EUR/USD

the Non Farms grew by 80,000. Unemployment reduced mildly to 9.0%, the G20

resolved nothing and the Greek Vote of Confidence has been won in pyrrhic fashion

by Papandreou, who now looks likely to resign. Where does this leave us? Confused.

With Europe sliding into recession (German Sept Factory orders down 4.3% - Fri),

Italian bonds trading above 6% and the EU in complete disarray it should be easy to

make a case for a much lower Euro. But it isn’t. The US has plenty of problems of its

own with unemployment unlikely to improve appreciably any time soon and it

would not surprise to see the Fed start the printing machines in the next couple of

months. Every time the Euro takes a dip it appears that various Central Banks are on

the bid and have an interest in it remaining at around current levels. It therefore

looks as though the wide consolidative trade is likely to continue for the time being.

Early in the week all eyes will remain firmly on Greece as Papandreou looks to form

a coalition government and to convince the EU to release the next tranche of the

bailout package. If only it were that easy. The Greek opposition want Papandreou’s

resignation and unity doesn't seem high on the agenda. The idea of Greece sticking

to the austerity measures, staying in the EU and everyone living happily ever after

doesn't seem very likely. Even if they do, the market already has one eye fixed

firmly on Italy where the vital vote on spending reform takes place on Tuesday.

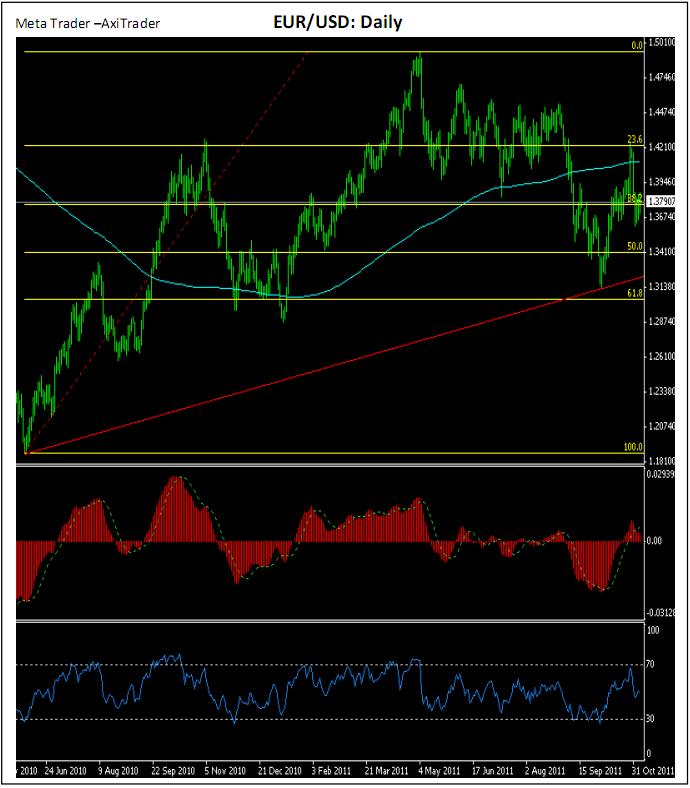

Technically the Euro looks pretty comfortable at around 1.3800. It would not

surprise to see the wide 1.34/1.42 range continue while the market struggles to

keep up with the daily political machinations from Brussels, Athens and increasingly

Rome, where Berlusconi isn’t likely to win a popularity contest any time soon.

The short term pressure for the Euro appears to be mildly to the upside, but having

said that, 1.39/1.40, if we were to see it looks toppish. To the downside 1.3600

should provide support early in the week. Choppy conditions look to be the way of

it for the time being so best bet is to take only a short term view and to trade

session by session.

This week’s Economic highlights are relatively light but will include China CPI, PPI

(Wed), German CPI & ECB Monthly Report (Thur)

AUD/USD

Technically it would appear that the AUD may enjoy some short term upside

movement early in the week. Mildly positive 4 hour indicators suggest an

attempt is likely to move back above 1.0400 and the 200 DMA at 1.0413. Above

here, 1.0450 is a hurdle to be overcome. If we do, then a move back towards

1.0600/10 looks possible where I would consider fading the rally for the next leg

lower, which I think can see a return to last week’s lows around 1.02 and then

the possibility of a continuation to the 0.9900/1.000 area, although this is too

far away to consider at this time.

The downside should see support, in the short term at Friday’s lows of 1.0315.

Below here, early in the week, 1.0290 and 1.0205 should provide a base.

As usual, the lead will be taken from the equity markets and how risk is being

perceived during any given session. For the time being, equities look as though

they are going to continue to gyrate in their recent volatile manner, reacting to

whatever the latest European news headline may bring and the Aud will react

accordingly.

The Economic highlight will be the Australian Unemployment numbers on

Thursday, although the Chinese CPI, PPI, Retail Sales and IP are all released on

Wednesday which will shake things up a bit.