EUR/USD

It didn't take long following the Spanish election result for the market to test the resolve

of officials to find a solution to the debt crisis. Bonds got hammered again, with Spanish

yields heading to 6.62%, despite the ECB stepping in to provide support. Equity markets

were heavily sold. The DAX & CAC were both down 3.4% and FTSE -2.62%. The S+P is

closing down 1.86%. Moody’s joined in by issuing a warning on the French AAA credit

rating and the Bundesbank issued its own warning by lowering the German economic

growth outlook for 2012 from 1.8% to 0.5%-1.0%.

Across the Atlantic, things were no better. The “super committee” are struggling to

come up with the $1.2T budget cuts required over the next decade. Should they fail,

(they may well admit defeat after the US equity markets close), to find the required

savings by Wednesday, then automatic spending cuts will be triggered. All this and an

election year too!

The only good news today has been that US existing housing starts, expected down

2.2%, actually rose by 1.4%. The DXY rose to a 6 week high at 78.26.

Given the plethora of bad news from Europe, the Euro has held up remarkably well,

currently pretty much unchanged from the Asia open on Monday. We have seen an

intraday low of 1.3429 before bouncing in a market that looks to be sitting very short of

Euros. It would appear that the smallest bit of good news could spark a pretty sharp

short covering rally. Where that good news is likely to come from though, is anyone’s

guess.

1.3400/20 is pretty major support now and a break here would be required to move

towards 1.3270 trend line support. We need a close under 1.3380 to really accelerate to

the downside.

To the topside, 1.3565 now provides the immediate resistance ahead of 1.3620 and

1.3695. A short squeeze would not surprise, in the short term, but for Asia today I

suspect 1.3460/1.3560 should cover it.

Look out for the US GDP and the FOMC Minutes later on.

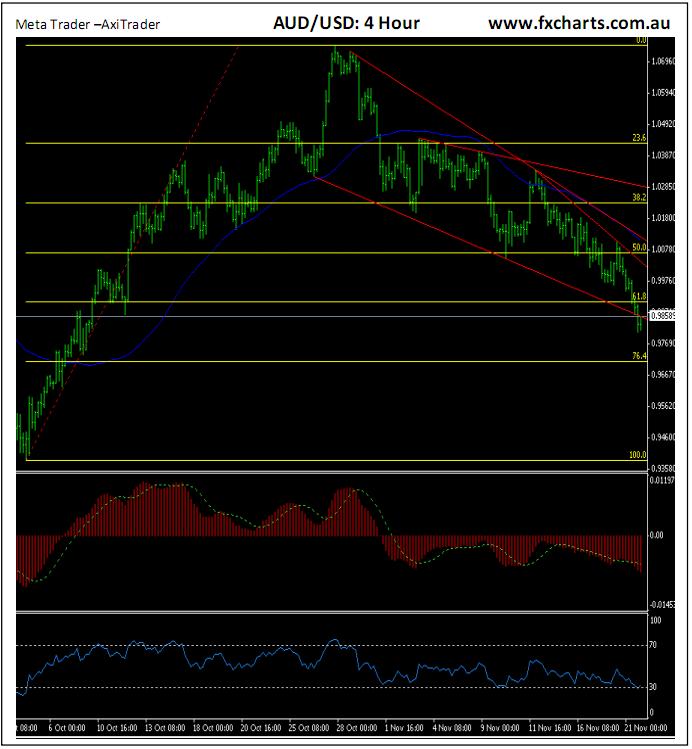

AUD/USD

The AUD held centre stage today for all the wrong reasons, taking a beating as

risk positions were cut all over the place. The news that the mining tax was set

to pass and that Qantas talks had broken down weighed heavily and following

the lead from Equities (S+P -1.86%), the AUD headed lower soon after the

markets opened. The decline accelerated once Europe got in and eventually

took out the support levels at 0.9910 and then 0.9860. We have seen a low of

0.9808 before an anaemic bounce to current levels.

From here things don't look very pretty and the immediate support is rather

thin on the ground. The day’s low (0.9808) will provide an intraday prop and

below here, there is not a lot until 0.9710. That said, the hourly’s are pretty

oversold and given that we are currently 120 bp lower than Asia yesterday, it

would not surprise to see some profit taking providing some support today,

particularly as the Euro has held up pretty well.

I would think 0.9800/0.9900 might cover it for the session and while there may

be some short term buying from profit takers, the greater trend remains down

and above 0.9900 should see some keen sellers.