2013 is shaping up as another pivotal year for markets following a 'tiresome' 2012 that saw some extreme volatility mid year, culminate in a positive Q4 performance. All in all, the ASX 200 added +14.5% - a result that probably sugar coated some of the complexities that investors had to deal with throughout the year.

That said, the mkt is now in a better place and prospects for 2013 seem positive, even though we'll probably still be reading and hearing about the same old macroeconomic headwinds and challenges in the year ahead.

At a macro level, Chinese growth is likely to pick up strength post the once in a decade change of leadership which takes place at the National Peoples Congress in March. Most estimates I read have China growing back up above 8% in 2013 which is clearly good for us, and the global economy more generally.

One of the main risks I can see in China is inflation but that's unlikely to become a problem until 2014 or beyond. After the inflationary impacts of their GFC support package, they're clearly reluctant to stoke up prices, particularly in some areas of their economy such as housing. This time last year I wrote..,.

One question that does trouble me a little is the challenge facing an economy that is hot in some parts and cooling in others. Yes, the Government has the tools available to re inflate prices if things start to come back too hard but how they support some parts whilst dampening others will be critical.

Property prices for instance are still at elevated levels and the government wants to avoid a bubble, yet they want to continue to support manufacturing given the slowing demand coming out of Europe. An interesting conundrum!

As is stands, they've done pretty well so far. They've cut interest rates across the board but only by about 55bp. They've reduced the Reserve Requirement Ratio for some banks - targeting the lenders that support smaller, local manufacturers. They also increased the flexibility within the banking system so loan rates (and savings rates) can be somewhat massaged depending on individual circumstances.

In essence, they seem to realise that their economy has many dynamic parts and that one size doesn't fit all. In 2013, infrastructure spend will be one of the biggest supporting factors for growth.

The US should see some better growth numbers too, given the private sector deleveraging process is more or less complete. Corporate America has remained fairly strong albeit with obvious nervousness (hence the lack of hiring). Once they start to see consumers spending again, and SME's investing, the big Corporates are likely to follow.

The situation is not as positive in Europe or Japan where we continue to expect ongoing struggles. I'm sick of talking about Europe and promised myself I'd do less of it in 2013, however one quick comment must be focused on the ECB and their actions in 2012.

At the start of last year we wrote....

The market can't have a sustained rally until we see that these nations can refinance debt and it seems that it will take some type of involvement by the ECB to provide the confidence needed in the market, which in turn will put downward pressure on bond yields.

The ECB came to the party mid way through last year and in my mind, that was the turning point for the region.

In Australia, the economy is actually showing signs of fatigue, and a likely up tick in unemployment as well as continued issues with consumer and business confidence should see the RBA remain active, and we expect cash rates to be 2.5% by mid year. (NAB expect 2.25% and ANZ are at 2%). This will be the most influential theme for domestic markets in 2013.

One of the biggest calls by the RBA last year was the prediction that the mining investment boom would peak lower, and end sooner than they had originally thought. They're now calling a peak at the end of 2013 and are feeling an obvious need to help stimulate other sectors, - in the hope they'll take up the slack.

I'm not as sure as the RBA that investment will peak this year. One economist I find insightful is Adam Carr. He treads his own path and often contradicts main stream thinking - I like that.

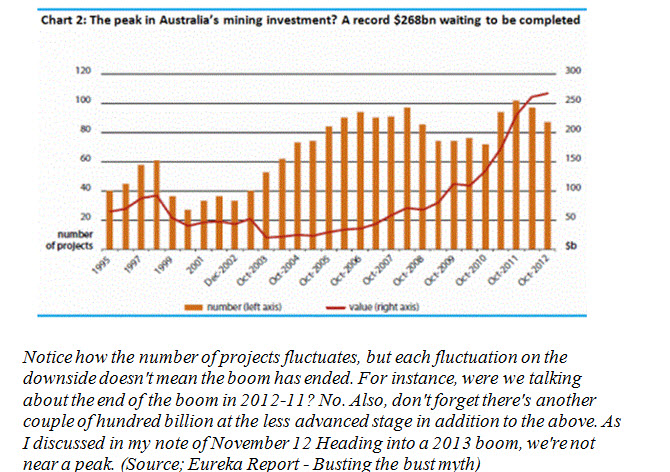

He recently wrote....According to estimates last week, still $268 billion in committed investment projects - an upgrade from previous estimates and over three-times the amount of mining investment completed over the last year. That was itself a record. Have a look at chart 2 (from the Bureau of Resource Economics) as a reminder.

One of the main aspects he sights in other articles is the massive investment in LNG. Although we might be seeing investment in more traditional mining businesses such as Copper and Iron Ore taper off, the massive amount of development in gas is more than enough to keep the boom going.

Current Market Stats

Currently, the ASX sits at 13.1 times forward earnings, which remains on the 'cheap side' of historical averages.

We also see collective Dividend Yields around 5% and when adding in franking credits, and the expectations towards cash rates, it adds to the appeal. Also important to note, that's a stat that covers the entire mkt - a lot of the portfolio's we run are yielding 7% or more, then add franking on top.

Dividend yields also compare favourably to Bond yields.

Although the market remains somewhat undervalued based on historical multiples, we have seen a recent rally in stock prices which has been on the basis of PE expansion rather than growth in earnings.

That's not necessarily a reason to be alarmed yet, as bullish phases

pre-empt earnings growth - however it's growth in earnings that support sustained moves higher. So we do need to see some signs of earnings optimism by Q2 at the latest.

Here's another take on mkt PE's which is a more dynamic way of viewing its relationship with different periods within the cycle.

Market outlook

I expect the ASX 200 to be above 5000 by year end. This is built somewhat on the improving macro backdrop, but more so on the impact of domestic monetary policy which I think will;

1.Reduce the appeal of alternative assets (mostly cash), and

2.Ultimately bring down the AUD towards 90c which, although is still high from a historical context, would be at a level that wouldn't pose too much of a headwind for business.

I think the second point there is the contentious one. I've been looking for the AUD to come back for the past few months but it just hasn't despite the tightening interest rate differential between us, the US & Europe.

One of the main impacts the Dollar has from an equity markets point of view is the attractiveness or otherwise of our mkt to overseas funds. If our market falls, the AUD is likely to fall as well, making it even cheaper. If we rally, the AUD is also likely to move higher making it even more expensive.

So, because of these factors, I think any weakness (3-5%) in our mkt will be bought into, while its hard to see our mkt really kicking into gear given the impact of the currency. That's one of the reasons why our target is around the 5000 level by year end - and not higher.

That said, if we do see any type of Central Bank intervention in our currency mkts, where the RBA offer up some of their currency reserves , which prompts weakness in the AUD, that's likely to be the catalyst for the mkt to really kick into gear. In my mind, that's the time to go a lot heavier into equities and it should be the start of the next real bullish phase in the market (not just a bear mkt rally).

I know this is an optimistic call and it will be met with some decent skepticism however its harder to argue with charts. We've had 12 years of a secular bear market - history shows they generally last about 9.4 years in the post world war two era.

So, if we have any faith in past experience, we've got to be conscious that at some point, probably soon, we will come out of this broad range trading environment and head into an upward bias.

A few observations

1. Stock markets don't necessarily track underlying economic performance

This has been particularly obvious with the strong stock mkt performances in Europe and the US, where economies remain relatively weak. Contrast this with China, where the economy is strong, stocks only added +3% in 2012 . This theme has also been obvious in Australia over the past few years where our stock market has under performed other developed economies despite our underlying economic metrics showing relative strength.

So, economic strength or otherwise doesn't necessarily have a high correlation to market performance, and mkts can indeed overcome economic headwinds. What really counts is the policy being rolled out by Central Banks and Governments. China had a tightening bias throughout 2011/2012, but it now seems they're more likely to start easing again. In Australia, our Central Bank was sluggish to react to global issues and we had relatively tight monetary policy - now the RBA is clearly in an easing mode.

2. Political incompetence is being increasingly tolerated

by mkts and even though we'll continue to see Republican's & Democrat's - Labor and Liberal's, dominate headlines, we're unlikely to see the mkt react as violently to politicly driven news flow as we saw in 2011/12.

On the domestic front, we've got an election coming up this year and the current Govt finds itself in a toxic position, helped only by the considerable doubts about the Oppositions ability to manage the treasury benches, not to mention their inability to put forward anything that borders on constructive policy.

It may sound harsh, but this lack of faith in either political party renders them both liabilities to economic growth and I've little confidence in either Gillard or Abbott as our PM...(surely the Libs have a better candidate...?). Anyway, one positive coming from this years election could be the fate of the Independent's, who have held way too much power in the parliament since the compromised Govt took office.

3. Market information & commentary is instant, and the ease that sometimes uneducated opinion finds an audience has made it increasingly confusing for investors to decipher what's valid and what's not. With so much noise, contrasting opinion, real time updates and sensationalism from some parts of the media, its been hard to maintain clarity of thought - that theme unfortunately is one that will continue and expand in the years ahead.

Although information is good and knowledge is power etc, I think at times it can be counter productive when we're in the business of making medium to longer term investment decisions. I think this year, more than most, it will be important to understand the macro backdrop, but not get caught up in its noise. Instead, focus attention more towards analysing sound investments.

The concept of yield support - a big theme in 2012 that is set to continue

This concept has built momentum over the past 12 months, and is likely to continue into the first half of 2013 at least. Cash rates have come back from 4.75% at the end of 2011 to 3.00% now and if we reach our estimated level of 2.5% by mid this year, that would equate to a fall of 2.25% - or in other words, if you've got a $1m sitting in the bank earning the cash rate, instead of getting $47,500 pa, you'll get $25,000 pa.

In contrast, a diversified portfolio of shares and fixed interest securities can yield more than 7% plus franking. Granted, there will be some capital volatility however the return differential is quite significant.

I suspect this is a conversation that will be had by many of the 910,000 Self Managed Super Fund Trustees now in Australia, that control about 30% of the $1.4 trillion in superannuation funds domestically. That figure collectively has risen by $117.5 billion - the second-highest figure on record - in the year to June 30.

Looking at the bank funding mix, it shows a lot of new money has gone into term deposits, attracted by high interest rates and pretty aggressive deals by banks & building societies as they diversified their sources of funding, away from more volatile International debt mkts, to domestic deposits.

That money has been earning decent returns as cash rates have been relatively high. Unfortunately for savers, that's no longer the case and investors are looking for income elsewhere. That's not a new theme - I actually wrote about it in last years report (click here) - however it's one that I expect will continue throughout 2013.

Key yield plays; ANZ, NAB, OKN, DWS, UGL, TLS, MIN, MTS, LEP, ALQ, SCP, WAM, BWP, SPN, WTF, FLT, SUN, MND, GEM

Another strategy that served us well in 2012 was having a relatively high allocation to fixed interest securities such as Bonds, Subordinated Notes & Hybrids, and we'll continue to maintain allocations to this area of the market.

That's helped to reduce portfolio volatility, increase yield and offer retirees a more balanced income stream throughout the year (most pay quarterly distributions). Although we still hold a number of these securities, the majority are trading well over face value which has lowered yields. Generally speaking, we'll now prefer to look at new issues as they arise rather than buy above face value on mkt.

Key fixed income plays; ANZHA, WBCHA, CWNHA, HLNG, TTSHA, WOWHC, HBSHB, CTXHA, SVWPA, CBAPC.

What about cyclicals in 2013?

This brings up the obvious question of what now for cyclicals? Higher beta stocks that pay less in dividends, retain more profits for growth and are generally linked to global economic expansion. Contrary to some views mid last year, I don't think this part of the mkt is dead, and it will roar back to life if we see (as expected) an up tick in China and continuing improvement from the US.

That said, I think the performance of some companies over the past few years has rendered them 'no go' areas for a portion of investors - and that's a valid decision. We all learn from our experiences and the misconception that BHP was bullet proof, China would continue to grow unabated, and Newcrest was the 'must have' Gold company in Australia, have proven somewhat misguided.

By their very nature, the earnings of cyclical stocks are more volatile than some of the high quality industrials we've got listed on the ASX, but it cuts both ways. They'll under perform in times of weakness, and out perform in times of strength. The real issue was not in the stocks themselves, but the sometimes unrealistic expectations of those that owned them.

If your portfolio has these stocks, as many do, you'll get a lower yield with more capital volatility. When things are good, you'll get more capital growth than your more defensive neighbour, but you've got to accept the added gyrations when they occur. Like many things in life, it's a trade off - and there's no such thing as the holy grail when it comes to investment.

I guess the biggest lesson here is understanding the way in which things trade in a portfolio, and constructing a portfolio that is suitable for your stage of life.

To sum up

I'm optimistic about the opportunities 2013 can bring. There are certainly risks around and I'm fully aware of the complexities that face investors globally. I can say with a degree of certainty, that mkts won't rise in a linear fashion, there will be pullbacks along the way and these will be our opportunities. I don't think we're in a mkt yet that needs to be chased.

When the short term sentiment is bullish, hold your positions and enjoy the ride. When mkts pull back, as they invariably do, selectively add sound investments to your portfolio.

At the start of last year, we suggested the following investment structure. We don't think a lot has changed and it's still as relevant now as it was then...

- Hold a selection of somewhat boring, high yield securities >7% that offset a lot of growth potential with a higher degree of earnings certainty. By this we mean securities that pay a high yield now with the understanding that the income will probably stay static for the next few years. These can include stocks and hybrid style investments.

- Complement this with some stocks that pay decent yields >4% now, but have strong trends in earnings and an underlying driver that will see those earnings continue to rise. This should filter through to growth in dividends over time.

- Combine options in the portfolio to smooth returns and take advantage of volatility. When we use options, we're primarily sellers of options (not buyers), with options being used to reduce risk, rather than adding risk to the portfolio.

- Consider using interest rate securities such as Hybrids to further reduce volatility and increase income.

- Be active rather than passive in the market. The set and forget approach is dead and active management will be key in 2012 & beyond.