For a full copy of our weekly report please contact me directly.

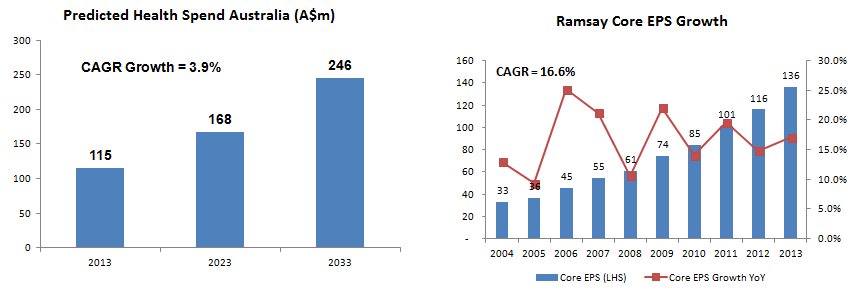

The aging population trend leads to a higher percentage of people in the over 65 age group. This is usually the retiree demographic, who no longer part of the work force but more importantly will spend a higher amount on health care than younger age groups. The other major issue facing developed countries is the obesity epidemic and it is pretty common knowledge that the US is leading the world with 35.7% of the population classified as obese. Obese people suffer a range of health issues that include respiratory, cardiovascular and diabetes illnesses to name a few. So the aging population problem along with an increasing obesity rate has led the AIHW (Australian Institute of health and Welfare) to predict that compounded annual health spend in Australia will increase by 3.9% over the next 20 years, which is higher than the rate of economic growth at around 2-3% rate. This problem might be dire for the next generation of young people but it is extremely bullish for the health sector. As the largest operator of private hospitals in Australia we think RHC will go on benefiting from the above GDP growth rate of healthcare expenditure.

RHC still derives a greater part of its profit from its network of Australian private hospitals, consisting about 93% of company net profits. From a regulatory stand point Liberal governments have been encouraging of private health insurance (PHI) and private hospitals in the Australian heath sector. The combination of the old carrot and stick policy that John Howard introduced to health insurance has meant that private hospitals now make up about half of all Australian hospitals. The 1% Medicare surcharge was the stick which hurt people who didn’t take up PHI and the 30% PHI rebate was the carrot that helped to enticed people to take up PHI. With its four prone strategy RHC has been able to grow the company’s core EPS by a compounded annual rate of 16.6% over the last 10 years. In fact RHC is the only company to achieve that type of growth on the ASX over the period consistently year after year, and it has now become a poster child for a growth company, and its valuation of 27x 12 month forward earnings shows that it is a well-loved and well owned stock among investors. RHC’s four prone strategy includes:

1. Organic growth from existing assets by implementing cost initiatives

2. Spend capital on brown field expansions at its existing hospitals where returns are above the cost of capital

3. Acquire hospitals or facilities which add to the footprint and is value accretive

4.

Public/private collaborations where RHC can provide public hospitals with new capability at competitive rates

The demographic changes and high level of health care spend over time mean that RHC will have plenty of growth opportunities, and we see the stock as something to add to the portfolio for the long term, especially on equity market pullbacks.

The Ramsay Santé acquisition in 2013 increased company net debt by A$157 million but gearing only increased 1% to 31%. The defensive and recurring nature of RHC’s revenues makes us very comfortable with this level of gearing and that the company has the ability to meet its debt obligations. RHC’s returns has been very strong, always a few percentage points above its cost of capital. But more importantly its incremental return on capital invested has been running above 20%, a testament of the many growth options it has to invest its cash flows.

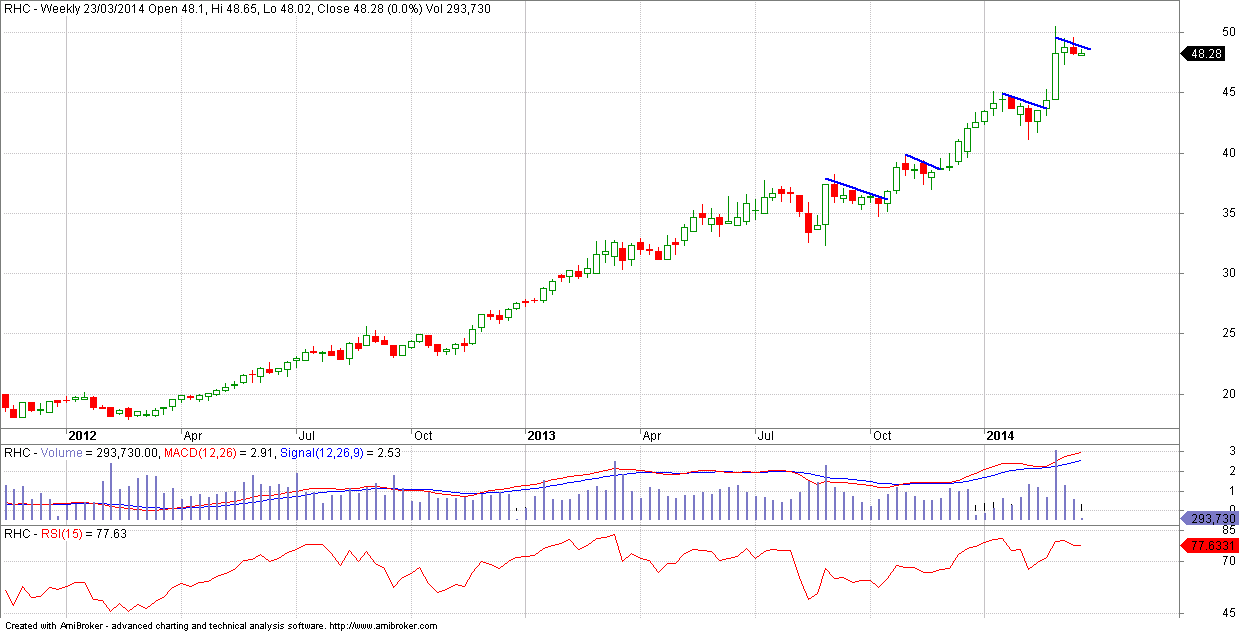

RHC has been trending up for 5 years now, seeing its share price increase fivefold. The last several months in particular have seen a noticeable pattern of impulsive moves up followed by corrective declines every now and then. The stock looks overbought but no reversals are yet evident. As a result, the strategy would have to be to buy any dips and not get too greedy because it won’t be long until the uptrend resumes. At this point in time, the previous swing low is at $41.06 so as long as it holds that level, the trend is still bullish.