By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

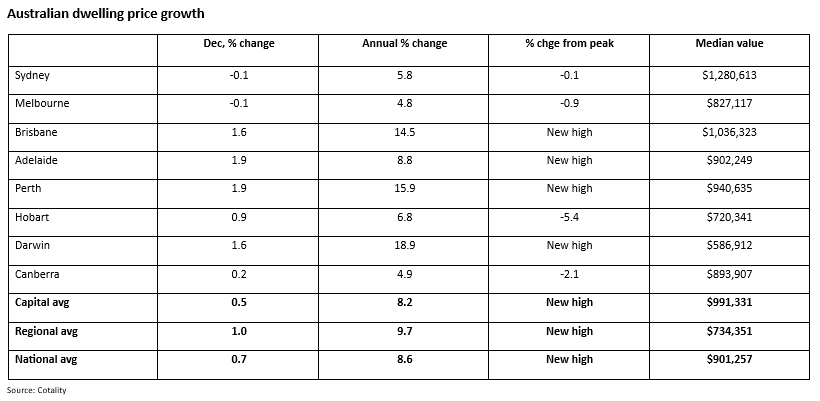

Australian home prices rose 8.6% in 2025, but they are slowing again on rate hike talk

Key points

- Cotality data shows national average home prices rose a strong 8.6% in 2025.

- But momentum slowed in December with prices up for an eleventh month in a row, but the pace slowing again to 0.7%mom. This is partly seasonal, but likely also reflects intensifying talk of rate hikes turning home buyers more cautious. Prices in Sydney and Melbourne actually fell slightly.

- Near record low vacancy rates contributed to rental growth of 5.2%yoy in 2025, up from 4.8%yoy in 2024, although the monthly pace slowed slightly in December.

- The lagged impact of last year’s rate cuts, the expansion of the 5% low deposit scheme and the startup of the Help to Buy Government equity scheme along with the ongoing housing shortage are expected to drive further gains in home prices this year.

- But gains are likely to slow reflecting the less favourable interest rate outlook, with the high risk of rate hikes, poor affordability and possibly further macro-prudential tightening by APRA.

- After 8.6% growth in 2025 we expect property price growth to slow to around 5-7% in 2026. However, this assumes that interest rates remain on hold. If rates rise, home prices could fall slightly.

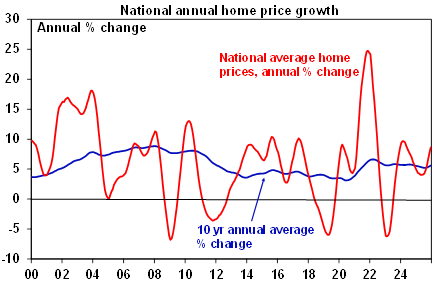

Home prices slowing again

Cotality data shows that national average property prices rose a strong 8.6% in 2025, up from 5.2% in 2024. This was on the back of three rate cuts, the ongoing housing shortage, the expansion of the 5% first home buyer deposit scheme and a continuing boom in prices in Brisbane, Adelaide and Perth.

Source: Cotality, AMP

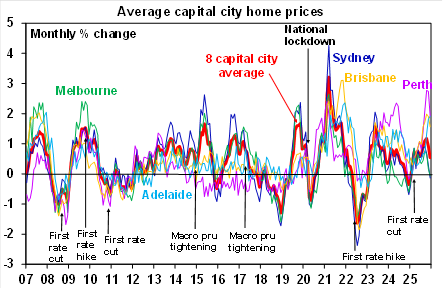

However, price gains slowed in December to 0.7%mom after peaking at 1.2%mom in October. Sydney and Melbourne actually saw prices fall slightly and while Brisbane, Adelaide and Perth continued to boom, Brisbane and Perth are showing some signs of slowing. The slowdown was most pronounced in capital cities, with regional prices up 1%mom in December and 9.7%yoy in 2025.

The slowdown is partly seasonal with December tending to be a softer month for price gains. After seasonal adjustment prices rose 0.9%mom nationally in December and they rose 0.4%mom in Sydney and Melbourne. But the slowdown likely also reflects increasing talk of rate hikes for this year depressing home buyer demand at a time when affordability is already very poor. Poor affordability is likely particularly biting in Sydney along with less negative listings and stronger supply and the malaise around Victoria is likely impacting Melbourne.

Source: Cotality, AMP

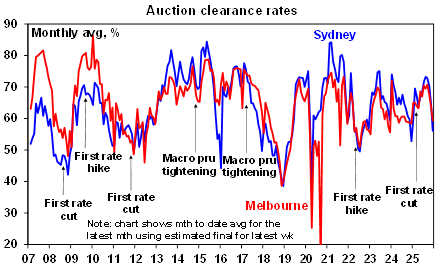

The slowdown is also evident in a greater than the normal seasonal fall in auction clearance rates into December in Sydney and Melbourne from the peak of rate cut optimism in August.

Source: Domain, AMP

House prices surprised on the upside in 2025

The 8.6% surge in property prices in 2025 was stronger than the 3% average rise we expected at the start of the year and reflected a combination of three RBA rate cuts, the expanded first home buyer 5% deposit scheme which was only announced prior to the Federal election, improved consumer confidence and the ongoing shortage of housing. This was also helped by below average levels of listings as vendors held back for higher prices and as lower interest rates relieved the pressure to sell for some distressed mortgage holders. These considerations more than offset the impact of poor affordability.

- Rate cuts tend to be associated with an upswing in property prices unless there has been a recession and sharply rising unemployment. 2025 was no exception with prices starting to rise from February when the RBA started cutting rates. Roughly speaking, the three 0.25% rate cuts added around $35,000 to how much a buyer on average earnings could borrow. Of course, this was more than swamped by a rise in median home prices of $71,400 last year.

- The Federal Government promised prior to the May election that it would expand access to the low deposit guarantee allowing most FHBs to get in with a 5% deposit from 1st October, which had been brought forward from 1st January 2026. And the Government’s Help to Buy Scheme has now started with 10,000 places a year. Both of these demand side policies add to demand by bringing forward purchases and adding to how much a buyer can pay and the property market moved in anticipation of their start up.

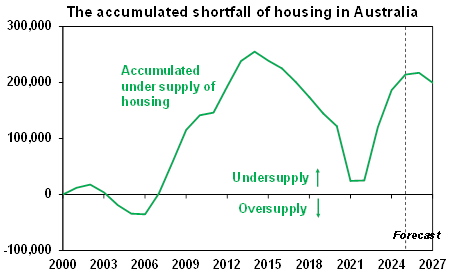

- While a slowing in population growth and improving housing completions brought the property market into better balance on annual basis, there was and still is an accumulated housing shortfall – of around 200,000 to 300,000 dwellings – that has built up over the last few years of under building.

Source: ABS, AMP

Expect prices to continue rising in 2026, but at a slower pace

So what to expect this year? The combination of the lagged effect of this year’s rate cuts, the expanded first home buyer 5% deposit scheme and the Help to Buy scheme, improved consumer confidence and the ongoing shortage of housing are likely to keep the upswing in property prices going in 2026. And the slowdown in prices in December is likely exaggerated by seasonal influences which should reverse in the months ahead. However, the pace of gains is likely to slow from that seen in 2025 as the interest rate outlook has turned less favourable with talk that the next move in rates will be up, APRA starting to ramp up controls to slow risky or speculative lending and affordability is now worse than ever.

- Our view that interest rates will be on hold this year as the recent pickup in inflation reverses somewhat and unemployment rises a bit heading off the need for rates hikes but inflation fears and improving growth prevent rate cuts. However, given the recent run of data showing rising inflation, still low unemployment and strengthening private sector economic growth, we are not particularly confident, and the risks are skewed to the upside on rates. Either way chatter that rates have bottomed with possible rate hikes this year will continue to act as a dampener on buyer demand. Whether rates remain on hold or start to rise, this will leave mortgage rates at their cycle low well above their record lows seen in 2021 of around 2 to 3%. As such, the buying capacity of home buyers is expected to remain below the levels seen in 2021-22. This will limit the upside in property prices.

- APRA is now starting to ramp up macro prudential regulatory controls to cool riskier forms of property lending and further moves are possible. The initial move to cap the proportion of each bank’s housing lending that goes to borrowers with a debt-to-income ratio of six times or more at 20% from 1st February won’t have much impact initially as the aggregate ratio is well below the 20% cap at present, but it’s clearly a pre-emptive move designed to cool investor activity before it gets too hot. If it doesn’t work (and some borrowers may try to get in ahead of the cap becoming binding, so it could actually boost investor lending in the near term) APRA is likely to do more like putting a cap on investor credit growth like the 10%yoy cap it applied in late 2014. Investor lending is already running at a pace in excess of 10%.

Source: RBA, AMP

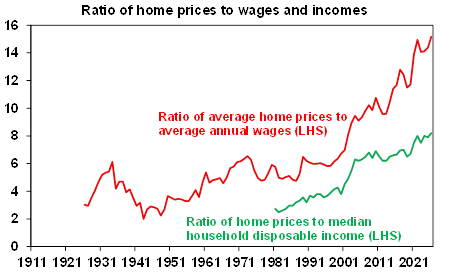

- Housing affordability has deteriorated further from already very poor levels. This is evident in the ratio of home prices to wages and incomes being at record levels. This could limit the upside in property prices – although we and many others have been saying that for years!

Source: Cotality, ABS, AMP

- Finally, slower population growth, reflecting a crackdown on student visas and a return to the normal pattern of students leaving after they complete their degrees (after disruption from the pandemic), may also take some pressure off the home buyer market. Population growth has already slowed from a peak of 662,000 over the year to September 2023 to 420,000 over the year to June quarter with the Government’s immigration forecasts implying a fall to around 365,000 in 2025-26.

Overall, Australian home prices are likely to remain in an upswing in 2026 on the back of the lagged impact of lower interest rates, support for first home buyers and the housing shortage. However, it’s likely to be constrained by the less favourable interest rate outlook with the high risk of a rate hike, the potential for more APRA moves to slow investor lending and poor affordability. After 8.6% growth in 2025 we anticipate a slowing in national average home prices growth to around 5-7%yoy this year. This is based on our view that the RBA leaves rates on hold this year. But if rates start to rise again home prices could fall slightly.

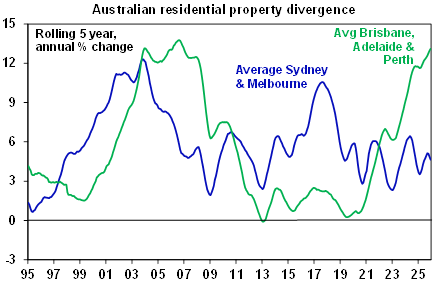

With FOMO running hot in the boom time cities of Brisbane, Perth and Adelaide they are likely to remain the strongest of the state capitals over the next six months. But as their relative affordability continues to deteriorate with average prices around or above those in Melbourne and price to income ratios being well above that in Melbourne they are at risk of some slowdown in the second half of the year.

Source: Cotality, AMP

What to watch?

The key things to watch will be interest rates, unemployment and population growth. A return to rate hikes, a sharply rising trend in unemployment and a sharp slowing in net migration could result in a resumption of property price falls. On the flipside a resumption of rate cuts and faster than expected population growth could drive a stronger rise in property prices.

Ends