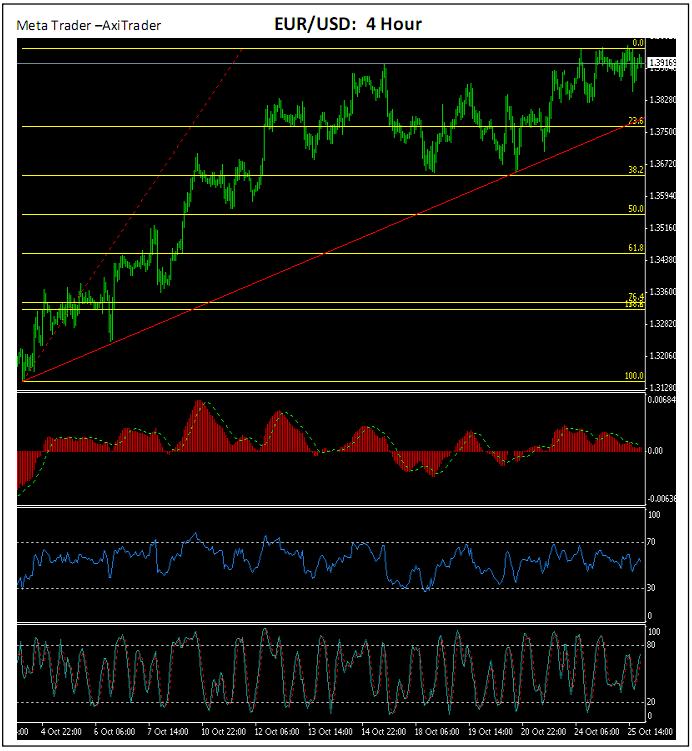

EUR/USD

The overnight news has become increasingly confused and negative from

Europe and it doesn't look as though there will be anything positive - if at all -

coming out of the EU tomorrow, with the possibility of a further delay being

touted around the markets. The cancellation of the Finance Ministers meeting

caused the Euro to spike down to 1.3850, but saw a quick recovery. There is no

apparent deal yet, on a Private Sector write down of Greek debt and no deal

either, on the makeup of the EFSF. To add to the woes, Italy failed to agree on

an austerity package item to raise the pension age and to top it off, the US data

was on the soft side today. Equity markets took the hint and headed lower, with

the S+P closing down 2%.

Despite all this the Euro has held up well when it had every opportunity to head

lower, posing the question as to how short the market really is? Or are the

banks selling assets and repatriating funds ahead of new recapitalization rules?

Technically there is not a whole lot of change from yesterday. Having been

down to 1.3850 and bounced successfully, it remains in place as the first level of

support, followed by a stronger base in the 1.3765/80 area, where trendline/Fibo lines converge. The topside target remains at 1.4005, 61.8% of 1.4545/1.3138. A break here would see a move towards the 200DMA at 1.4116

and then to 1.4210 (76.4% of the same move).

In Asia today I think we should expect further consolidation and 1.3880/1.3960

ought to cover it. Further out, the short term indicators have unwound. The

Euro, has spurned the opportunity to head lower, and may yet do so, however

it appears the market is still caught short and may want to test 1.4000 sooner

rather than later.

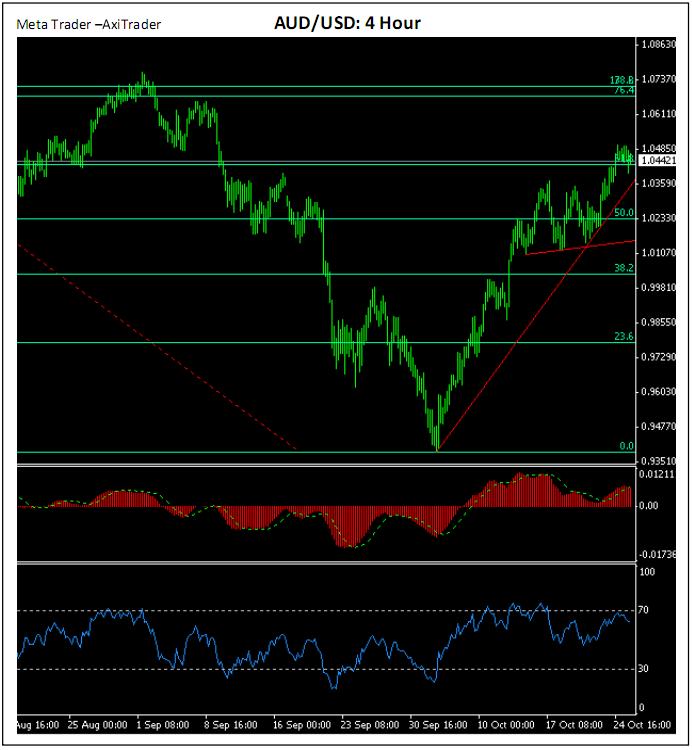

AUD/USD

The AUD has taken a breather today confined largely to a 1.04/1.05 range that

looks likely to continue in today’s session, at least until the 3Q CPI figure later

on this morning, where 0.6% is the expectation and will give a guide as to what

to expect from the RBA on Tuesday. Don't expect too much.

The dailies still point higher but much depends on the market view of risk assets

and if today’s move of 1.7% lower in the S+P is a barometer, we are unlikely to

see too much upside today unless the CPI surprises drastically to the upside.

Suspect that 1.0400/1.0470 should cover it early on, with the possibility of a dip

to around 1.0360 later on.