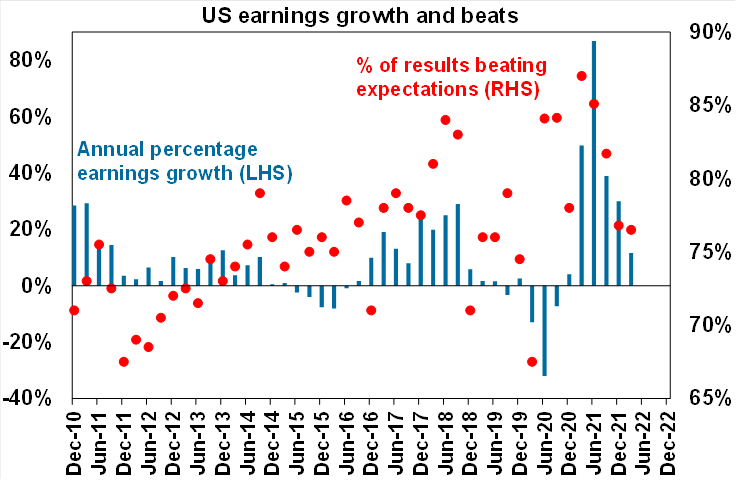

More than 90% of US S&P 500 companies have now reported March quarter earnings with 76% beating expectations which is in line with the norm. However, consensus earnings expectations for the quarter have now moved up to 11.6%yoy from 4.3% at the start of the reporting season. With the average beat running around 7.3% its likely to end up at around 12%yoy. Energy, materials and industrials are seeing the strongest earnings growth. Earnings growth in Europe & Asia has been stronger though averaging 13.9%yoy.

Source: Bloomberg, AMP

Japanese household spending improved in March as covid restrictions were lifted. This also contributed to a further recover in the April Economy Watchers sentiment indicators.

Weak Chinese trade data. Chinese export and import growth slowed in April reflecting coronavirus lockdowns. CPI inflation rose to 2.1%yoy, but this was due to higher food prices with core inflation slowing to 0.9%yoy and producer price inflation slowing further to 8%yoy. Meanwhile, the PBOC reiterated that monetary policy would “increase support to the real economy.”

Australian economic events and implications

Real retail sales growth remained strong in the March quarter. While part of the recent strength in retail sales was due to inflation real retail sales were up a solid 1.2%qoq and combined with likely strength in services spending suggests that consumer spending will make a strong contribution to March quarter GDP growth.

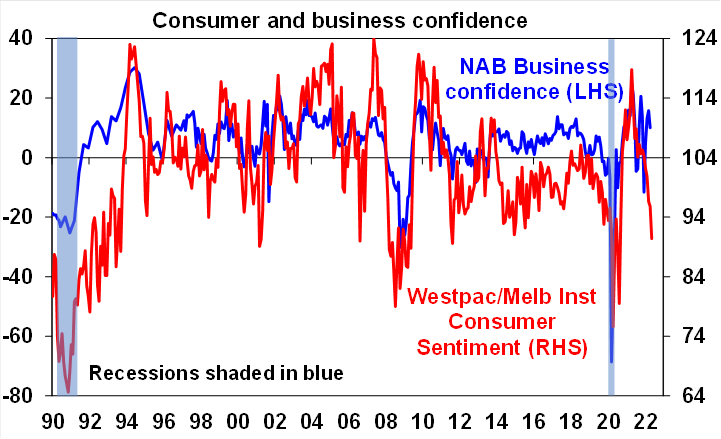

But consumer confidence is now down sharply and there is a big divergence with business confidence. Consumer confidence fell again in May according to the Westpac/MI survey and is now at its lowest since August 2020 thanks to rising prices and rising interest rates. However, while consumers are depressed timely credit and debit card data suggests they are continuing to spend and this is helping keep business conditions & confidence strong, albeit the latter did fall a bit in May. The main concern for businesses are rising costs with labour and purchase costs rising to new highs in April of 3%qoq and 4.6%qoq respectively pointing to further inflationary pressure ahead and adding to pressure for the RBA to increase rates further. We expect the RBA to increase the cash rate by 0.4% at its June meeting and raise it to 1.5-2% by year end, but the massive hit to confidence, the negative wealth effect from falling home prices and the roll over of fixed rate borrowers seeing a doubling in their rates suggests that the peak will be limited to 2.5% next year.

Source: NAB, Westpac/MI, AMP

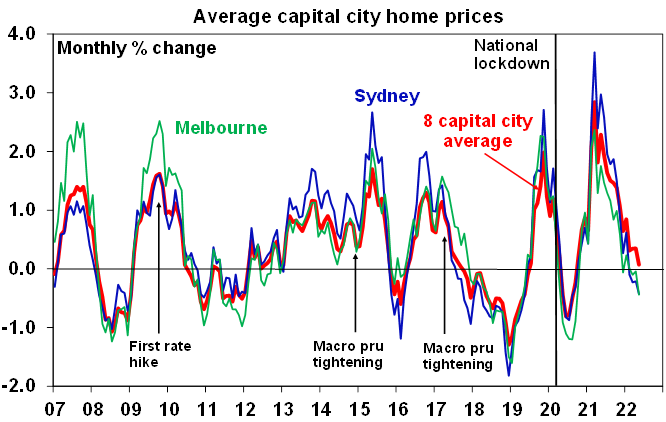

Consumers getting more pessimistic on housing. The Westpac/MI consumer survey showed another deterioration in sentiment towards buying homes with the “time to buy a dwelling’ index falling again in May and down 25% on a year ago, consistent with a further softening in the housing market. So far this month CoreLogic data shows property prices continuing to slow with more falls in Sydney and Melbourne.

Last observation is for May to date. Source: CoreLogic, AMP

What to watch over the next week?

In the US, expect to see solid gains in April retail sales and industrial production but with home builder conditions falling back slightly again (all due Tuesday), housing starts (Wednesday) also likely to fall and manufacturing conditions indexes for the New York and Philadelphia regions likely to pull back slightly in May (due Monday and Thursday).

Japanese March quarter GDP (Monday) is expected to have contracted by -0.5%qoq reflecting the impact of Covid restrictions and inflation data (Friday) for April is expected to jump reflecting the dropping out of the reduction in mobile phone charges a year ago with core inflation rising to 0.3%yoy from -0.7%.

Chinese economic activity data for April due for release on Monday is expected to be hit by Covid lockdowns with industrial production likely to slow to just 0.5%yoy, retail sales likely to contract by -6.2%, investment growth to slow and unemployment likely to rise.

In Australia, the minutes from the RBA’s last board meeting (Tuesday) are expected to be hawkish reinforcing expectations for more rate hikes to control inflation. Thanks to the tight labour market, March quarter wages data is expected to show an acceleration to 0.8%qoq, its fastest increase since 2014 and taking annual wages growth to 2.5%. April jobs data is expected to show a 20,000 gain in employment with unemployment dipping slightly to 3.9%, the lowest since 1974.

Outlook for investment markets

Shares are likely to see continued short term volatility as central banks continue to tighten to combat high inflation, the war in Ukraine continues and Chinese Covid lockdowns impact. However, we see shares providing reasonable returns on a 12-month horizon as global recovery ultimately continues, profit growth slows but remains solid and interest rates rise but not to onerous levels at least not for the next year.

Still low yields & a capital loss from a further rise in yields are likely to result in ongoing negative returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-covid levels and office occupancy remains well below pre-covid levels), but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home price gains are likely to slow further with average prices falling from mid-year as poor affordability, rising mortgage rates and rising listings impact. Expect a 10 to 15% top to bottom fall in prices from mid-year into 2024 but with a large variation between regions. Sydney and Melbourne prices have likely already peaked.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of just 0.1% at present but it should rise as the RBA raises interest rates.

A rising trend in the $A is likely over the next 12 months helped by strong commodity prices, probably taking it to around $US0.80. It’s likely to remain volatile in the short term though.

Ends

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.