Date of Data Capture:

9/8/2016

Name:

NETCOMM WIRELESS LTD (NTC)

Classification:

Technology Communications

Current Price:

$2.90

Market Capitalisation:

$426M

Forecast EBITDA Growth:

96.5%

Gross Yield:

0%

Consensus Price Target:

$3.61

# Covering Analysts:

5

Discount at Current Price:

24.1%

Price Target Trend:

Increasing/Flat

Signal Time Frame:

Monthly/Weekly

Trend Bias:

Up/Flat Long/Medium-term

Indicators:

Short-term:

Neutral

Medium-term:

Positive

Long-term:

Positive Neutral

Recommendation:

Buy

Set-up Notes:

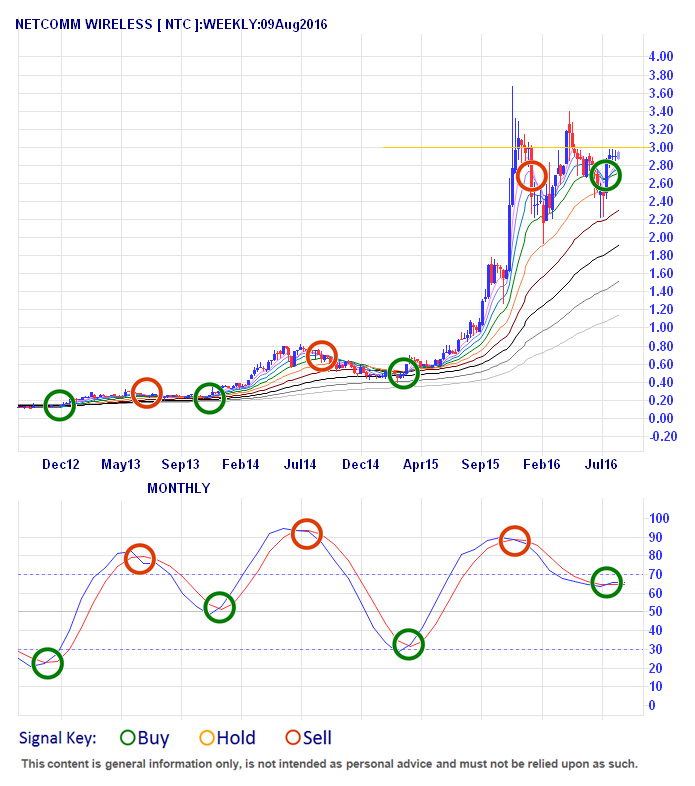

• NTC seems to be coming out of a 9 month consolidation and is sitting right below important structural resistance just its long-term signal turns positive again.

• The $3 ceiling overhead is significant and could provide some volatility as the price works its way through, with $3.50 a likely resistance target going forward.

• Support layers down from $2.74, $2.50 and $2.38 behind, but without a resistance dip we expect them to push higher with great fundamentals and good momentum building at this important juncture.

Growth Focus:

NetComm Wireless Ltd

Our primary focus here is capital gain, we will select our stocks from the ASX top 500 All Ordinaries Index.

In an age of wireless internet, when things comes down 'to the wire' it is not normally a good situation. For this reason and with an eye on the future we are looking at NetComm Wireless Ltd (NTC) as our Growth Focus pick and we believe they are ready to tap higher prices based on continued great performance within a truly massive market.

Founded in 1982 and headquartered in Sydney, NetComm Wireless is a leader in wireless internet and has already seen some remarkable success over the last few years. With their sights on further expansion, coupled with major contracts with global clients backing them up we believe they are likely to connect with further gains.

Even with current valuations seen as expensive by some, we are choosing to look forward from the recent contract deals with global operators and blue chip domestic clients and see that they are still potentially at quite an early stage of growth and valuation.

Accordingly, the estimates for sales and earnings growth are some of the most aggressive we have seen and while recent results have disappointed perhaps overly optimistic expectations, they have still shown excellent growth. Couple that with significant infrastructure investments we are thinking further growth will comm soon.

Despite NetComm increasing 15 fold within the last 5 years the trading history of the last 9 months looks more like a high-wire act with the price balancing precariously beneath structural resistance at $3.00. This is where it paused for breath back at the end of 2015 after completing a solid 600% run from 50c at the start of that year.

Any stock will enter a period of price consolidation after a strong run – and that is what we have seen here with loose gyrations winding their way through the medium-term timeframe while it blows off some steam in the bigger monthly picture. This has been constricting over the last year and is now due for a breakout just as the longer-term signal turns positive again for the first time in 8 months. With strong fundamentals looking sound and with technicals turning positive the time to connect to Netcomm could well be now as they look ready to net some gains.