Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses the RBA rate hike.

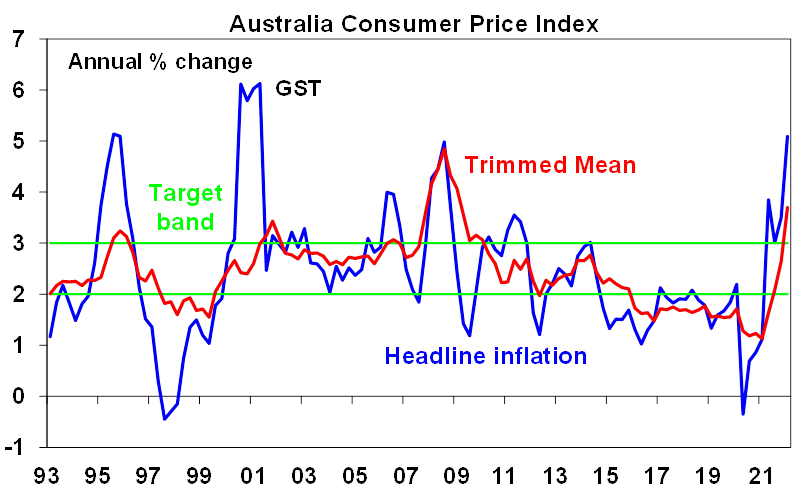

Australian inflation, as measured by the consumer price index, was considerably higher than expected in the March quarter. Headline consumer prices rose by 2.1% over the quarter or 5.1% higher over the year (consensus was for a 1.7% rise or 4.6% over the year). The RBA’s preferred measure of underlying inflation, the “trimmed mean”, was 1.4% higher over the quarter or 3.7% over the year, which was higher than expectations of a 1.2% rise. The other measure of underlying inflation, the “weighted median”, wasn’t as elevated and rose by 1% in the March quarter or 3.2% over the year (which was actually slightly below expectations of a 1.1% rise). These figures are significantly above the RBA’s forecasts (published in early February) of around 0.8% over the quarter on the headline and underlying figures (although the RBA would have presumably updated their forecasts over March to account for the big lift in global commodity prices).

Source: Macrobond, AMP

The March data confirmed that the lift in inflation is occurring across many areas. Global supply-side disruptions (related to high goods demand from consumers, transport issues and backlogs at factories reflecting covid related production delays) are still leading to higher prices, evident in food inflation (+2.8% over the quarter), large household appliances (+3.6%) and small household appliances (+2.3%) but this impact is likely to wane towards the end of the year as supply backlogs are easing and as consumer goods demand declines (in place of higher services spending). This could already be starting, with furniture prices down by 3.4% in the March quarter. Australian floods in NSW and Qld are also leading to higher prices for fruit and vegetables (+5.8% over the March quarter) and meat and seafood (+4.8%) which is also a temporary factor. Commodity prices were already rising in recent months and the Russia/Ukraine war exacerbated commodity supply issues, which lifts input costs across the board, and especially for petrol (up 11% in the March quarter), gas and household fuels (+6.3% over the quarter) and new dwelling purchase by owner-occupiers (+5.7% over the quarter) because of higher costs of housing construction materials (and also fewer HomeBuilder grants paid by the Government). Other large price rises were in education (tertiary education was up by 6.3% over the quarter) from a new fee structure from the job-ready graduate package, which is a temporary factor, and the usual seasonal impacts of changes in the Pharmaceutical Benefits Scheme also led to a rise in pharmaceutical products (+5.7%) and hospital services (+1.8%). The only major large price fall was in international holiday travel and accommodation (-23.1%) from a fall in airline prices.

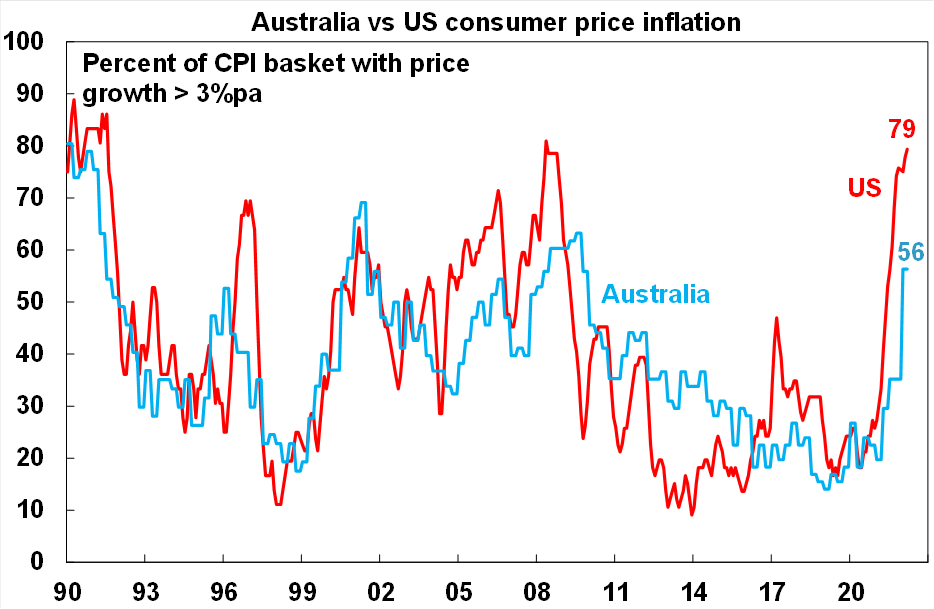

While there are some temporary factors that are leading to a lift in inflation (which could mean that we have seen the peak in quarterly inflation), there has been a cumulative impact on consumer prices from these temporary or short-lived supply issues which are leading to uncomfortably high consumer prices. Impacts from higher commodity prices and global supply issues could also still persist for the remainder of the year which means that we haven’t reached the peak in annual inflation yet. And the breadth of price rises across CPI baskets has also increased. In the March quarter, 56% of CPI categories had a price rise of more than 3% over the quarter, compared to just 35% last quarter (which is still lower than the US at 79%).

Source: ABS, AMP

Implications for the RBA

We now expect the RBA to start hiking at its May meeting next week and by 0.4%, which will take the cash rate to 0.5%. The latest inflation blowout adds significant pressure on the RBA to immediately start raising rates and to do so more aggressively than initially thought likely.

Hiking next week will mean moving before it gets to see March quarter wages data due on 18th May which it has previously indicated its inclined to wait for and may annoy the Government as we are in the midst of an election campaign.

But delaying will only risk an escalation in inflation expectations, with the jobs market so tight it’s only a matter of time before wages growth picks up and various surveys suggest that its already doing so anyway and waiting till June to raise rates will probably have little impact on the election outcome as everyone knows rate hikes are coming anyway. In terms of the election, the RBA will now look more political not to go in May given the surge in inflation.

Keeping inflation expectations down is key to keeping inflation low and stable. But the blow out in inflation suggests Australia is now starting to face the same risks as in various other countries, ie that inflation expectations will get out of control locking in higher than target inflation and making it even harder to get inflation back down again. Hiking the cash rate the first time by just 0.15% (to get the cash rate to 0.25%) won’t send a particularly strong signal in terms of the RBA’s resolve to keep inflation expectations down. So, we expect the first hike to be 0.4% taking the cash rate to 0.5%. We expect another 0.25% hike in June and now see the cash rate rising to 1.5% by year end.

Moving earlier up front – ie the “stitch in time saves nine” strategy now being deployed by the RBNZ - should allow the RBA to slow the pace of rate hikes through next year in order to better to better balance the risk for the household sector which is likely now more sensitive to rate hikes as a result of higher household debt levels. And through next year many fixed rate home borrowers will roll over from 2% rates to around 4% rates which along with the negative wealth effect from likely falling home prices will start to do some of the RBA’s work for it.

But for now the key for the RBA is to make sure it keeps inflation expectations down.

Ends

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.