Date of Data Capture:

20/9/2017

Name:

EML PAYMENTS LTD (EML)

Classification:

Transaction & Payment Services

Current Price:

$1.945

Market Capitalisation:

$476M

Forecast Sales Growth:

35.9%

Yield Estimate:

0%

Consensus Price Target:

$2.03

# Covering Analysts:

4

Discount at Current Price:

4.37%

Price Target Trend:

Increasing-Flat

Signal Timeframe:

Monthly-Weekly-Daily

Trend Bias:

Up-Flat / Long-Short

Indicators:

Short-term:

Positive-Neutral

Medium-term:

Positive-Neutral

Long-term:

Positive

Recommendation:

Buy

Focus:

Capital Growth

Set up Notes:

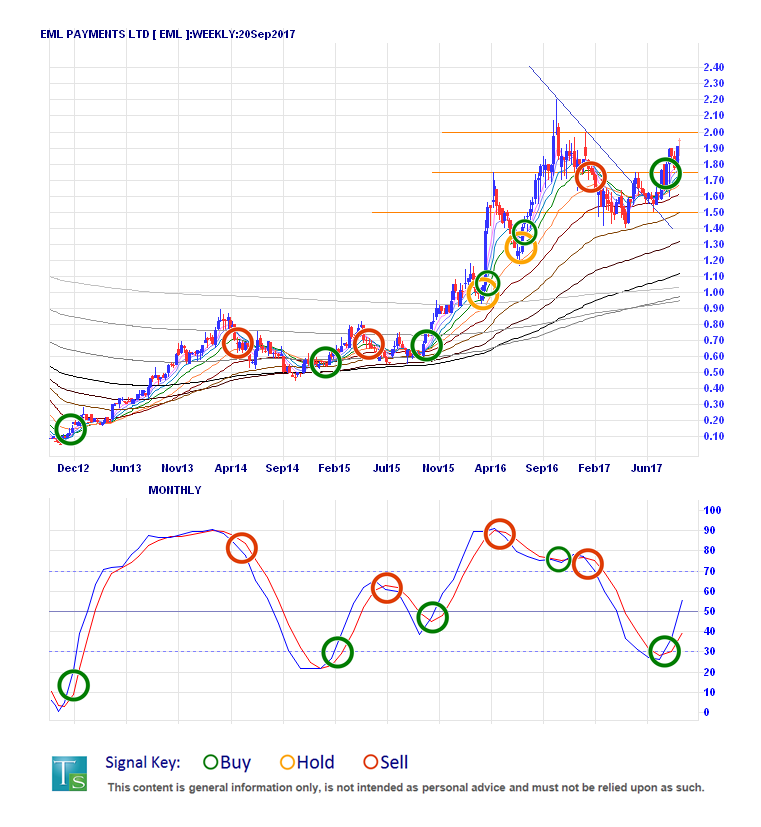

• EML is moving out of a 12-month medium-term consolidation after rising over 200% from late 2015 to late 2016. Right now they are pushing up against $2 resistance but show good fundamental and technical momentum here.

• Earnings growth has been strong over the last two years and this is set to continue with strong forecasting for sales, earnings and profits through to 2020, maintaining steady margins.

• Positive signals cross the major timeframes though expect volatility and a pullback or two before the ceiling breaks to reveal the old peak high target at $2.20 and blue sky above.

• Structural resistance sits at $2.00 and $2.20 with structural support layered from $1.90 to $1.80.

Growth Focus:

EML Payments Ltd (EML)

Our primary focus here is capital gain, we will select our stocks from the ASX top 500 All Ordinaries Index.

When the cards are running hot it makes sense to increase your stake. That is what we are looking to do here with EML Payments Ltd (EML) as the payment solutions company continues to their winning streak of strong earnings and profit growth. With excellent performance and strong forecasting ahead of them, we are confident they will stay ahead of the pack.

Originating from Queensland, EML began dealings in 2003 as a gift card provider but has since grown to offer payment solutions to major global corporates across Australia, Europe and the US. Totalling billions of dollars, these payments are facilitated through over 800 payment, payout, gift and reward programs using physical, mobile and virtual payment cards. With ongoing expansion moving ahead with new contracts and acquisitions in Europe and North America we think the odds are stacked in their favour.

EML has shown excellent fundamental performance and grew earnings by over 50% last year (over 100% the year before) and seem set for continued growth with consensus forecasts upping the ante with strong earnings growth seen carrying through to 2020. Expectations are positive across sales, profits and earnings and the attractive forecasts are supported by high margins that are also set to increase to nearly 80% in the near future. With low costs and good cash flow we see plenty of potential for continued organic growth being bolstered by an acquisitive growth strategy that should see them remain a cut above the rest.

Technically, in the bigger picture we see pricing in the early stage of a potentially significant new long-term uptrend after EML consolidated back by 36% over 12 months from their peak price achieved in late 2016. This peak followed a rally of 266% that began the year prior with a similar long-term signal we are following here again. After basing around $1.50 early in 2017 they broke linear resistance by mid-year and began rally back up to where we find them now, working against $2.00 structural resistance. While we see good momentum across most of the major timeframes, we do expect some volatility and even a potential pullback as the price chips away at that ceiling, but you would need a big blind spot to not see their potential.

With excellent performance, aggressive forecasting and an exciting growth profile backed by strong cash flows, we are happy to chip in and lay our cards on the table as we are confident EML Payments Ltd will continue to come up Trumps.

**Disclosure: Taylor Securities clients and staff may have exposure to the stocks we research and write about.**