By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

Investment markets and key developments

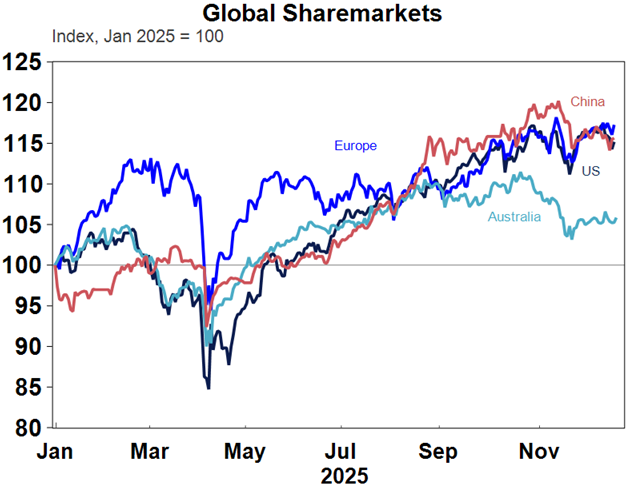

Global shares were mostly week again over the last week with US shares dragged lower by ongoing AI bubble worries despite a boost later in the week from lower-than-expected inflation data. Eurozone shares rose slightly but Japanese and Chinese shares fell. Australian shares also fell around 0.7% for the week on the back of the weak US lead and ongoing expectations that the RBA will raise rates again next year. Australian financial and consumer stocks saw small gains, but most sectors fell for the week with big falls in resources, health and IT shares. Bond yields fell in the US and Europe but rose in Japan on Australia and expectations for rate hikes.

Source: Macrobond, AMP

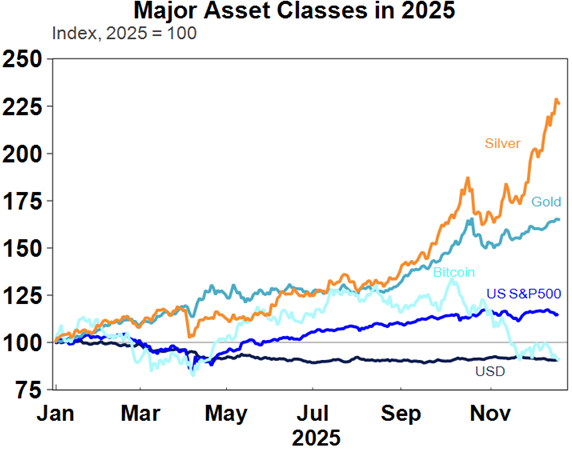

The past week saw gold continue to grind higher, but silver pull back and Bitcoin head back to around its November low. Gold is likely to continue to benefit particularly on concerns that President Trump will seek to weaken Fed independence by nominating a new Fed Chair “who believes in lower interest rates, by a lot”. Metal and iron ore prices rose but oil prices fell to their lowest for the year helped by a glut of oil globally. The latter was despite a US blockade of oil tankers going into and out of Venezuela as it only produces about 1% of global oil production (despite having 17% of proven global reserves) because gulf states can easily make up any loss. The $A fell slightly and the $US was little changed.

Source: Macrobond, AMP

After a nice bounce from their November lows shares have been under pressure again. Our view remains that the renewed weakness in the last two weeks is corrective and that the rising trend in shares likely remains in place as global growth remains okay, the Fed has left the door open for more rate cuts, earnings growth is likely to remain strong in the US and looks to be picking up in Australia, Trump is moving towards more consumer friendly policies ahead of next year’s mid-term elections and we are in a period of seasonal strength for shares. Relative strength in consumer discretionary and material shares along with small caps, metals and the $A are positive signs from a cyclical perspective.

However, the current correction could still go further with a possible double top having formed in the US share market. AI worries and an imminent Supreme Court ruling on Trump’s emerging powers tariffs could also cause near term worries for shares. In terms of the latter if the Supreme Court rules against the tariffs it could create significant short term uncertainty. Trump can replace the tariffs with a power that gives him the ability to impose up to 15% tariffs for 150 days and then use another power to run fair trade reviews (as has been the case with some of the tariffs on China and sectoral imports) and move back to current levels more permanently. However, this would take time and in any case there would be near term uncertainty around whether the tariff revenue raised would have to be returned (which could amount to $200bn or so), what will happen to all the trade deals Trump negotiated and would the tariffs under other powers also be subject to challenge. At the very least it could create upwards pressure on US bond yields on fears about a renewed deficit blow out and higher bond yields could make life harder for shares. And a defeat for the tariffs which have been Trump’s key policy on top of election defeats could see the Trump Administration become more erratic (as occurred back in 2020 with covid).

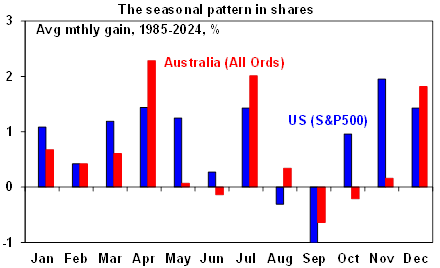

Out of interest the Santa rally normally kicks in around mid-December on the back of festive cheer and new year optimism, the investment of any bonuses, low volumes and no capital raisings at this time of year. Over the last 15 years the period from mid-December to year end has seen an average gain of 0.3% in US shares with shares up in this two-week period 9 years out of 15. In Australia, over the last 15 years the average gain over the last two weeks of December has been 0.9% with shares up 9 years out of 15. Of course, it’s not guaranteed and Santa didn’t come late last year with a bout of nerves ahead of the incoming Trump Administration – he then came in January this year.

Source: Bloomberg, AMP

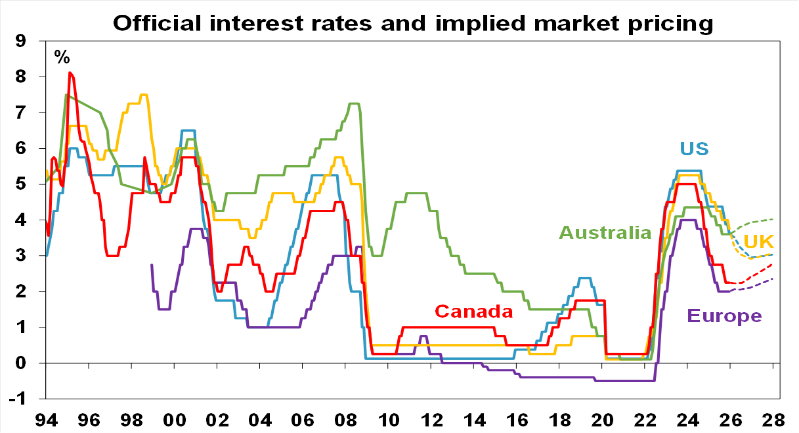

The past week saw another round of central bank moves – this time going in different directions. The European Central Bank left its deposit rate at 2% as widely expected with a neutral to slightly hawkish bias as growth and inflation forecasts were revised up and President Lagarde reiterated that policy is “in a good place.” There is still some chance of another cut though, as inflation is forecasts to be below target until 2028, but its low and the money market basically sees the ECB on hold next year. The Swedish and Norwegian central banks also left rates on hold.

Meanwhile the Bank of England cut rates by another 0.25% to 3.75%, but it was a very close vote and came with cautious commentary about future cuts. It is lagging in the rate cutting cycle due to higher inflation but another cut or two is likely next year supported by a fall in core inflation to 3.2%yoy in November and soft jobs data.

Going the other way though the Bank of Japan continued the very gradual process of normalising its interest rates with a 0.25% hike to 0.75%. This has been well flagged and is consistent with inflation being more in line with the 2% inflation target (core inflation was 1.6%yoy in November) and signs that the economy remains okay with the December quarter Tankan survey showing mostly solid business conditions. The next hike is likely 6-9 months away and Japanese rates are still too low and rising too slowly to cause a big reversal of the so-called carry trade.

In Australia, our view remains that the RBA will leave rates on hold next year, but with the RBA determined to ensure that inflation heads back to target the risk is skewed to a rate hike. The key will be what happens to inflation and our view remains that December quarter inflation data to be released at the end of January will show trimmed mean inflation back in line with RBA forecasts (for a 0.8%qoq or 3.2%yoy rise) allowing it to sit tight on rates. Relatively benign readings for output prices in the NAB and PMI business surveys are consistent with this. And the fall back in consumer confidence and auction clearances highlight the fragility in household spending should rates rise.

Dashed lines show money market expectations. Source: Bloomberg, AMP

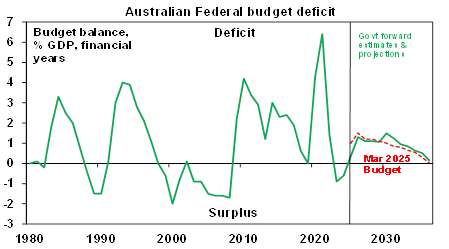

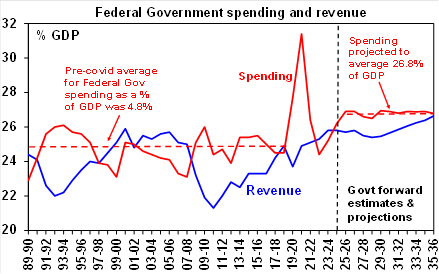

The Australian Government’s mid-year budget update (MYEFO) saw some spending restraint, but deficits and high spending are still locked in. There was another round of revenue upgrades (helped by higher than expected commodity prices) of around $41bn over four years and $20bn savings offset new spending and stronger than expected spending under existing programs result in lower budget deficits forecasts for the next four years than forecast back in the March Budget. But the reduction was only $8.7bn, still leaves in place sizeable deficits and they now look worse beyond 2028-29.

Source: Australian Treasury, AMP

While Australia’s budget and public debt situation is a non-event compared to many other comparable countries, the picture painted in the MYEFO has four major concerns.

- Firstly, the policy stimulus from a swing into bigger budget deficits this financial year is now going to be around 1% of GDP and doesn’t make things any easier for the RBA in battling a renewed pickup in inflation.

- Secondly, public spending is getting locked in at a permanently higher share of the economy compared to before the pandemic. This doesn’t augur well in terms of turning around poor productivity growth and hence in terms of boosting living standards. The continuing high level of public spending is adding to the capacity constraints in the economy at a time when Federal and State governments should be cutting public spending to free up resources in the economy to allow for the nascent recovery in private sector spending. The failure of the Government to cut back spending will only mean higher than otherwise inflation and interest rates.

Source: Australian Treasury, AMP

- Thirdly, the deficit projections don’t really look that believable as spending growth looks unrealistically low in the next two years and the return to balance over the next decade is reliant on bracket creep which is unfair and prone to be reversed by tax cuts ahead of elections.

- Finally, the increasing amount of spending on things like climate, manufacturing and housing now “off budget” in that its supposedly an investment, means the underlying cash deficit is understating the actual deficit because this spending still adds to debt and is a cost to taxpayers.

Ideally the Government needs to slash spending including via greater means testing of access to government programs and adopt quantifiable budget rules like previous governments did. This should be reviewed in a new Charter of Budget Honesty.

Major global economic events and implications

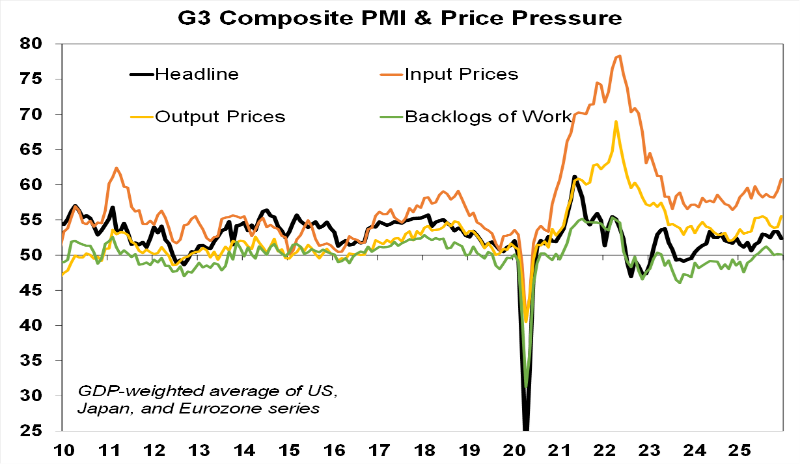

Aggregate business conditions PMIs in developed countries softened on average in December with falls in the US, Europe, Japan and Australia. They are at levels that continue to point to okay but moderate economic growth. Input and output prices rose, mainly due to the US.

Source: Bloomberg, AMP

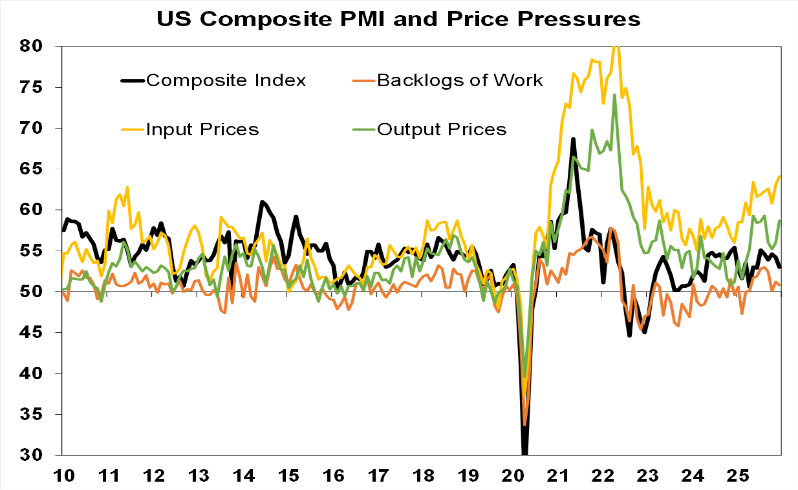

The US composite PMI slowed in December with input prices and output prices up and remaining at elevated levels. “Tariff derangement syndrome” (or reality) must still be impacting! Regional manufacturing conditions indexes were weak in December though and home builder conditions rose but remain weak.

Source: Bloomberg, AMP

Fortunately, the November CPI came in softer at 2.7%yoy for headline and 2.6%yoy for core, but it needs to be treated with caution. This in turn implies core PCE inflation of around 2.6%yoy and with tariffs likely accounting for some of that and their impact likely to peak out early next year it should allow lower inflation ahead. However, the November CPI was likely biased downwards by the shutdown with some cities seeing flat rents due to no October survey and the November survey occurring later than normal and so picking up more holiday sales. So, we will have to wait for December data to get a clearer picture.

Source: Bloomberg, AMP

Meanwhile, delayed US jobs data for October and November confirm a slowdown but it’s not yet calamitous. On the one hand unemployment rose to 3.6%, wages growth slowed further to 3.5%yoy (which is no problem for inflation if productivity growth is 1.5-2%) and payroll growth is continuing to trend down. Against this, delayed DOGE layoffs distorted payrolls down in October and the trend in private payroll growth is a bit stronger. So, all up it supports a case for a further Fed rate cut but suggests there is no urgency after seeing three cuts. December jobs and inflation data due in January will likely be key for the Fed at its late January meeting. US initial jobless claims remain relatively low but continuing claims rebounded (after the Thanksgiving distortion).

Source: Macrobond, AMP

Retail sales remained solid in October. While the headline was flat, excluding autos and gasoline they rose a solid 0.5%mom, which suggests that US consumers are still spending okay despite poor consumer confidence levels.

Source: Macrobond, AMP

Canadian inflation data showed underlying measures falling to 2.8%yoy. It’s unlikely to change the outlook for the BoC to keep rates on hold at 2.25% though.

Source: Macrobond, AMP

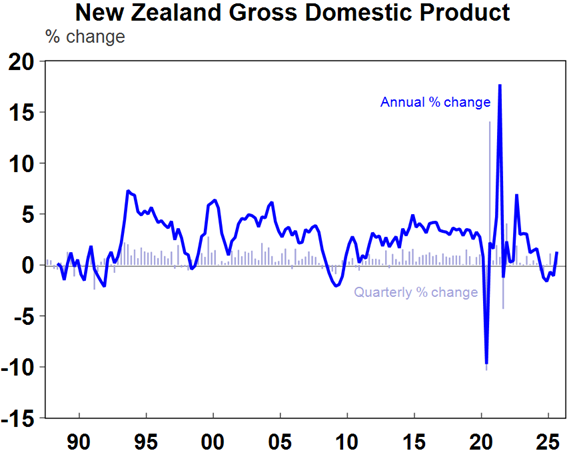

New Zealand’s economy picked up last quarter with better-than-expected GDP growth of 1.1%qoq or 1.3%yoy. NZ growth is very volatile though and the rebound was driven by investment and trade with flat consumer spending but the rate cuts of the last year or so are likely to drive a further recovery going forward albeit at a slower rate.

Source: Macrobond, AMP

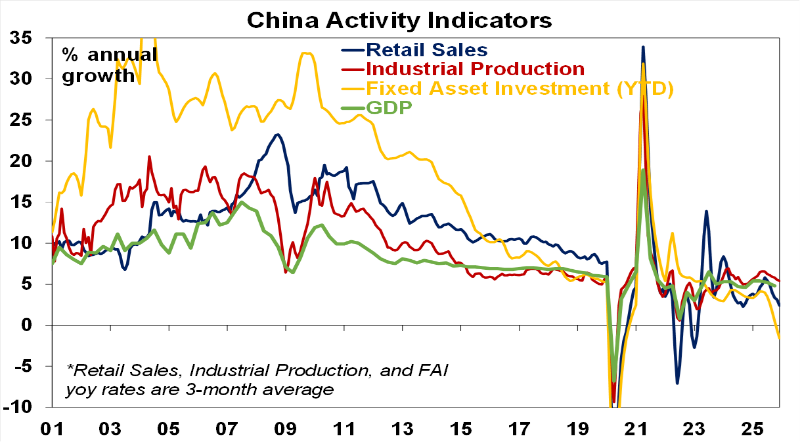

Chinese data for November slowed further with growth in industrial production slowing to 4.8%yoy, retail sales at just 1.3%yoy and investment down around 11%yoy not helped by the ongoing slump in property investment and policies to reduce excess capacity. Home prices continue to fall. While growth in 2025 may still come in around 5%, the weakness adds to the case for further policy stimulus with the previous week’s Economic Work Conference suggesting further incremental stimulus measures are on the way.

Source: Bloomberg, AMP

Australia economic events and implications

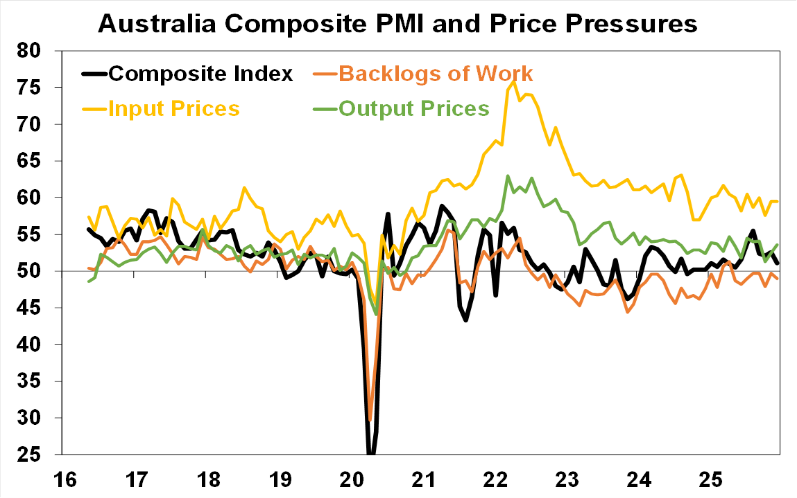

Australia’s December composite PMI fell 1.5 points to 51.1 suggesting a more gradual pickup in economic growth going forward. Input price pressures were flat and output price pressures rose but the latter remains in the same moderate range it’s been in the for the last two years and suggest that the upswing seen in CPI inflation since mid-year may be temporary.

Source: Bloomberg, AMP

Consumer confidence as measured by the Westpac/MI survey fell 9% in December on the back of rate hike talk. Confidence is back to its average for the year remains soft. Perceptions of whether now is a good time to buy major household items saw the sharpest fall. The alternative ANZ/Roy Morgan confidence index is far weaker. This suggests the upswing in consumer spending may be fragile and particularly vulnerable if interest rates start rising again.

Source: Westpac/Melbourne Institute, ANZ/Roy Morgan, AMP

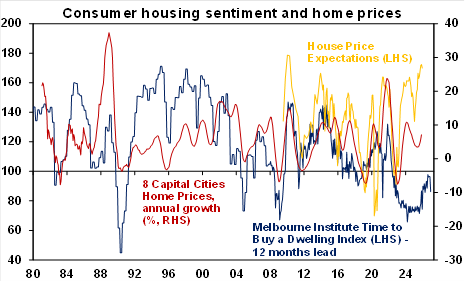

The Westpac/MI consumer survey showed home price growth expectations remain very strong. But perceptions as to whether now is a good time to buy a dwelling fell sharply in December. This is consistent a slump in auction clearance rates and slowing home price growth lately.

Source: Cotality, Westpac/MI, AMP

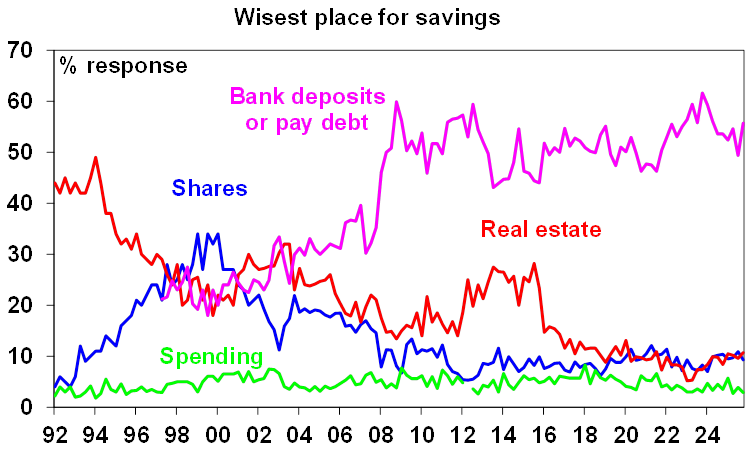

Consumers remain cautious in terms of the wisest place for savings, favouring bank deposits and paying down debt. I guess they have been since the GFC so its not new.

Source: Westpac/Melbourne Institute, AMP

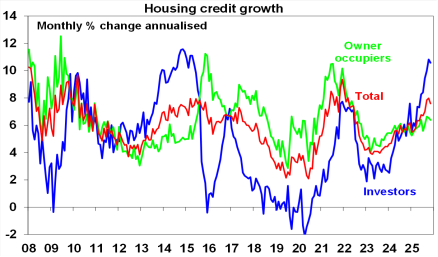

Private credit growth slowed slightly in November due to a fall in personal credit with housing credit also slowing a bit. But growth in lending to investors remains very strong, potentially meaning more moves by APRA to slow it.

Source: RBA, AMP

Real Estate Institute of Australia data for the September quarter shows rental growth stabilising after a sharp slowing but still low vacancy rates, the housing shortage and accelerating asking rents suggests its bottomed.

Source: REIA, AMP

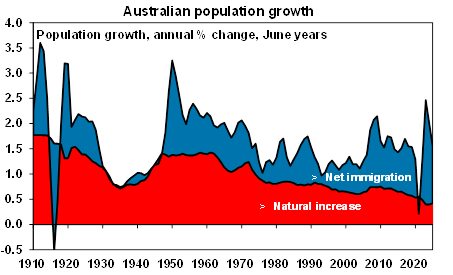

In terms of housing demand, population growth slowed to just 0.3%qoq in the June quarter or to 1.5%yoy or 420,100 over the year to the June quarter. This is down from a record 2.5%yoy population growth in 2022-23 and reflects a slowdown in net overseas migration from 538,300 to 305,600. Slower population growth means slowing underlying demand for housing and on our estimates annual underlying demand is now back to around balance with the annual supply of housing. But the shortfall built up over years of excess housing demand remains around 200,000 to 300,000 dwellings and will take years to reduce.

Source: ABS, AMP

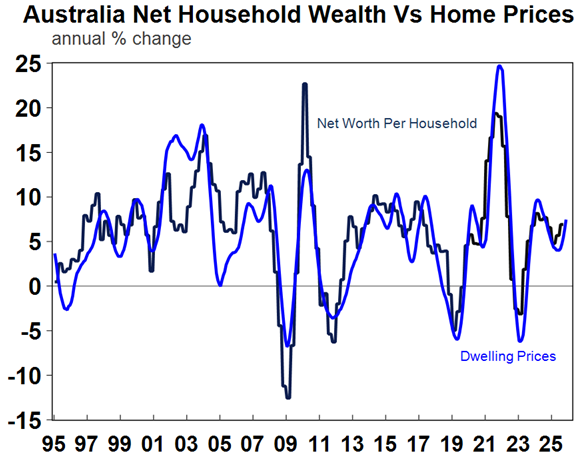

Rising wealth is driving a positive wealth effect for Australian households which helps boost consumer spending. Over the last year net household wealth is up around 7%yoy or nearly $1.5bn mainly driven by rising house and land prices and rising super balances.

Source: Macrobond, AMP

What to watch over the next three weeks?

In the US, the key indicators to watch over the next three weeks include delayed September quarter GDP which is expected to show solid annualised growth of 3.2%, consumer confidence which is expected to improve slightly and capital goods orders which is expected to show modest growth (all due 23rd December), November retail sales which is expected to show weak growth (possibly on 29th December), the December manufacturing conditions ISM which is expected to remain soft around 48 (5th January) and December jobs data which is expected to show modest growth in payrolls and unemployment around 4.6% (9th January). The minutes from the last Fed meeting will be released on 31st December and will be watched for whether the Fed is inclined to pause on rates after three cuts.

In the Eurozone, inflation data for December (7th January) is expected to show core inflation remaining around 2.4%yoy with unemployment for November (8th January) remaining around 6.4%.

Chinese December business conditions PMIs (31st December) are likely to remain soft.

In Australia, the minutes from the last RBA meeting (23rd December) are likely to confirm that the RBA remains cautious and biased to raise rates early next year if upcoming inflation data does not provide confidence that it’s heading back to target. Some imperfect guidance on this will be provided by November monthly CPI data (7th January) which we expect to show some slowing to 3.7%yoy with trimmed mean inflation cooling to 3.1%yoy helped by Black Friday price discounts. Cotality home price data for December (2nd January) is likely to show a further slowing in average price gains to 0.6%mom, down from 1% in November as rate hike talk dents buyer confidence particularly in Sydney and Melbourne where home price growth has stalled in contrast to Brisbane, Adelaide and Perth where it remains strong. Home price growth for 2025 is likely to come in though at a strong 8.3%yoy, up from 5.2%yoy in 2024. In other data, expect a 4% fall in November building approvals (7th January) and the trade surplus to rise slightly to around $5bn (8th January).

Outlook for investment markets

After three years of strong returns, it’s inevitable that investment returns will slow. We have seen a bit of that in 2025 but expect a further slowing in 2026.

Global and Australian share returns are expected to slow further in the year ahead to around 8%. Stretched valuations in the key direction setting US share market, political uncertainty associated with the midterm elections (which years have seen below average returns and increased volatility) and AI bubble worries are the main drags but returns should still be positive thanks to Fed rate cuts, Trump’s consumer friendly pivot and solid profit growth. A return to profit growth should also support gains in Australian shares even though the RBA may have finished cutting rates. Another 15% or so correction in share markets is likely along the way though.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to stay solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to around 5-7% in 2026 after 8.3% in 2025 due to poor affordability, rates on hold with talk of rate hikes and APRA’s move to ramp up macro prudential controls.

Cash and bank deposits are expected to provide returns around 3.6%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA holds and possibly hikes. Fair value for the Australian dollar is around $US0.73.

Ends