Date of Data Capture:

27/7/2017

Name:

HANSEN TECHNOLOGIES LTD (HSN)

Classification:

IT Services & Consulting

Current Price:

$3.83

Market Capitalisation:

$737M

Forecast EBITDA Growth:

25.81%

Gross Yield:

1.69%

Consensus Price Target:

$4.24

# Covering Analysts:

4

Discount at Current Price:

10.70%

Price Target Trend:

Increasing-Flat

Signal Timeframe:

Monthly-Daily

Trend Bias:

Up-Down / Long-Short

Indicators:

Short-term:

Positive

Medium-term:

Neutral

Long-term:

Positive

Recommendation:

Buy

Focus:

Capital Growth

Set up Notes:

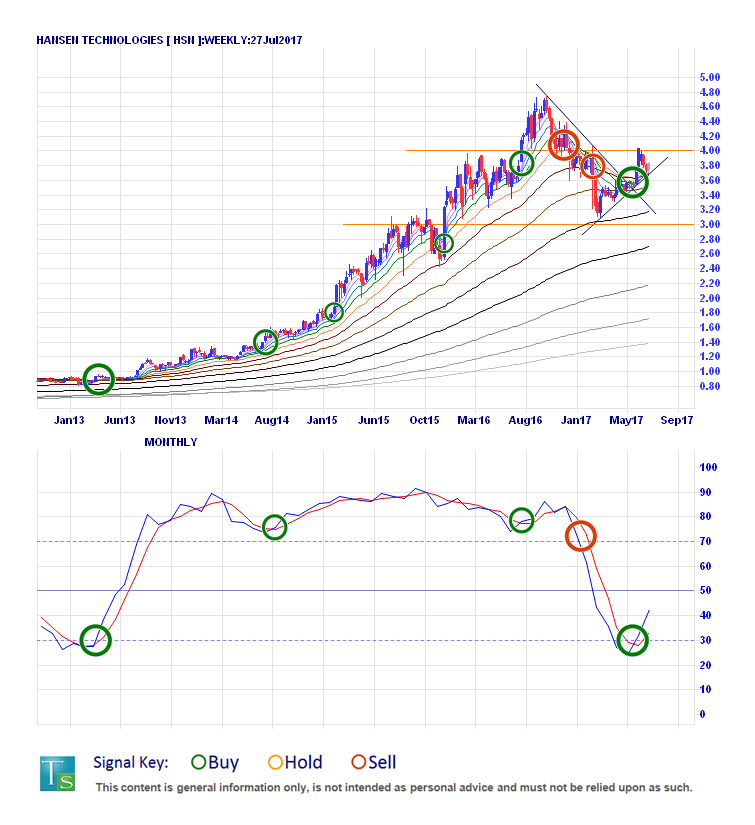

• Finding buying opportunities in HSN has been difficult as they gained nearly 500% since 2013 within a very robust uptrend – with them consolidating down by around 35% over the last 6 months this could be our chance.

• Fundamentally sound, they have a good history of sustained strong earnings growth – though this dipped going into 2017 it is forecast to get back on track through 2018 and out to 2019.

• Technically sound with good analyst sentiment, we come to them after pricing broke linear resistance in May before rallying to $4 resistance, pulling back to bounce off support around $3.70 which is where they are now.

• With short-term signalling returning to positive we are following the well-correlated long-term model, with good support layered down to $3.

Growth Focus:

Hansen Technologies Ltd (HSN)

Our primary focus here is capital gain, we will select our stocks from the ASX top 500 All Ordinaries Index.

When selecting stocks we tend to start with an inventory of attributes we score, compare and rank. At the end of this process we have a simple ledger of what we believe to be the best of the best – stocks that held good account of themselves in both fundamental and technical terms. This time, billing systems developer Hansen Technologies Ltd (HSN) was headlining our results and is a balanced choice, combining excellent fundamental and technical credentials. Their history of price performance is strong and adds well to their steadily increasing dividend that continues to raise interest.

Charging forth from Doncaster back in 1971, Hansen began as a pioneering internet based customer service company and has evolved to provide supported billing systems to energy and utilities, telecommunications, and pay-tv industries. With reliable and recurring revenue streams HSN has been seen as a defensive play, but also one with enviable performance seen across sales, earnings and profits for the last few years and enviable price growth reflecting that. While 2017 is forecast to be more modest, performance is expected to pick up into and past 2018 and we think they are definitely a stock to keep tabs on.

Even though organic growth has been a key driver behind HSN, they have also tallied up a number of acquisitions on their path to their current position, spanning 45 countries. Just this month a fundraising was done to raise $50M at $3.70 to pay for the takeover of a Norwegian-based energy billing company. This is significant as it fills detail into the bigger picture of an expansive 2018 – but also that this effectively adds a psychological floor of support at $3.70, in addition to the support established during the last months of their seven month correction through to March 2017. With price finding support and breaking resistance it looks like they could be about to make a much more positive statement going forward.

Take note that while they currently offer a good discount this could come in handy with structural price resistance directly overhead at $4.00 - a barrier that held just 4 weeks ago. Even though we expect some continued volatility here, we are following a well-correlated longer-term signal that last triggered back in March 2013, before making a 500% rally over through to 2016. The recent price consolidation is normal within growth cycles and we see this as an opportunistic and advantageous entry point to an otherwise attractive stock.

With an excellent track record behind them and strong forecasts supporting a strong technical outlook, we are reckoning these early whispers of a larger recovery will prove to be anything but idle

chit chat.